Race &Recovery

Late Covid Loans Hurt Recovery in Chicago’s Minority Neighborhoods

Bloomberg is tracking the economic recovery in minority communities across the country

This year billions of dollars in U.S. pandemic relief for small businesses finally made it to minority neighborhoods, reaching hair salons, daycares and restaurants in some of the poorest and most-segregated urban areas of the nation.

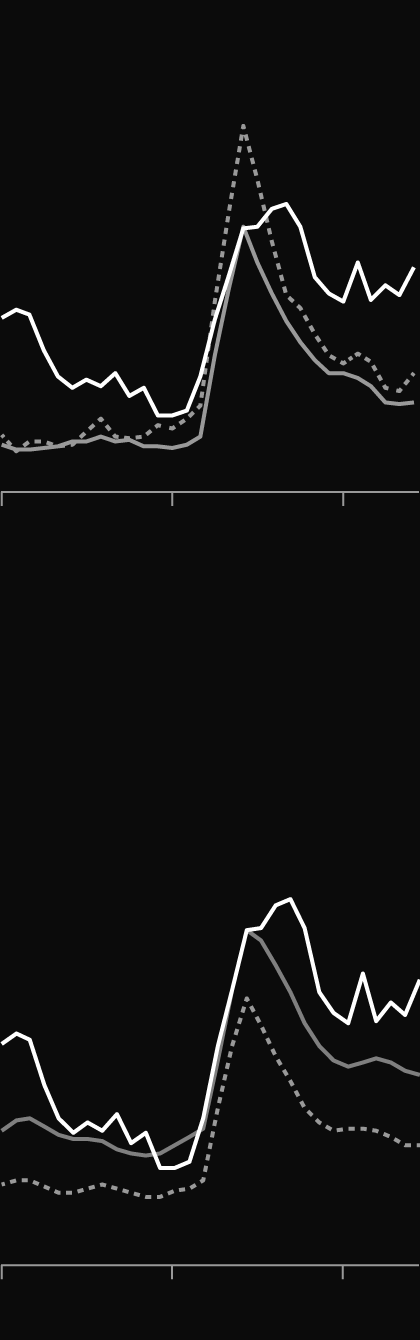

Chicago unemployment rates by group,

3-month moving average

Hispanic

13.8%

Black

7.3%

5.5%

White

2019

2020

2021

8.3 p.p.

Gap between Black and White unemployment,

June 2021

Chicago Black vs. U.S. Black unemployment rates, 3-month moving average

13.8%

9.2%

5.8%

National

overall

2019

2020

2021

Chicago unemployment rates by group, 3-month moving average

Hispanic

13.8%

Black

7.3%

5.5%

White

2019

2020

2021

8.3 p.p.

Gap between Black and White

unemployment, June 2021

Chicago Black vs. U.S. Black unemployment rates, 3-month moving average

13.8%

9.2%

5.8%

National

overall

2019

2020

2021

So far the infusion of Paycheck Protection Program funds has failed to translate into a meaningful economic recovery in many of these neighborhoods, data compiled by Bloomberg show.

Nowhere is this more on display than in Chicago, the only metro area tracked by Bloomberg where majority-Black zip codes have received more stimulus dollars per capita than White areas—albeit by a small amount—yet the pace of business reopenings is lagging and the local rate of Black unemployment is high. PPP loans are forgiven if businesses use a large part of the funds to keep employees on payroll, and the struggle to access federal aid early on in the crisis meant many small firms couldn’t stave off layoffs or even closures.

The latest data highlight how patchy the economic rebound has been in the U.S., where GDP growth is roaring nationally but many are left behind, including in minority neighborhoods from Los Angeles to Houston. The uneven recovery is a central reason why Federal Reserve Chairman Jerome Powell says the economy still has a ways to go.

Joblessness in Chicago’s Black community is considerably higher than the national average, but more in line with other cities when looking at White and Hispanic groups, according to local unemployment rates calculated by Bloomberg as part of an analysis of the recovery in more than a dozen metro areas in the U.S.

In Chicago, the delayed recovery is linked to historical neglect and investment starvation that would take more than pandemic federal loans to fix. Long before Covid-19, places like South Shore and Humboldt Park had endured decades of population decline, joblessness and store closures.

“Chicago on the South side and the West side—there are very challenged neighborhoods where economic enterprise is limited, many low and moderate income groups, and Covid hit those neighborhoods really, really hard,” Chicago Fed President Charles Evans said last month. “The recovery usually takes longer there.”

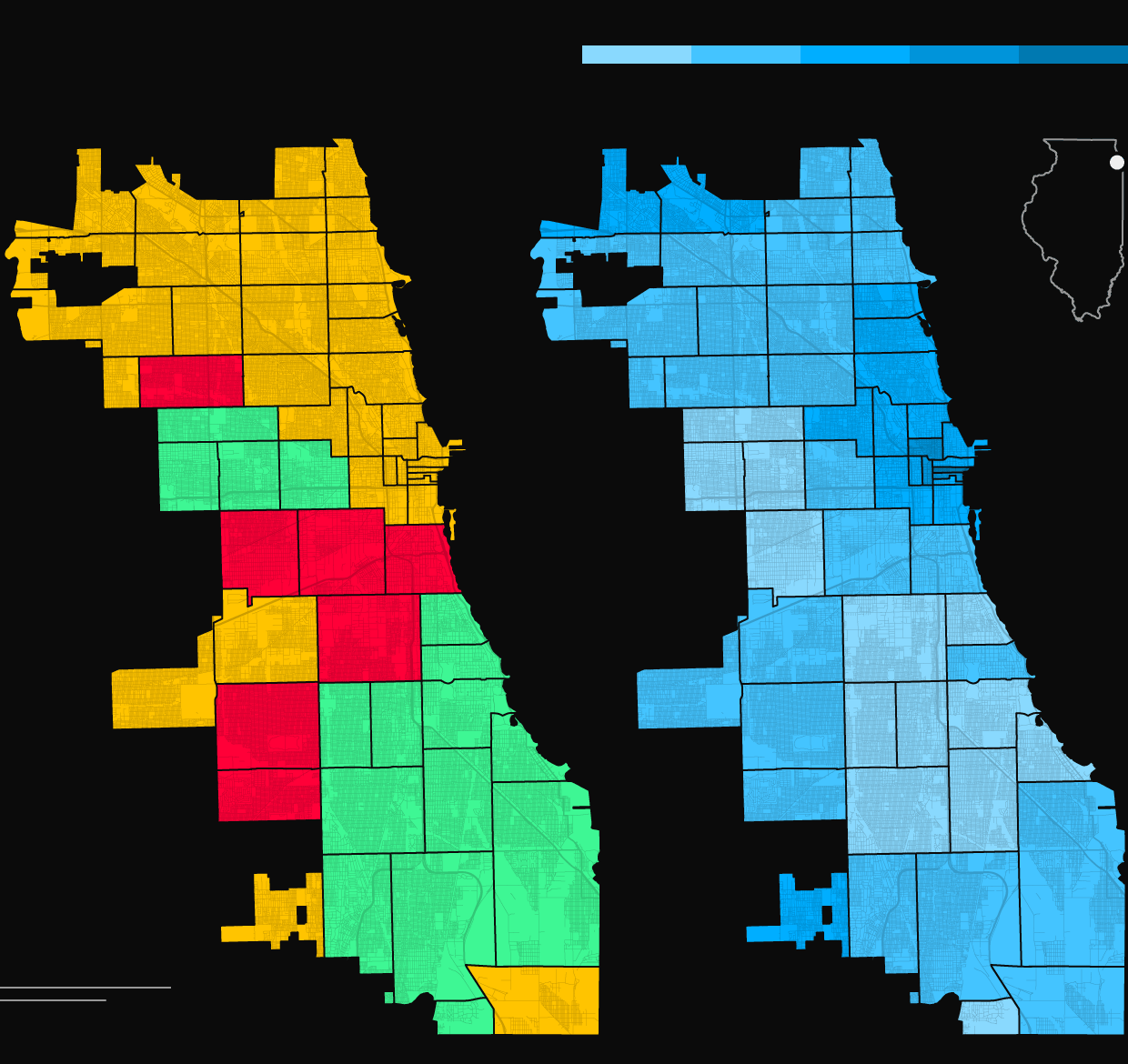

Windy City Wealth Gap

Majority racial/ethnic group by zip code:

Median household income (2019)

◼ Black

◼ White

◼ Hispanic

40K

80K

120K

$160K

Rogers

Park

Chicago

Forest

Glen

Edgewater

Jefferson

Park

Lake View

Belmont

Cragin

Logan

Square

Lincoln

Park

Humboldt

Park

Austin

Garfield

Park

Near

West Side

Loop

Lake

Michigan

Lower

West Side

Brighton

Park

Bronzeville

New City

Garfield

Ridge

Englewood

West

Lawn

South

Shore

Grand

Crossing

Ashburn

Calumet

Heights

Roseland

Morgan

Park

West

Pullman

5 miles

Hegewisch

5 km

Majority racial/ethnic group by zip code:

Median household income (2019)

◼ Black

◼ White

◼ Hispanic

40K

80K

120K

$160K

Rogers

Park

Chicago

Forest

Glen

Edgewater

Jefferson

Park

Lake View

Belmont

Cragin

Logan

Square

Lincoln

Park

Humboldt

Park

Austin

Near

West

Side

Garfield

Park

Loop

Lake

Michigan

Lower

West Side

Brighton

Park

Bronzeville

New City

Garfield

Ridge

Englewood

West

Lawn

South

Shore

Grand

Crossing

Ashburn

Calumet

Heights

Roseland

Morgan

Park

West

Pullman

5 miles

Hegewisch

5 km

Majority racial/ethnic group by zip code:

Median household income (2019)

◼ Black

◼ White

◼ Hispanic

40K

80K

120K

$160K

Rogers

Park

Forest

Glen

Chicago

Edgewater

Jefferson

Park

Lake View

Belmont

Cragin

Logan

Square

Lincoln

Park

Humboldt

Park

Austin

Near

West

Side

Loop

Lake

Michigan

Lower

West Side

Brighton

Park

Bronzeville

New City

Garfield

Ridge

Englewood

West

Lawn

South

Shore

Grand

Crossing

Ashburn

Calumet

Heights

Roseland

Morgan

Park

West

Pullman

5 miles

Hegewisch

5 km

Majority racial/ethnic group by zip code:

◼ Black

◼ White

◼ Hispanic

Chicago

Forest

Glen

Edgewater

Belmont

Cragin

Lincoln

Park

Humboldt

Park

Near

West

Side

Loop

Lake

Michigan

Brighton

Park

Bronzeville

Garfield

Ridge

Englewood

West

Lawn

South

Shore

Roseland

Morgan

Park

5 miles

Hegewisch

5 km

Median household income (2019)

