How to Make a Fortune on Obamacare

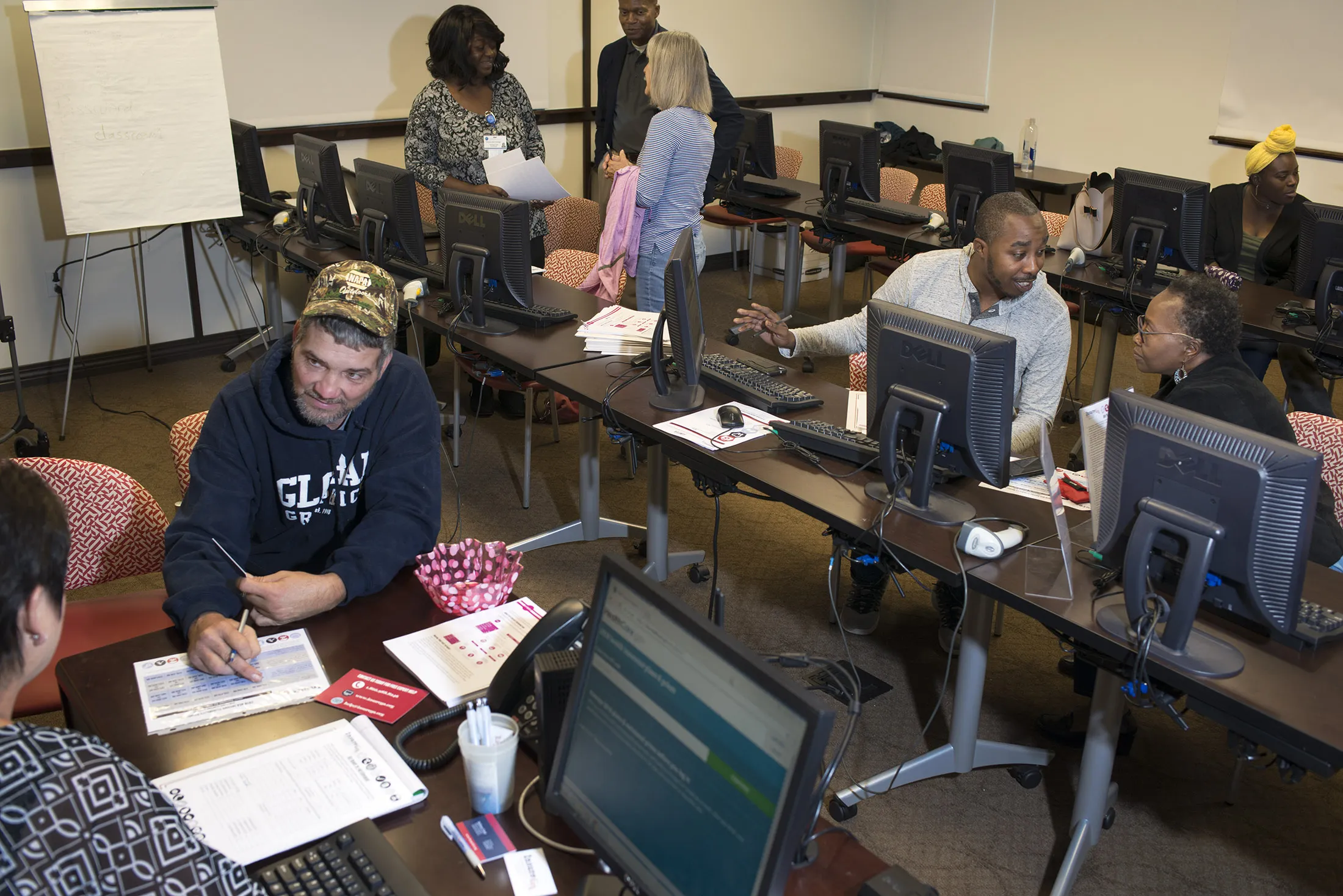

An insurance sign-up session at Phoebe Sumter Medical Center in Americus, Ga., on Nov. 9, 2017.

Photographer: Susana Raab for Bloomberg Businessweek

At the start of 2016, nine companies offered health insurance in Georgia through the federal Patient Protection and Affordable Care Act, aka ACA, aka Obamacare. Eighty-five percent of residents signing up could choose from among four to eight carriers, depending on where they lived. One by one, though, companies stopped selling insurance through ACA exchanges—they were spooked by uncertainty about the market’s future, or were paying more for care than they were collecting in premiums and other payments, or both.

As 2017 dawned, only five companies remained, and almost half of Georgia’s ACA population was choosing from one or two insurers. Then, in August, Anthem Inc. Blue Cross Blue Shield announced it would pull out of ACA marketplaces in 74 of Georgia’s 159 counties, leaving all but 14 counties with a single carrier for 2018. “We were beside ourselves,” says Melissa Camp, who directs a program to help people sign up for ACA benefits at the nonprofit InsureGA.