40K

80K

120K

$160K

Rogers

Park

Jefferson

Park

Lake View

Logan

Square

Austin

Garfield

Park

Lower

West Side

New City

Grand

Crossing

Ashburn

Calumet

Heights

West

Pullman

5 miles

5 km

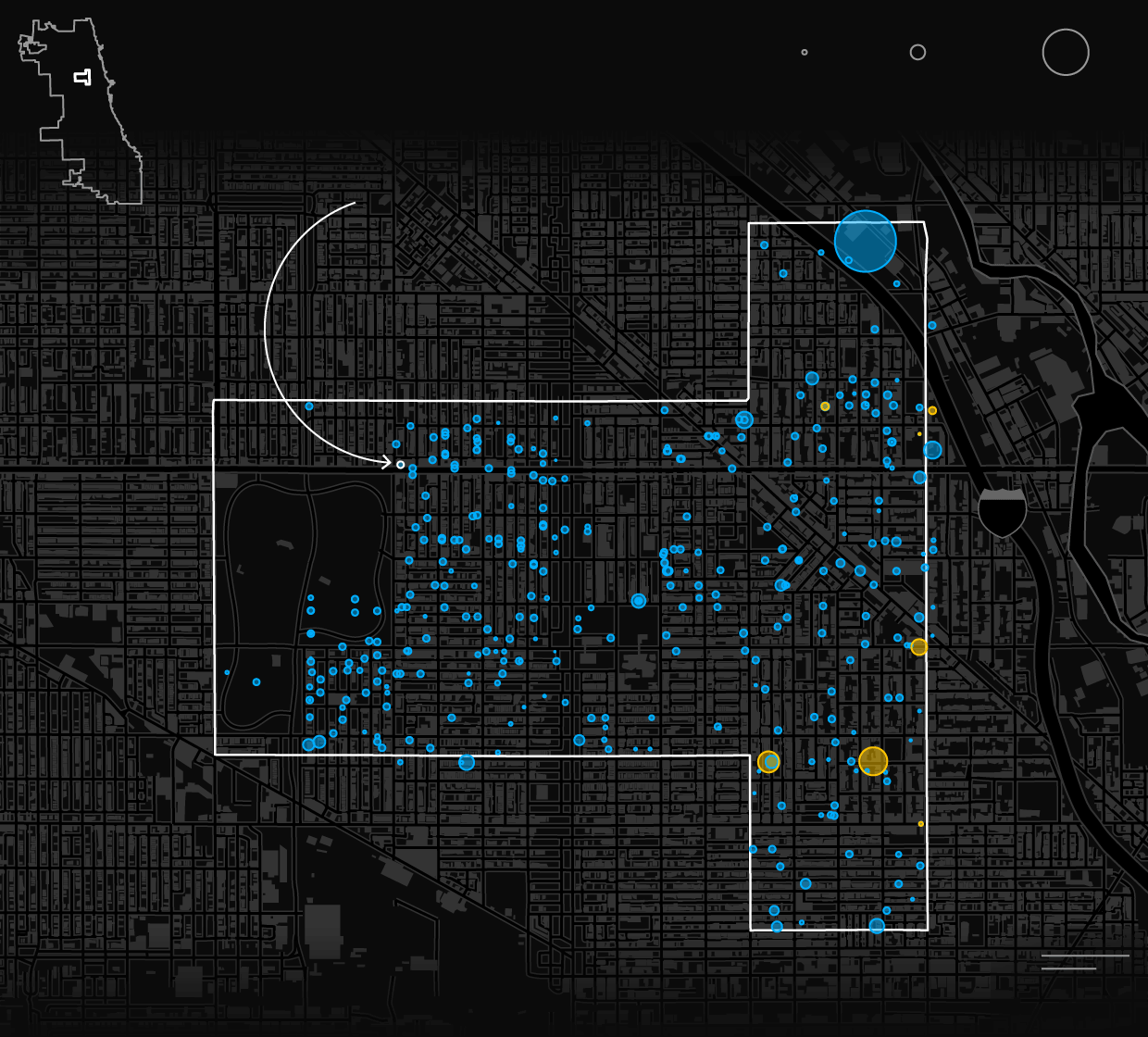

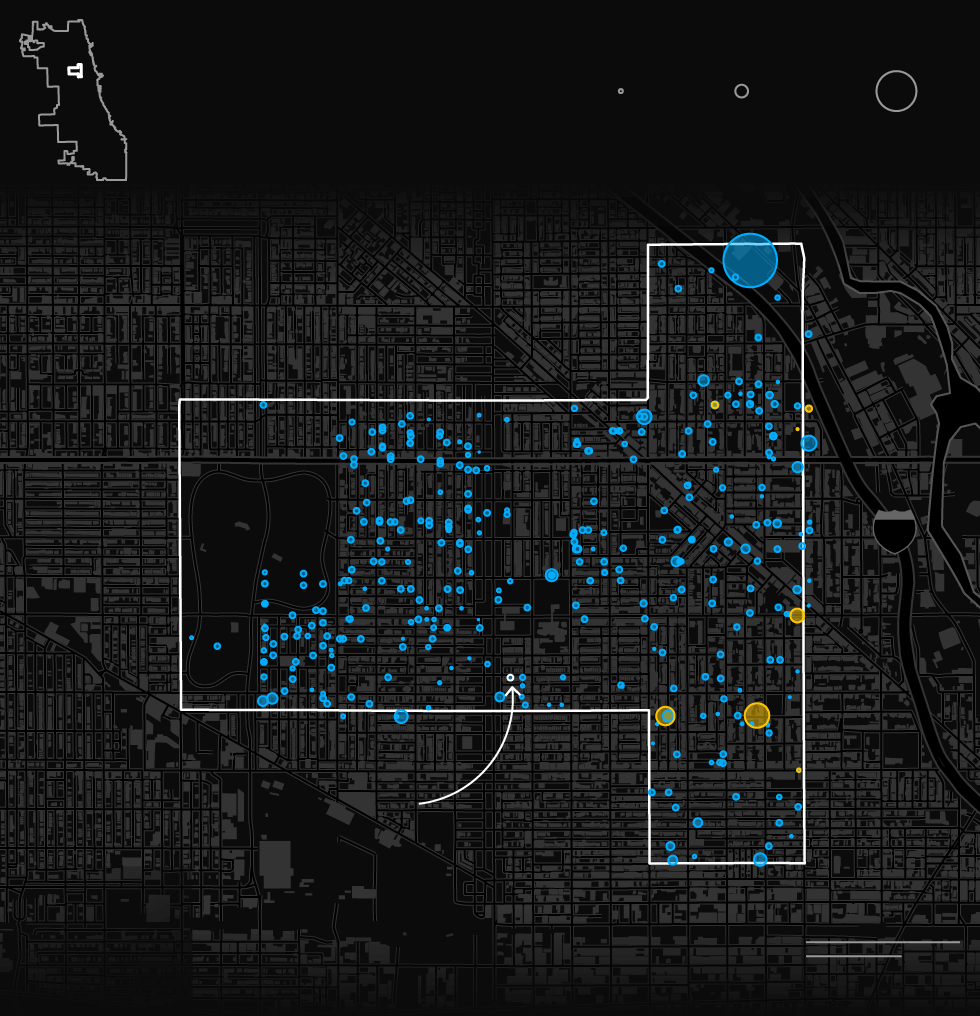

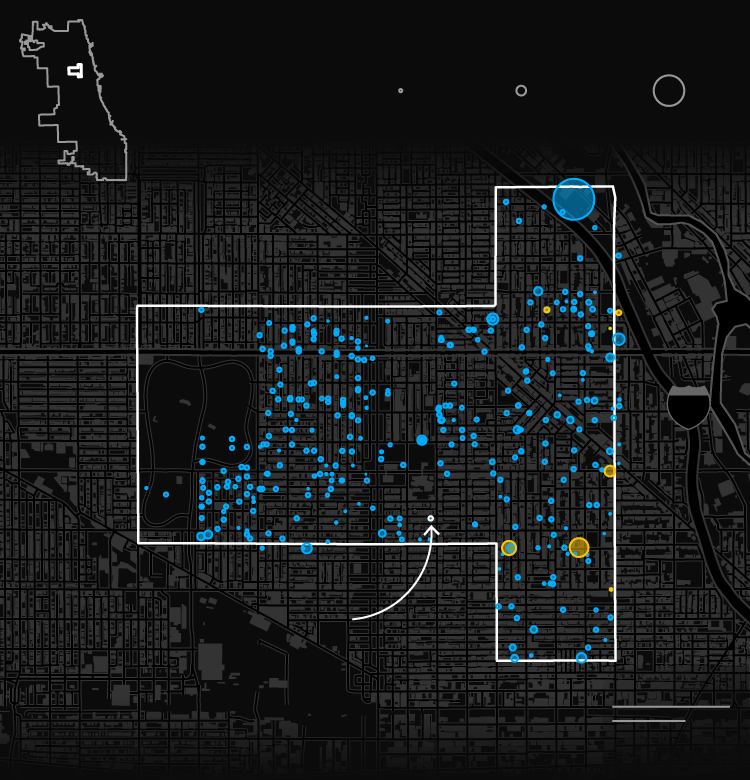

Small businesses in majority-Black areas of the city ultimately got $355.4 million for every 100,000 residents, compared with $347.5 million in White communities and $163.3 million in Latino neighborhoods, according to the data.

But Black neighborhoods of metro Chicago received 72% of their PPP funds this year, in the final round of the $800 billion program, while majority-White parts of the city got 65% of their loans last year, government data show. That means that by the time significant PPP money arrived in some minority neighborhoods, they’d already lived through the months of shutdowns and the worst of the pandemic’s economic impact.

The delays in securing federal relief when local economies needed it most threaten to further widen the racial wealth gap in the third-largest U.S. city, where 30% of the population is Black and 29% is Latino.

Chicago

Norridge

Irving

Park

Lake

View

60639

Majority-Hispanic

90

Belmont

Cragin

Melrose

Park

West Town

Austin

60622

Majority-White

Oak

Park

Loop

Lake Michigan

290

Chicago

Broadview

Cicero

Bridgeport

55

41

Brighton

Park

LA

Grange

90

Hyde

Park

Garfield

Ridge

60649

Majority-Black

Englewood

Hodgkins

South

Shore

94

1 mile

Ashburn

Burbank

1 km

Chicago

Irving

Park

60639

Majority-Hispanic

Lake

View

90

Belmont

Cragin

60622

Majority-White

Melrose

Park

West Town

Austin

Oak

Park

Loop

Lake Michigan

290

Chicago

Broadview

Cicero

Bridgeport

55

41

Brighton

Park

LA

Grange

90

Hyde

Park

Garfield

Ridge

60649

Majority-Black

Englewood

Hodgkins

South

Shore

94

Ashburn

1 mile

Burbank

1 km

Chicago

60639

Majority-Hispanic

Lake

View

90

Belmont

Cragin

60622

Majority-White

West

Town

Austin

Oak

Park

Loop

Lake Michigan

290

Chicago

Cicero

Bridgeport

55

41

Brighton

Park

90

Hyde

Park

Garfield

Ridge

60649

Majority-Black

Englewood

South

Shore

94

Burbank

Ashburn

1 mile

1 km

Chicago

60639

Majority-Hispanic

Lake

View

Belmont

Cragin

60622

Majority-White

West

Town

Austin

Oak

Park

Loop

Lake Michigan

Chicago

Cicero

Bridgeport

Brighton

Park

Hyde

Park

60649

Majority-

Black

Garfield

Ridge

Englewood

South

Shore

Burbank

Ashburn

2 miles

2 km

Chicago

60639

Majority-

Hispanic

60622

Majority-

White

Austin

Oak

Park

Loop

Lake Michigan

Chicago

Cicero

Brighton

Park

60649

Majority-

Black

Hyde

Park

Garfield

Ridge

Ashburn

Burbank

2 miles

2 km

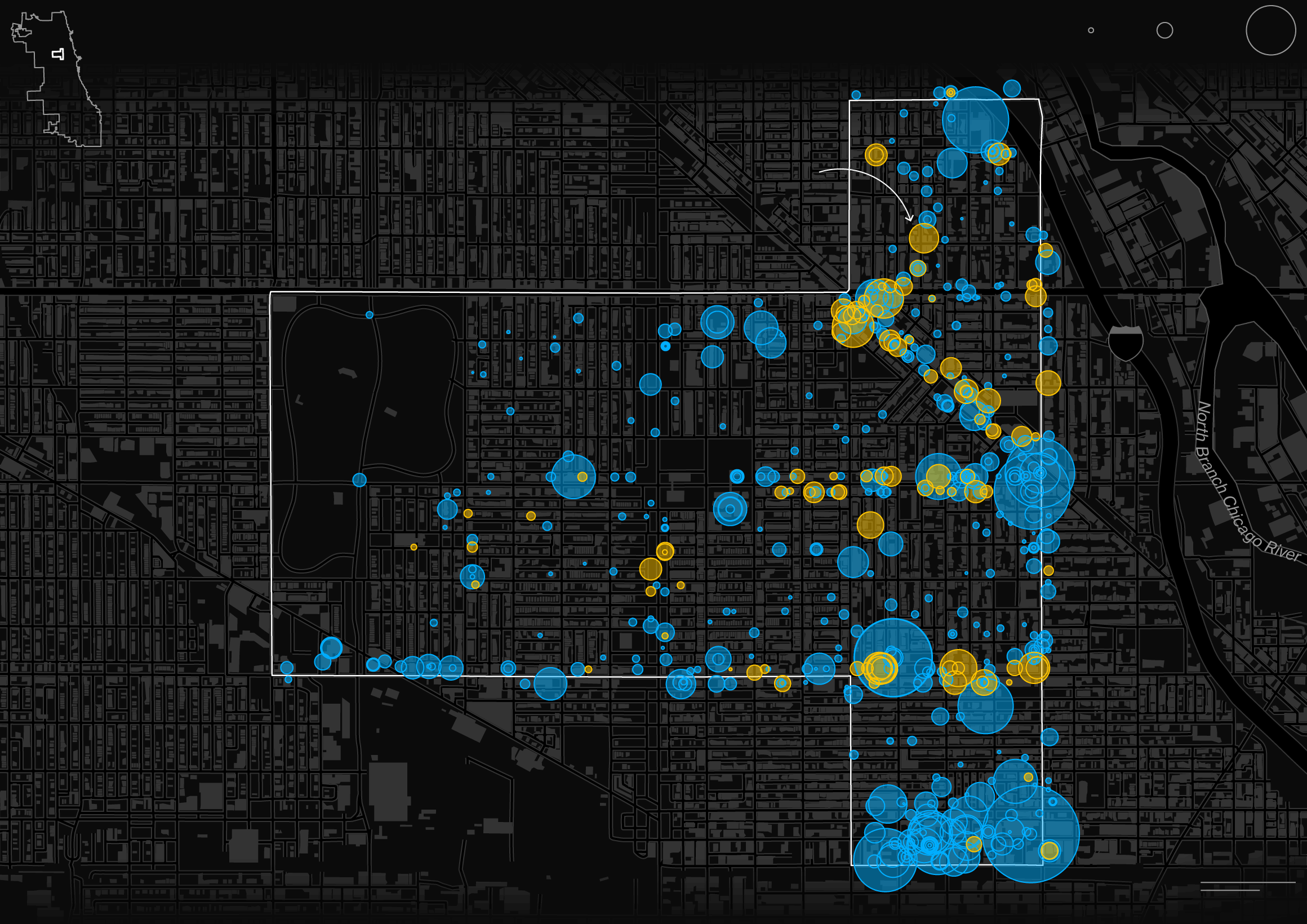

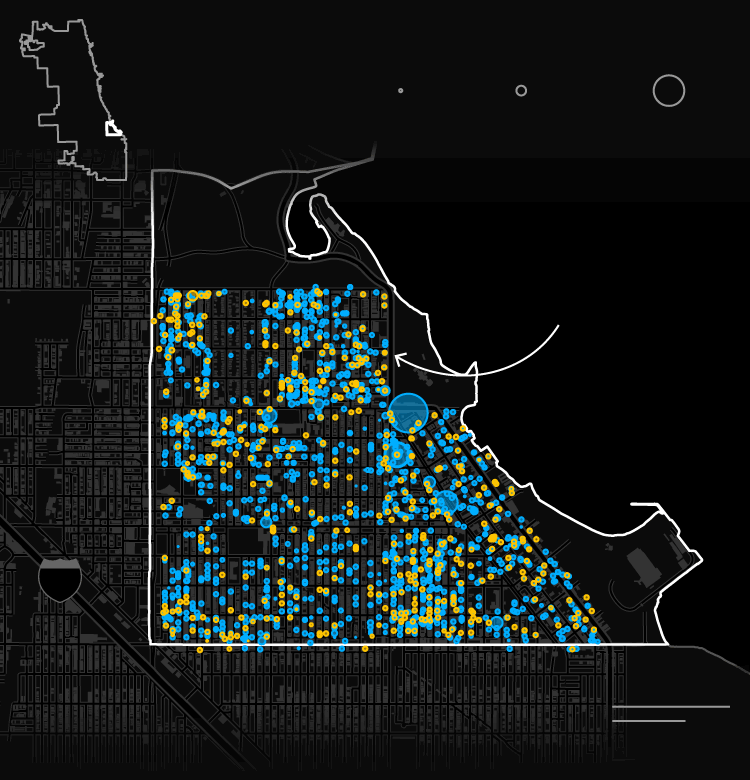

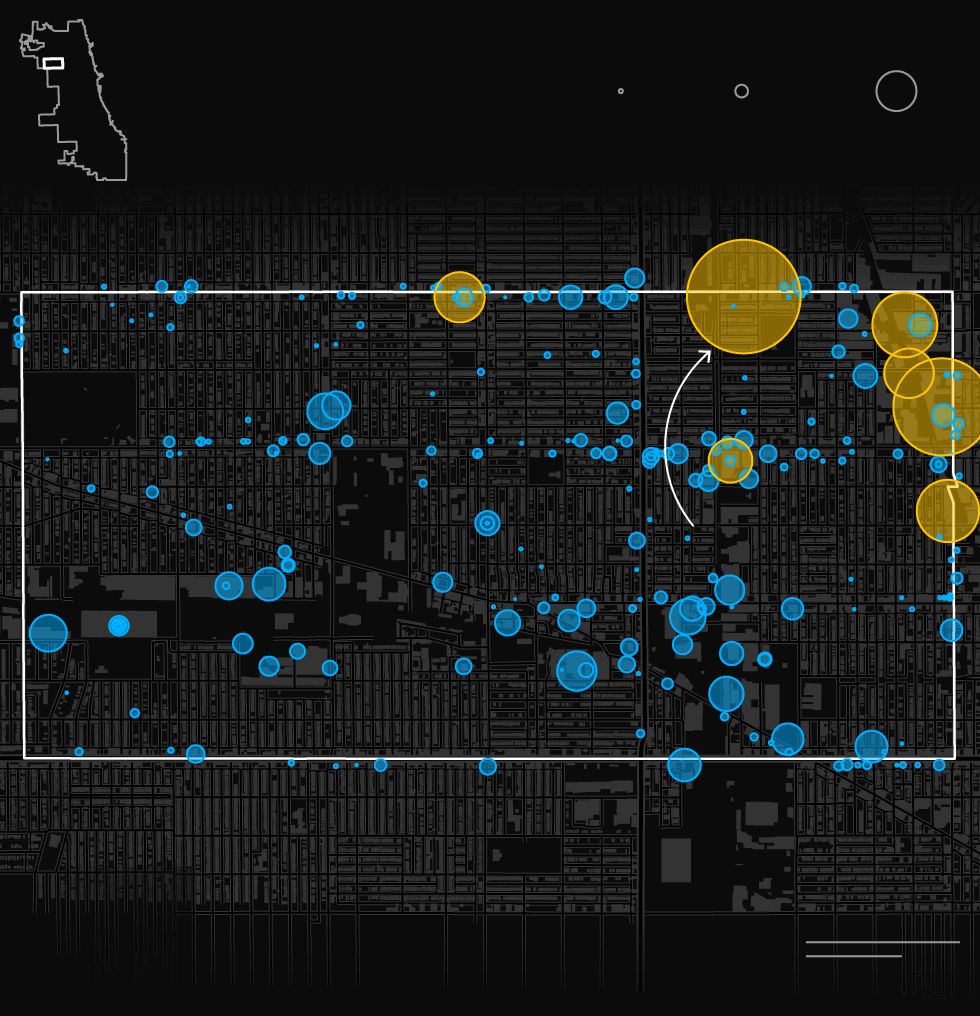

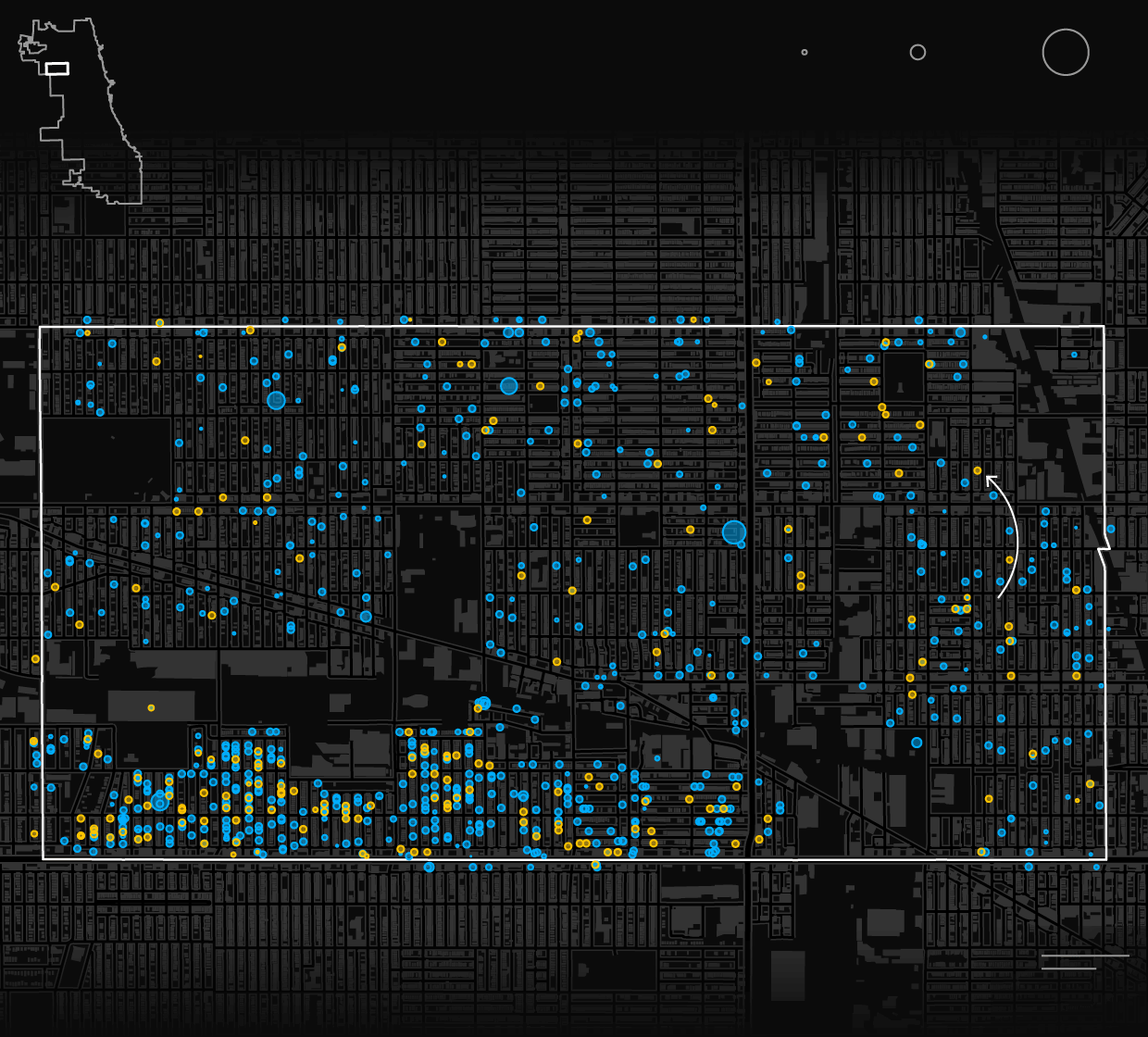

Zip code 60622

April 2020

$10K

Loan amount:

$100K

$1M

W Armitage Ave

Nearly $14 million went to restaurants and bars, among the businesses receiving the most loans.

Logan Square

Wicker

Park

W North Ave

90

N Kedzie Ave

N California Ave

N Western Ave

N Damen Ave

N Ashland Ave

N MilwaukeeAve

W Division Ave

Humboldt

Park

East

Village

Ukrainian

Village

Noble

Square

W Chicago Ave

West Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2020

$1M

Loan amount:

$10K

$100K

W Armitage Ave

Nearly $14 million went to restaurants and bars, among the businesses receiving the most loans.

Logan

Square

Wicker

Park

W North Ave

N Kedzie Ave

N Ashland Ave

N California Ave

N Western Ave

N Damen Ave

N MilwaukeeAve

90

Humboldt

Park

East

Village

Ukrainian

Village

Noble

Square

W Chicago Ave

West

Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2020

Loan amount:

$10K

$100K

$1M

Nearly $14 million went to restaurants and bars, among the businesses receiving the most loans.

W Armitage Ave

Logan

Square

Wicker

Park

W North Ave

N Ashland Ave

N Kedzie Ave

N California Ave

N Western Ave

N MilwaukeeAve

90

Humboldt

Park

Ukrainian

Village

Noble

Square

W Chicago Ave

West

Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2020

Loan amount:

$10K

$100K

$1M

W Armitage Ave

Logan Square

Wicker

Park

W North Ave

N Kedzie Ave

N Ashland Ave

90

Ukrainian

Village

W Chicago Ave

West

Town

Nearly $14 million went to restaurants and bars, among the businesses receiving the most loans.

.5 mile

.5 km

Zip code 60622

April 2020

Loan amount:

$10K

$100K

$1M

W Armitage Ave

Logan Square

Wicker

Park

W North Ave

N Ashland Ave

N Kedzie Ave

90

Ukrainian

Village

W Chicago Ave

West

Town

Nearly $14 million went to restaurants and bars, among the businesses receiving the most loans.

.5 mile

.5 km

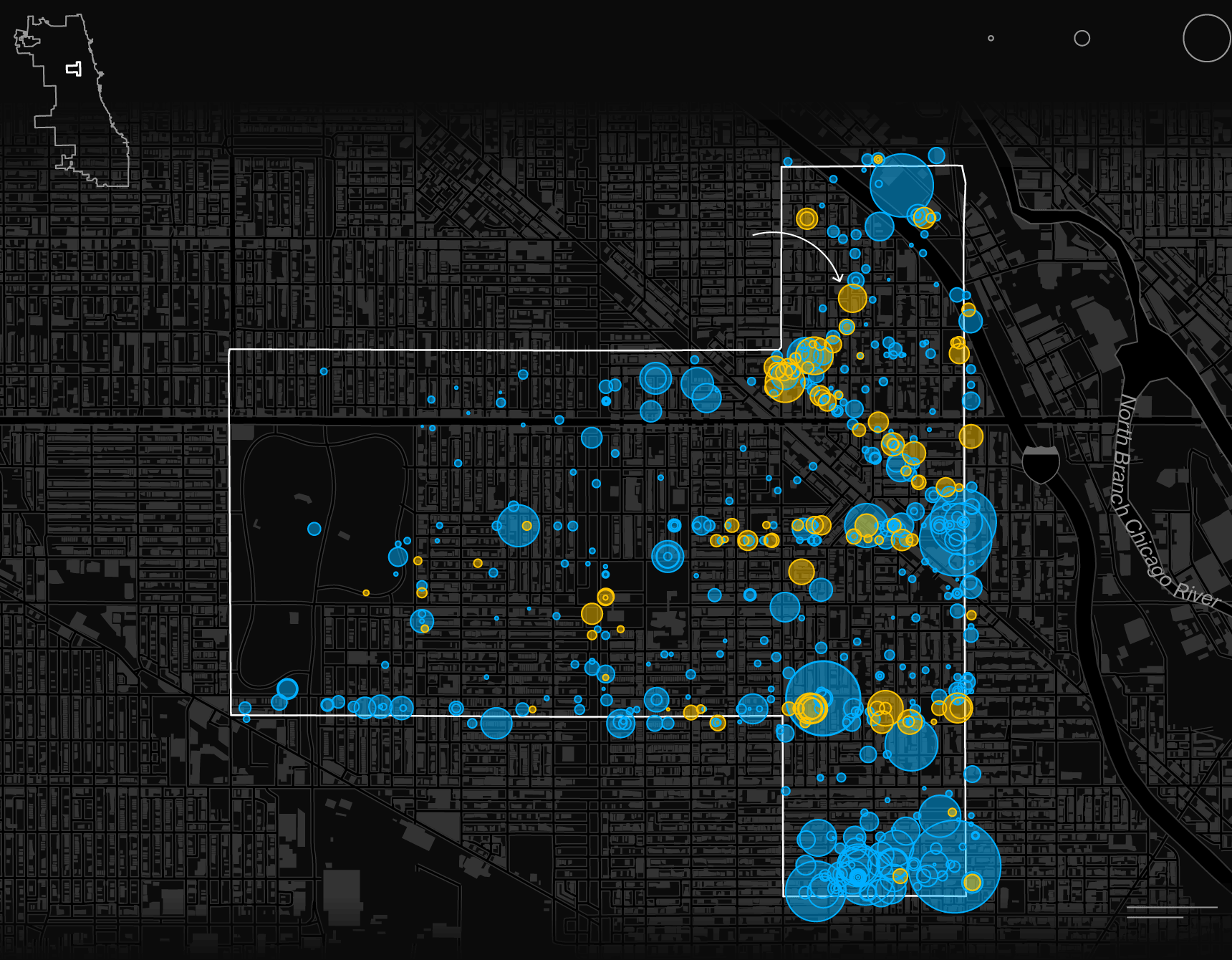

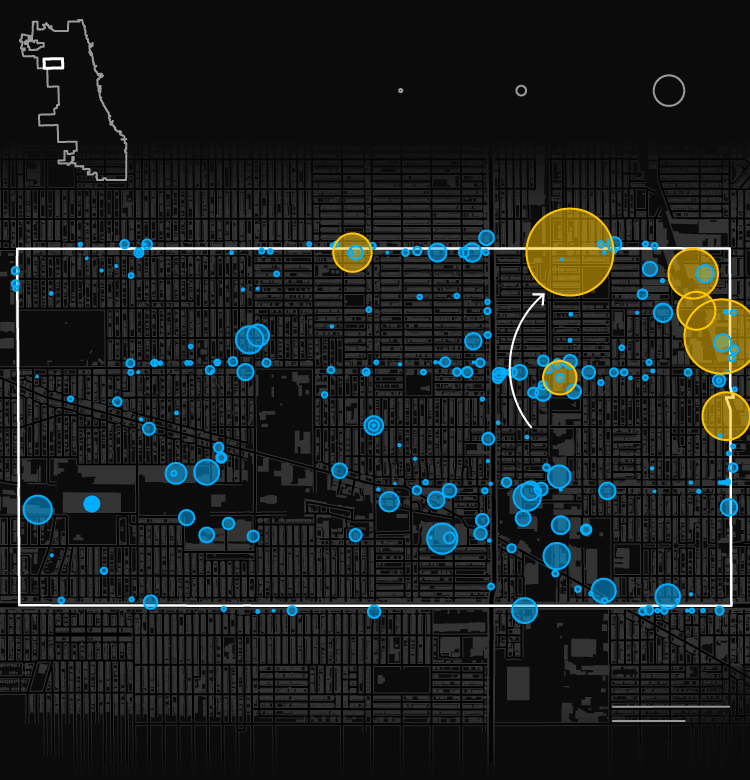

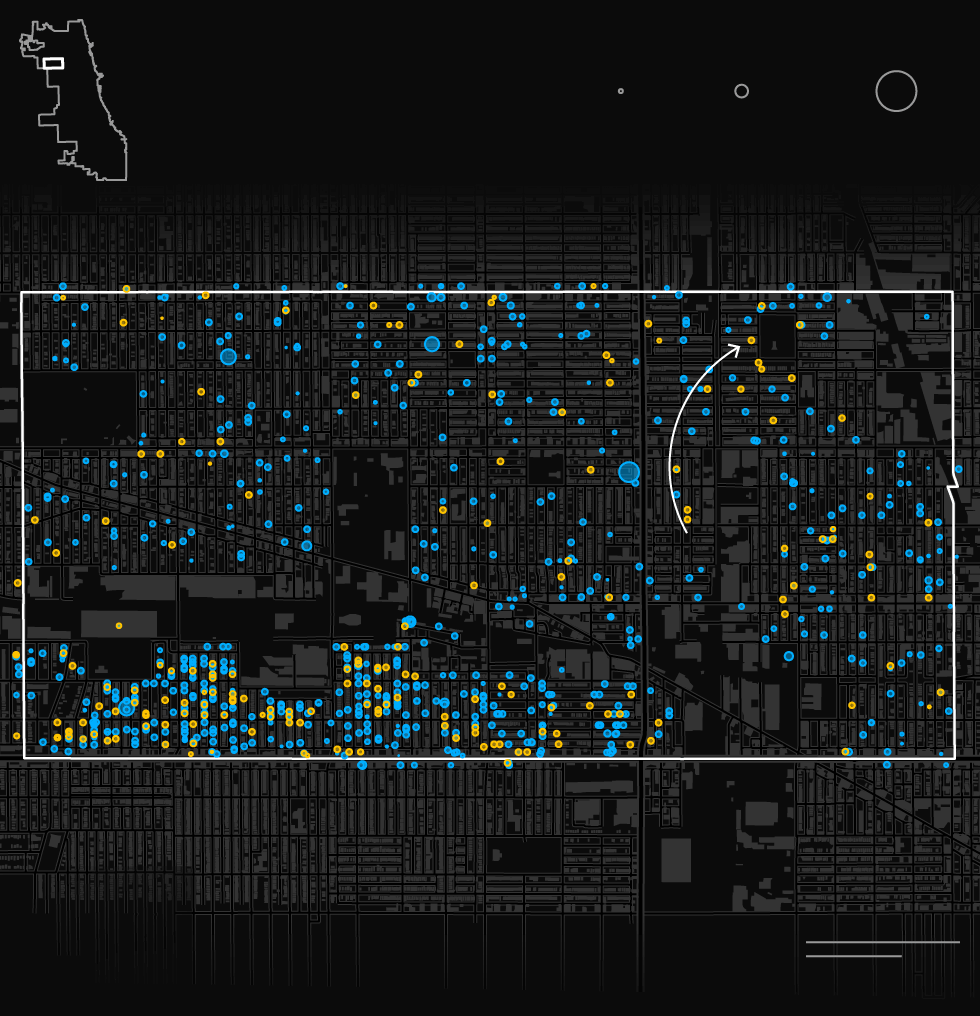

Zip code 60622

April 2021

$10K

Loan amount:

$100K

$1M

W Armitage Ave

The average loan fell to $25,000 from nearly $125,000 in April 2020, with fewer restaurant recipients.

Logan Square

Wicker

Park

W North Ave

90

N Kedzie Ave

N California Ave

N Western Ave

N Damen Ave

N Ashland Ave

N MilwaukeeAve

W Division Ave

Humboldt

Park

East

Village

Ukrainian

Village

Noble

Square

W Chicago Ave

West Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2021

$1M

Loan amount:

$10K

$100K

W Armitage Ave

The average loan fell to $25,000 from nearly $125,000 in April 2020, with fewer restaurant recipients.

Logan

Square

Wicker

Park

W North Ave

N Kedzie Ave

N Ashland Ave

N California Ave

N Western Ave

N Damen Ave

N MilwaukeeAve

90

Humboldt

Park

East

Village

Ukrainian

Village

Noble

Square

W Chicago Ave

West

Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2021

Loan amount:

$10K

$100K

$1M

The average loan fell to $25,000 from nearly $125,000 in April 2020, with fewer restaurant recipients.

W Armitage Ave

Logan

Square

Wicker

Park

W North Ave

N Ashland Ave

N Kedzie Ave

N California Ave

N Western Ave

N MilwaukeeAve

90

Humboldt

Park

Ukrainian

Village

Noble

Square

W Chicago Ave

West

Town

W Hubbard Ave

.25 mile

.25 km

Zip code 60622

April 2021

Loan amount:

$10K

$100K

$1M

W Armitage Ave

Logan Square

Wicker

Park

W North Ave

N Kedzie Ave

N Ashland Ave

90

Ukrainian

Village

W Chicago Ave

West

Town

The average loan fell to $25,000 from nearly $125,000 in April 2020, with fewer restaurant recipients.

.5 mile

.5 km

Zip code 60622

April 2021

Loan amount:

$10K

$100K

$1M

W Armitage Ave

Logan Square

Wicker

Park

W North Ave

N Ashland Ave

N Kedzie Ave

90

Ukrainian

Village

W Chicago Ave

West

Town

The average loan fell to $25,000 from nearly $125,000 in April 2020, with fewer restaurant recipients.

.5 mile

.5 km

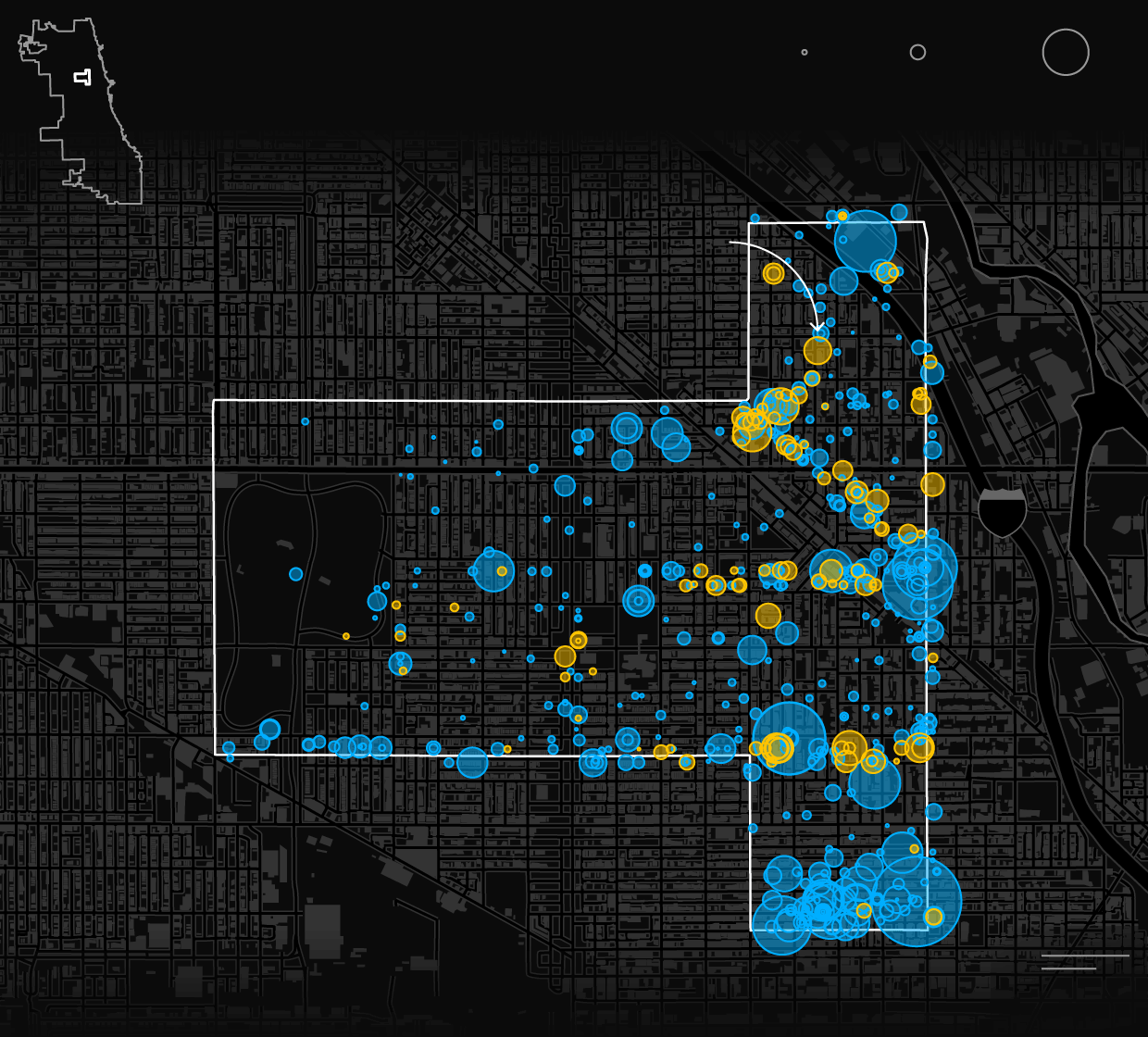

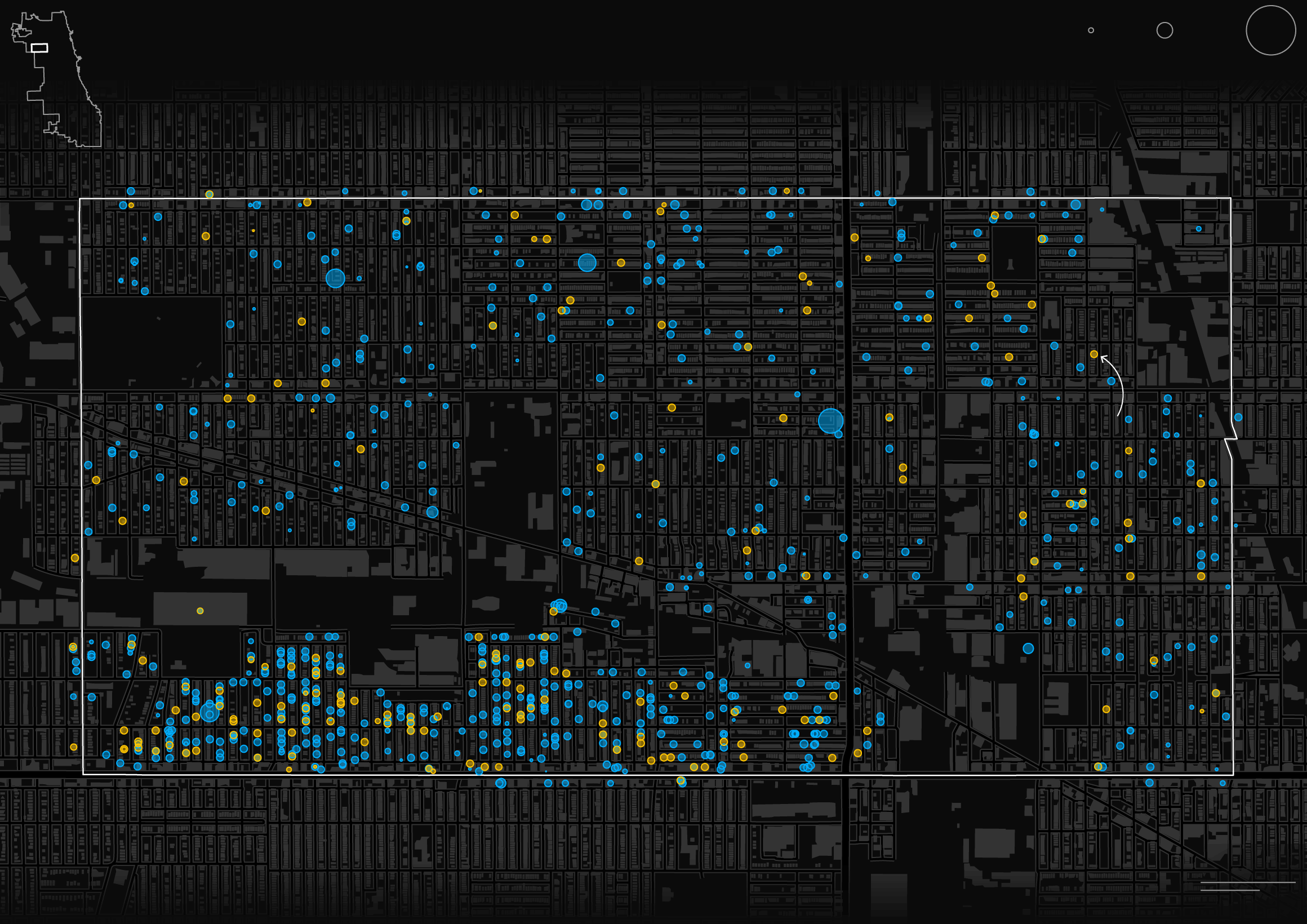

Zip code 60649

April 2020

$10K

Loan amount:

$100K

$1M

Jackson Park

Woodlawn

Just four borrowers, several in construction plus a nursing home, represented almost half of all the money this month.

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South Shore

E 75th St

S Stony Island Ave

S Jeffery Blvd

S Yates Blvd

S Exchange Ave

90

E 79th St

Avalon

Park

South Chicago

.25 mile

.25 km

Zip code 60649

April 2020

$1M

Loan amount:

$10K

$100K

Jackson

Park

Woodlawn

Just four borrowers, several in construction plus a nursing home, represented almost half of all the money this month.

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South Shore

E 75th St

S Stony Island Ave

S Jeffery Blvd

S Yates Blvd

S Exchange Ave

90

E 79th St

Avalon

Park

South Chicago

.25 mile

.25 km

Zip code 60649

April 2020

Loan amount:

$10K

$100K

$1M

Just four borrowers, several in construction plus a nursing home, represented almost half of all the money this month.

Jackson

Park

Woodlawn

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South

Shore

S Stony Island Ave

E 75th St

S Exchange Ave

S Jeffery Blvd

S Yates Blvd

90

E 79th St

Avalon

Park

.25 mile

South Chicago

.25 km

Zip code 60649

April 2020

Loan amount:

$10K

$100K

$1M

Jackson

Park

Just four borrowers, several in construction plus a nursing home, represented almost half of all the money this month.

E 67th St

S Stony Island Ave

Lake Michigan

South

Shore

S South Shore Dr

90

E 79th St

Avalon

Park

South Chicago

.5 mile

.5 km

Zip code 60649

April 2020

Loan amount:

$10K

$100K

$1M

Just four borrowers, several in construction plus a nursing home, represented almost half of all the money this month.

Jackson

Park

E 67th St

S Stony Island Ave

Lake Michigan

South

Shore

S South Shore Dr

90

E 79th St

Avalon

Park

.5 mile

South Chicago

.5 km

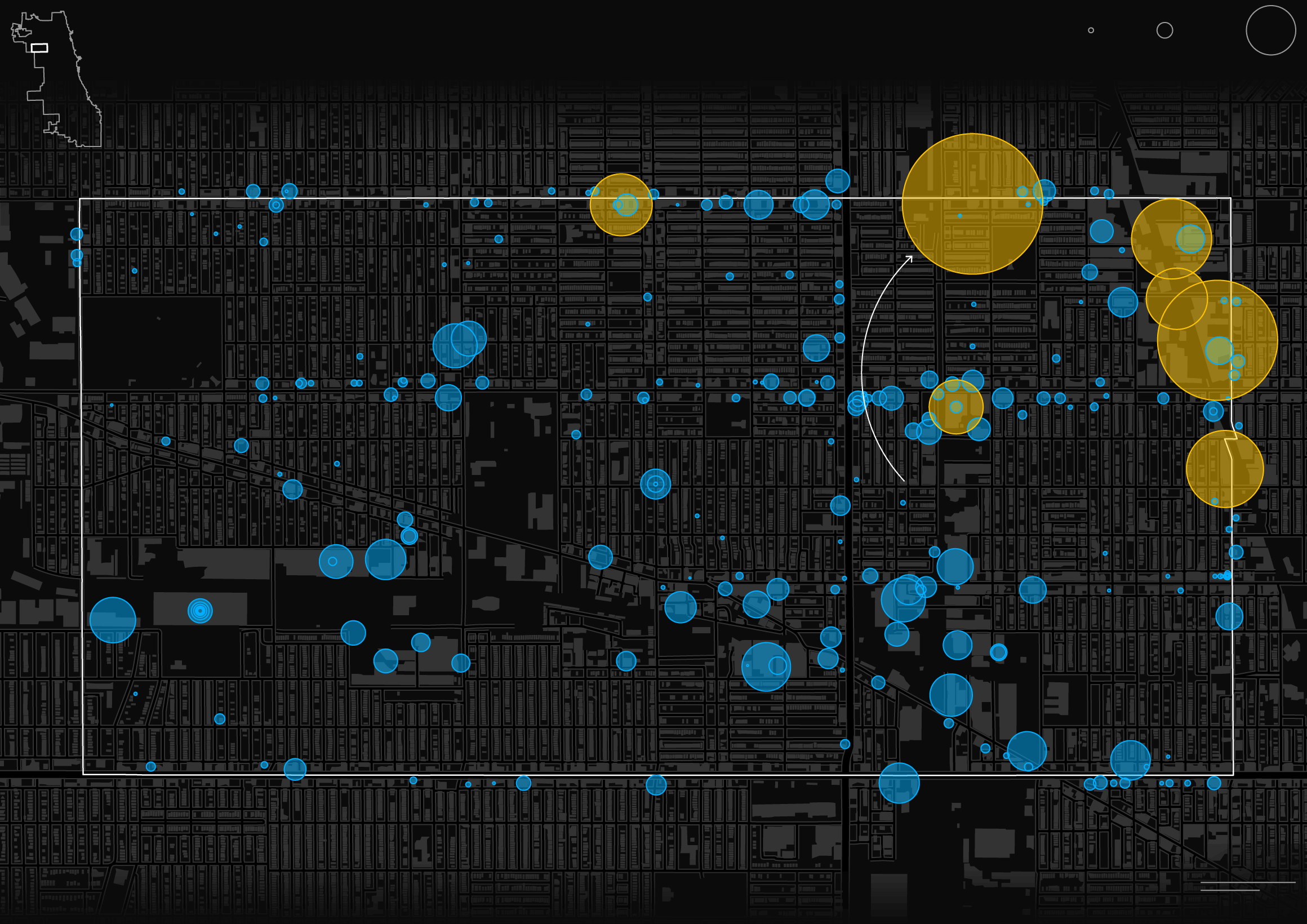

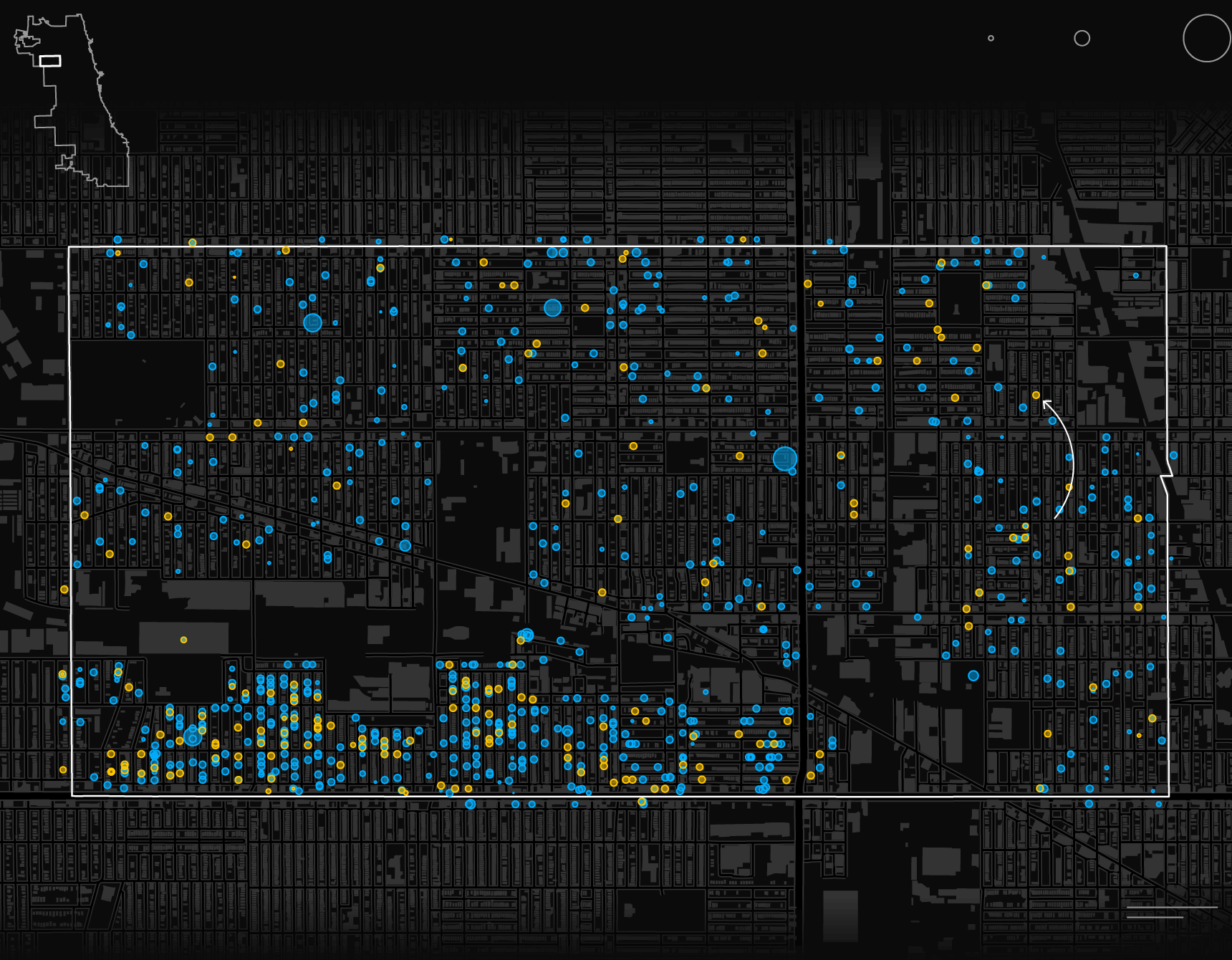

Zip code 60649

April 2021

$10K

Loan amount:

$100K

$1M

Jackson Park

Woodlawn

More than 500 loans, totalling about $10 million, went to beauty salons and barber shops.

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South Shore

E 75th St

S Stony Island Ave

S Jeffery Blvd

S Yates Blvd

S Exchange Ave

90

E 79th St

Avalon

Park

South Chicago

.25 mile

.25 km

Zip code 60649

April 2021

$1M

Loan amount:

$10K

$100K

Jackson

Park

Woodlawn

More than 500 loans, totalling about $10 million, went to beauty salons and barber shops.

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South Shore

E 75th St

S Stony Island Ave

S Jeffery Blvd

S Yates Blvd

S Exchange Ave

90

E 79th St

Avalon

Park

South Chicago

.25 mile

.25 km

Zip code 60649

April 2021

Loan amount:

$10K

$100K

$1M

More than 500 loans, totalling about $10 million, went to beauty salons and barber shops.

Jackson

Park

Woodlawn

E 67th St

E 71st St

S South Shore Dr

Lake Michigan

Grand

Crossing

South

Shore

S Stony Island Ave

E 75th St

S Exchange Ave

S Jeffery Blvd

S Yates Blvd

90

Avalon

Park

E 79th St

.25 mile

South Chicago

.25 km

Zip code 60649

April 2021

Loan amount:

$10K

$100K

$1M

Jackson

Park

More than 500 loans, totalling about $10 million, went to beauty salons and barber shops.

E 67th St

S Stony Island Ave

Lake Michigan

South

Shore

S South Shore Dr

90

E 79th St

Avalon

Park

South Chicago

.5 mile

.5 km

Zip code 60649

April 2021

Loan amount:

$10K

$100K

$1M

More than 500 loans, totalling about $10 million, went to beauty salons and barber shops.

Jackson

Park

E 67th St

S Stony Island Ave

Lake Michigan

South

Shore

S South Shore Dr

90

E 79th St

Avalon

Park

.5 mile

South Chicago

.5 km

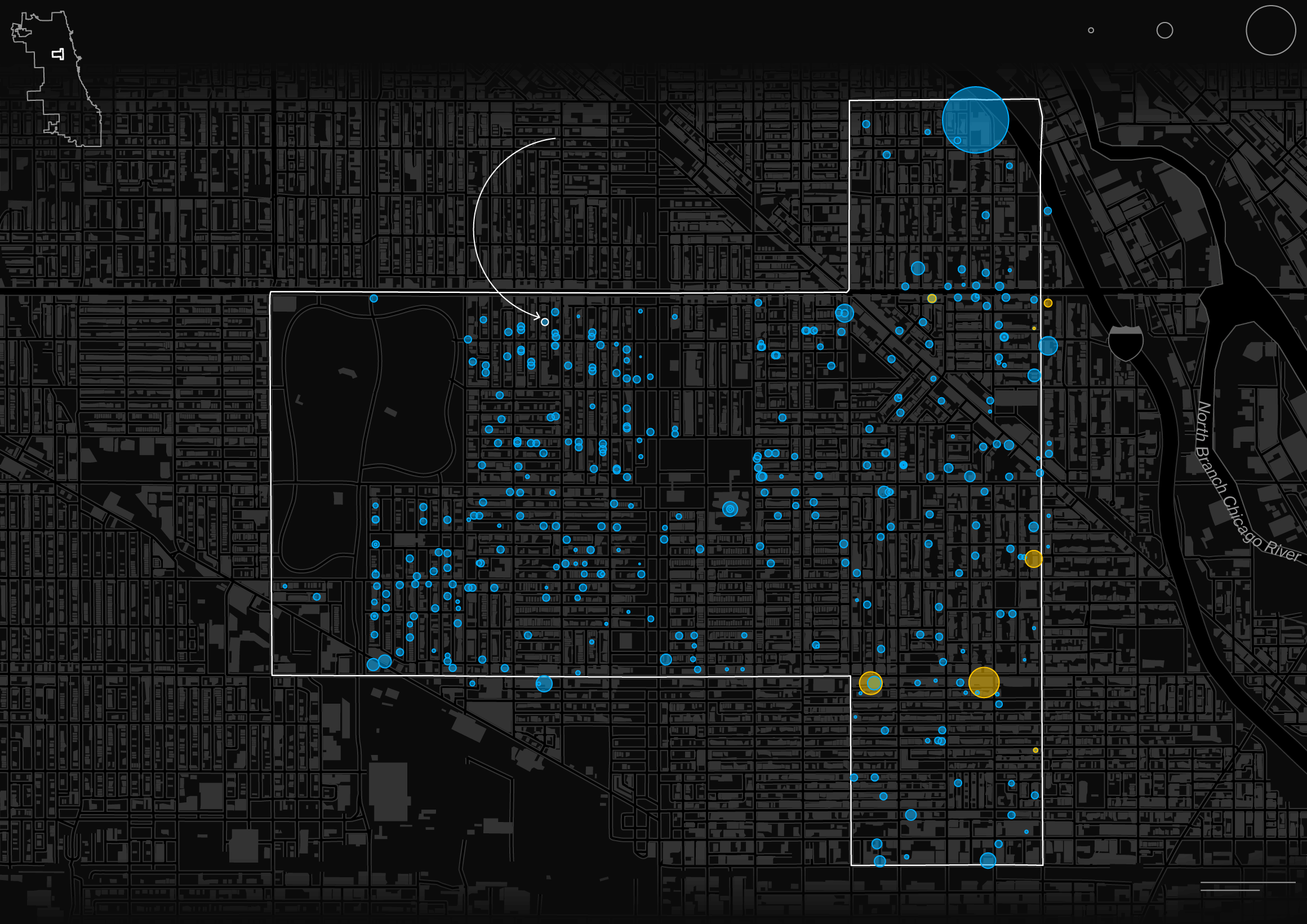

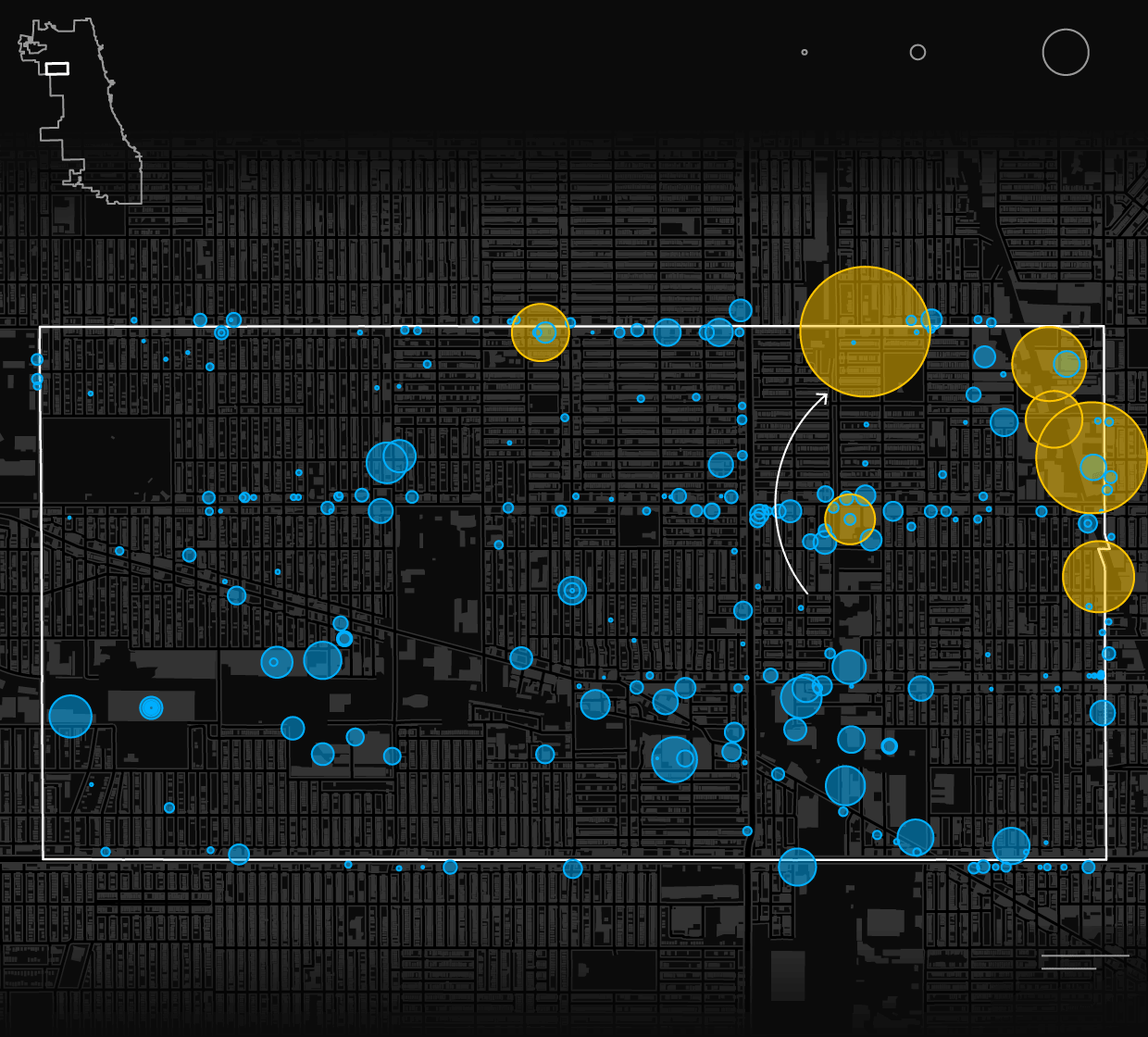

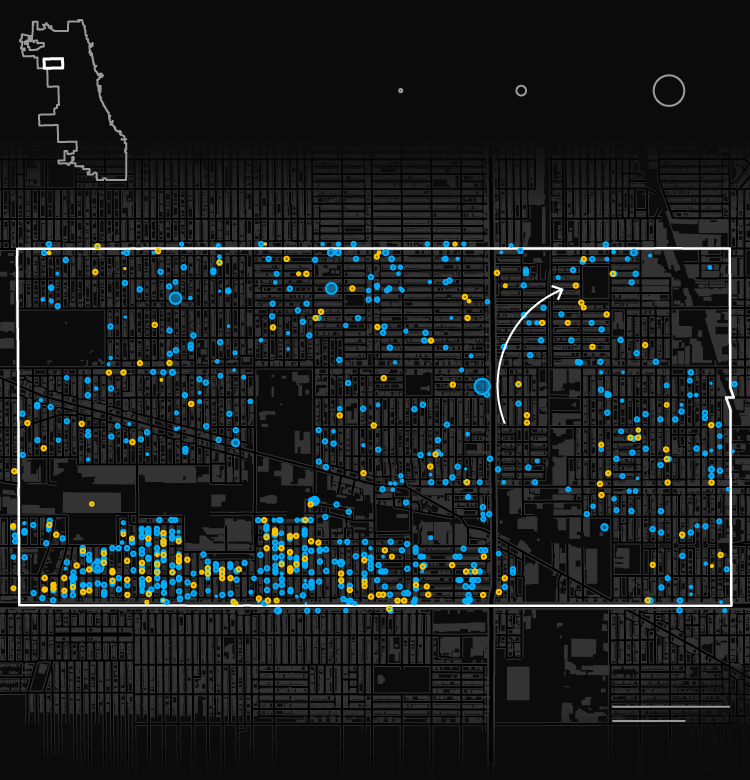

Zip code 60639

April 2020

$10K

Loan amount:

$100K

$1M

Avondale

W Diversey Ave

Hermosa

Belmont Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

Several borrowers in this zip code received seven-figure loans in this round, pushing the average to more than $190,000.

N Narragansett Ave

N Central Ave

W Grand Ave

W Armitage Ave

N Pulaski Rd

W North Ave

Austin

Humboldt Park

.25 mile

.25 km

Zip code 60639

April 2020

$1M

Loan amount:

$10K

$100K

Avondale

W Diversey Ave

Hermosa

Belmont Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

N Narragansett Ave

W Grand Ave

Several borrowers in this zip code received seven-figure loans in this round, pushing the average to more than $190,000.

N Central Ave

N Pulaski Rd

W North Ave

Humboldt

Park

Austin

.25 mile

.25 km

Zip code 60639

April 2020

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

Hermosa

Belmont

Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

N Narragansett Ave

W Grand Ave

Several borrowers in this zip code received seven-figure loans in this round.

N Central Ave

N Pulaski Rd

W North Ave

Humboldt

Park

.25 mile

Austin

.25 km

Zip code 60639

April 2020

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

N Narragansett Ave

Belmont

Cragin

Hermosa

Several borrowers in this zip code received seven-figure loans in this round.

W North Ave

Austin

.5 mile

.5 km

Zip code 60639

April 2020

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

N Narragansett Ave

Belmont

Cragin

Hermosa

Several borrowers in this zip code received seven-figure loans in this round.

W North Ave

Austin

.5 mile

.5 km

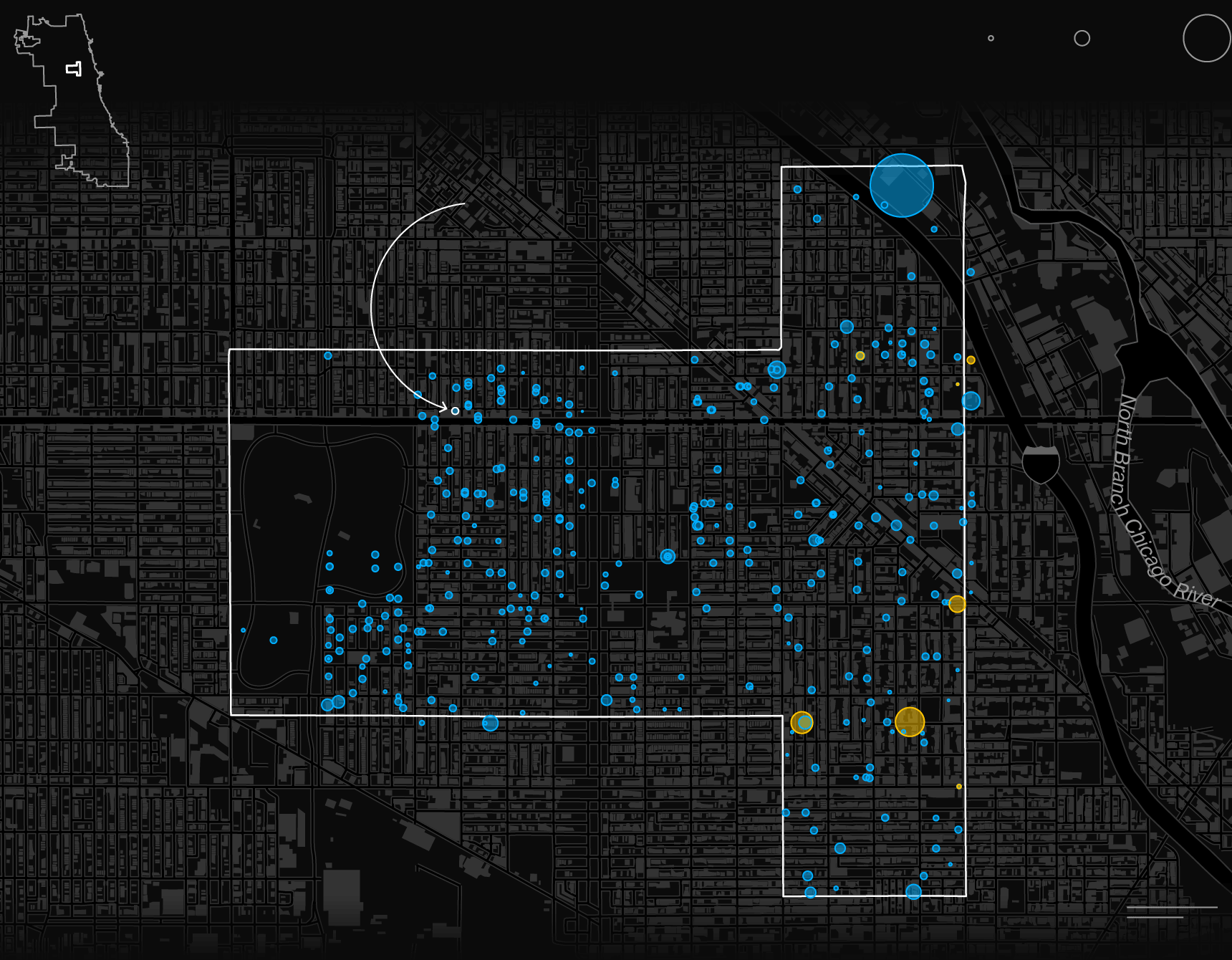

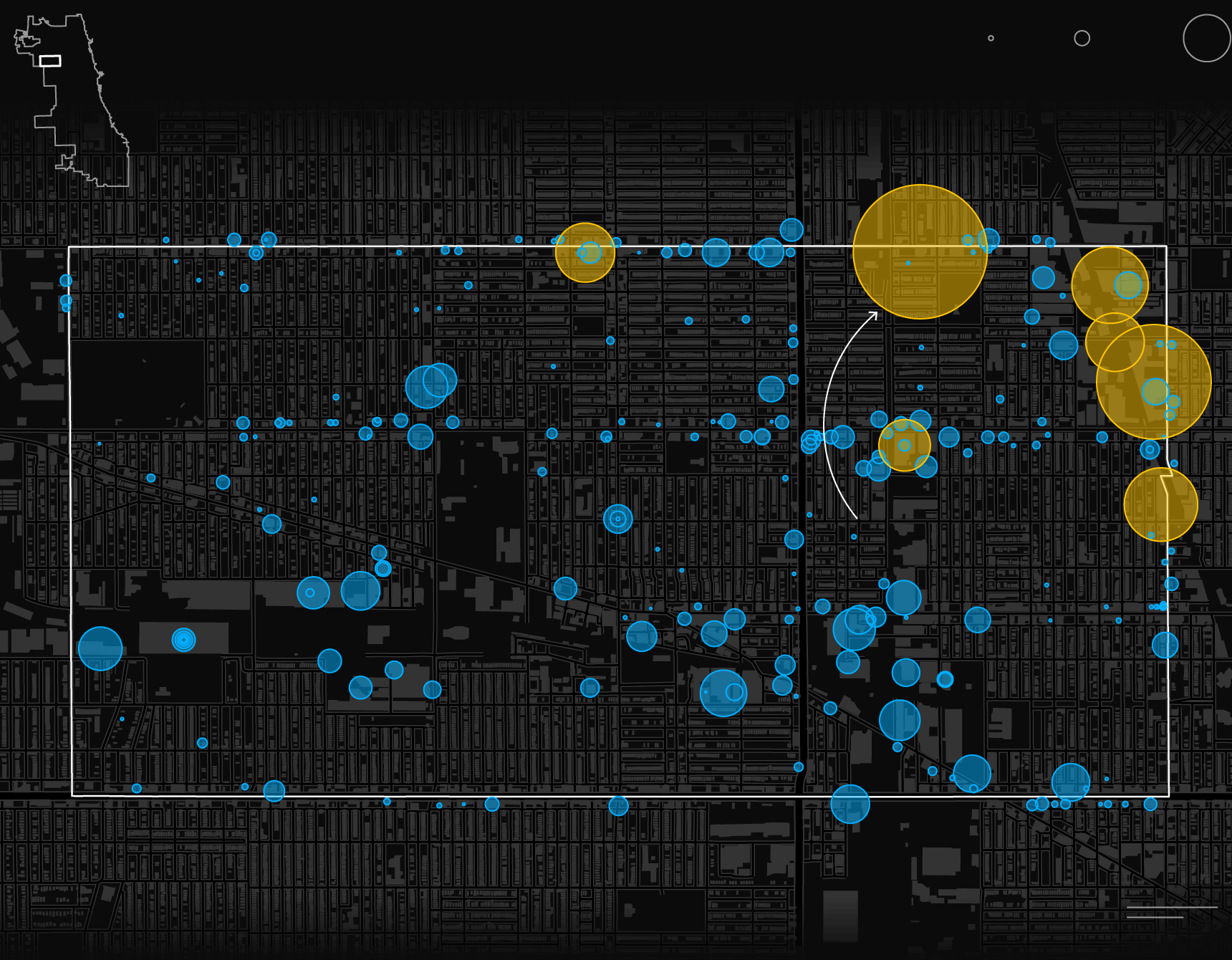

Zip code 60639

April 2021

$10K

Loan amount:

$100K

$1M

Avondale

W Diversey Ave

Hermosa

Belmont Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

Here, barber shops and beauty salons were also the most common PPP recipients this month.

N Narragansett Ave

N Central Ave

W Grand Ave

W Armitage Ave

N Pulaski Rd

W North Ave

Austin

Humboldt Park

.25 mile

.25 km

Zip code 60639

April 2021

$1M

Loan amount:

$10K

$100K

Avondale

W Diversey Ave

Hermosa

Belmont Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

N Narragansett Ave

W Grand Ave

Here, barber shops and beauty salons were also the most common PPP recipients this month.

N Central Ave

N Pulaski Rd

W North Ave

Humboldt

Park

Austin

.25 mile

.25 km

Zip code 60639

April 2021

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

Hermosa

Belmont

Cragin

N Laramie Ave

N Cicero Ave

N Kostner Ave

W Fullerton Ave

N Narragansett Ave

W Grand Ave

Here, barber shops and beauty salons were also the most common PPP recipients this month.

N Central Ave

N Pulaski Rd

W North Ave

Humboldt

Park

.25 mile

Austin

.25 km

Zip code 60639

April 2021

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

N Narragansett Ave

Belmont

Cragin

Hermosa

Here, barber shops and beauty salons were also the most common PPP recipients this month.

W North Ave

Austin

.5 mile

.5 km

Zip code 60639

April 2021

Loan amount:

$10K

$100K

$1M

Avondale

W Diversey Ave

N Narragansett Ave

Belmont

Cragin

Hermosa

Here, barber shops and beauty salons were also the most common PPP recipients this month.

W North Ave

Austin

.5 mile

.5 km

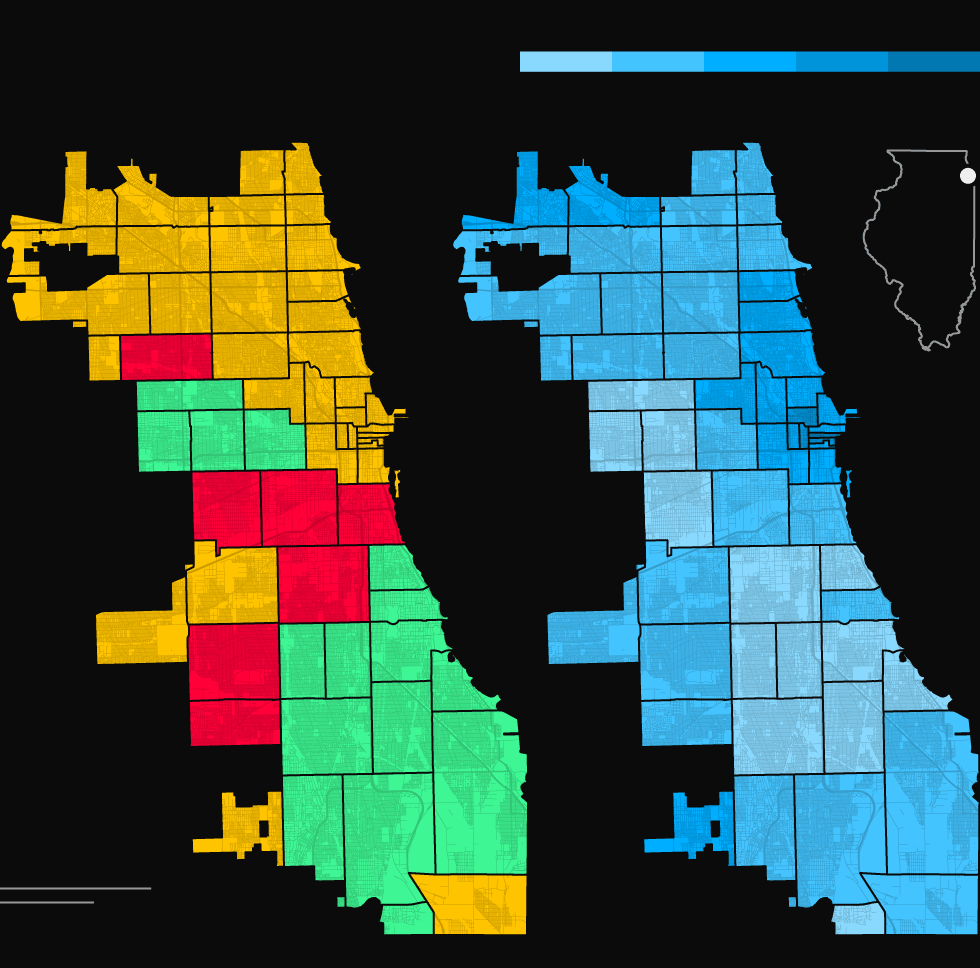

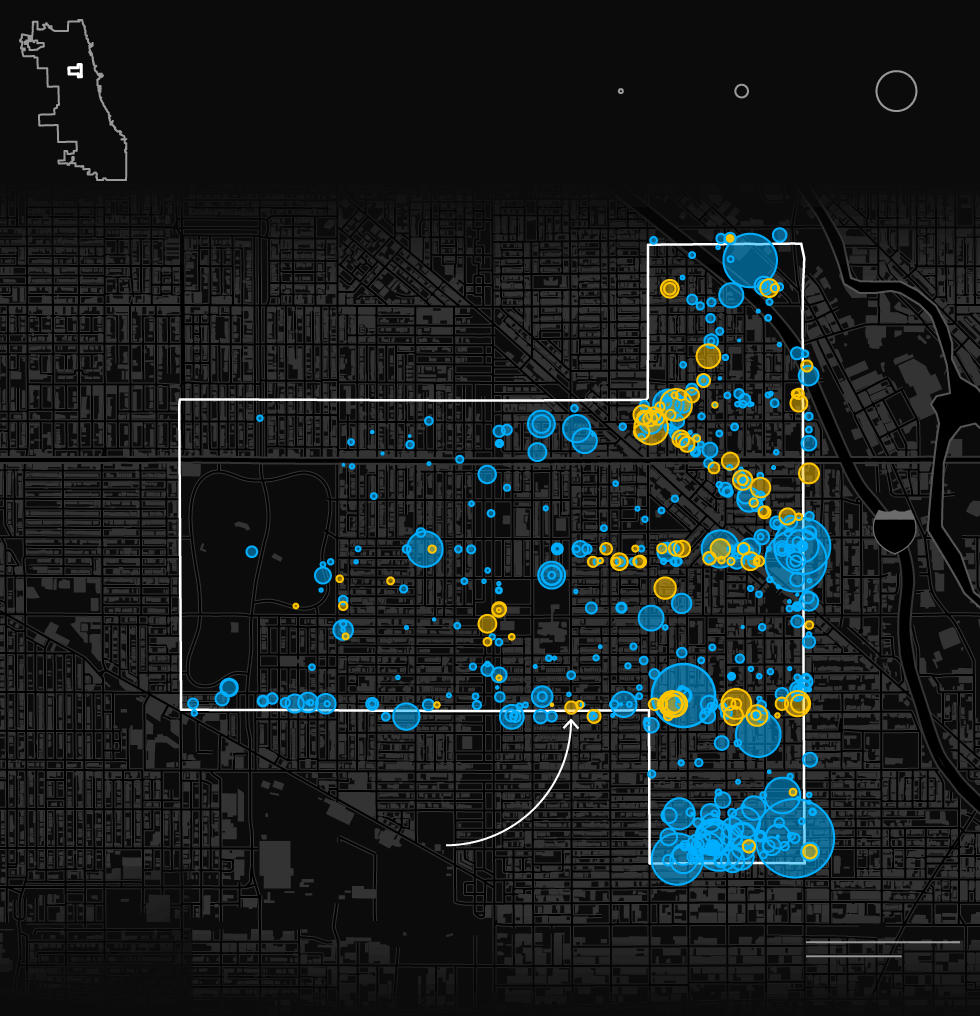

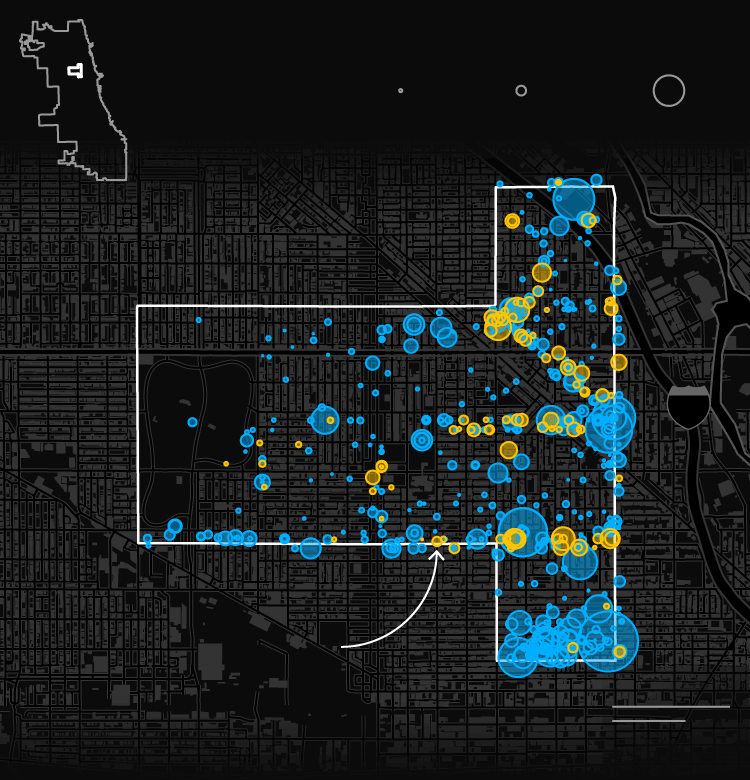

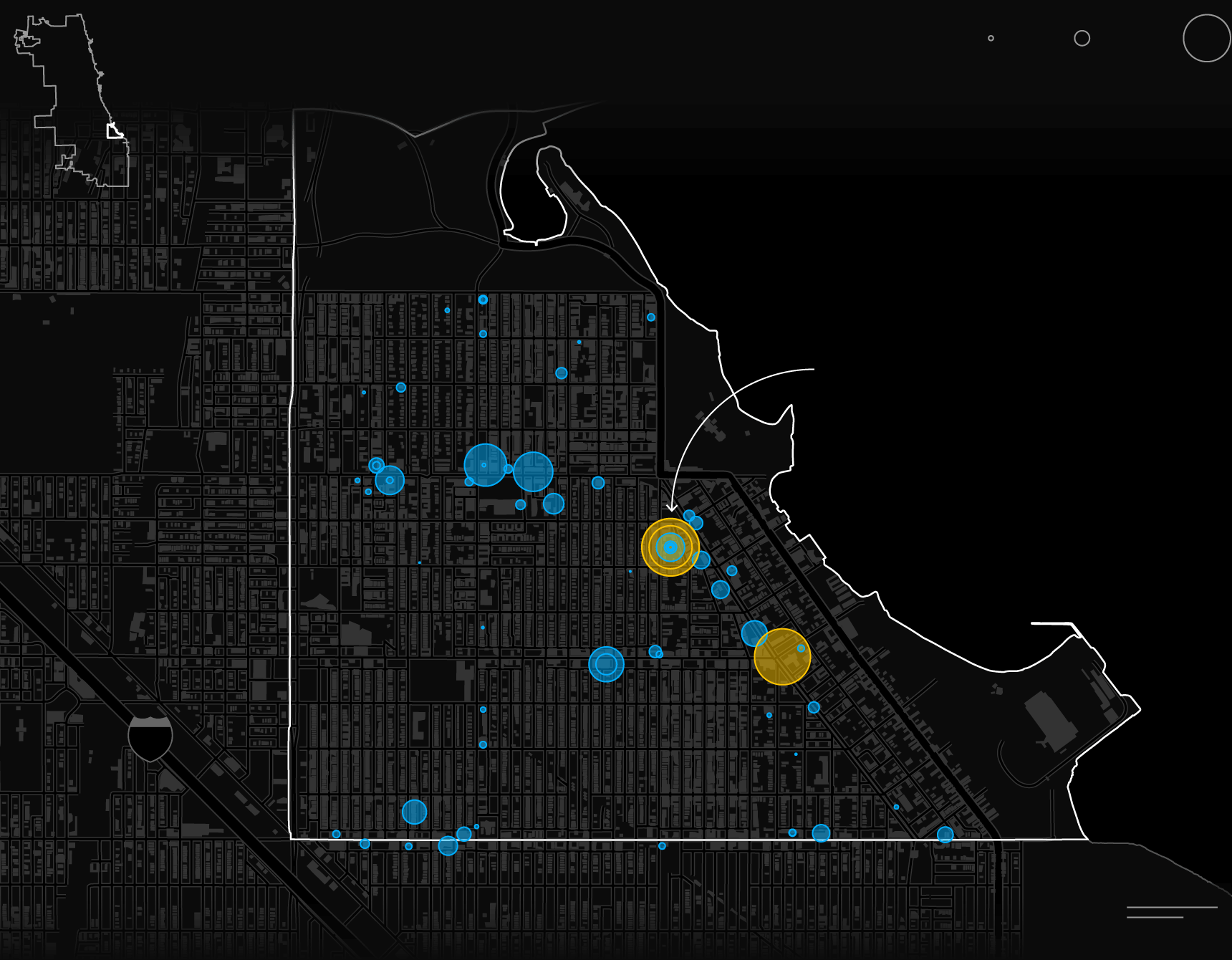

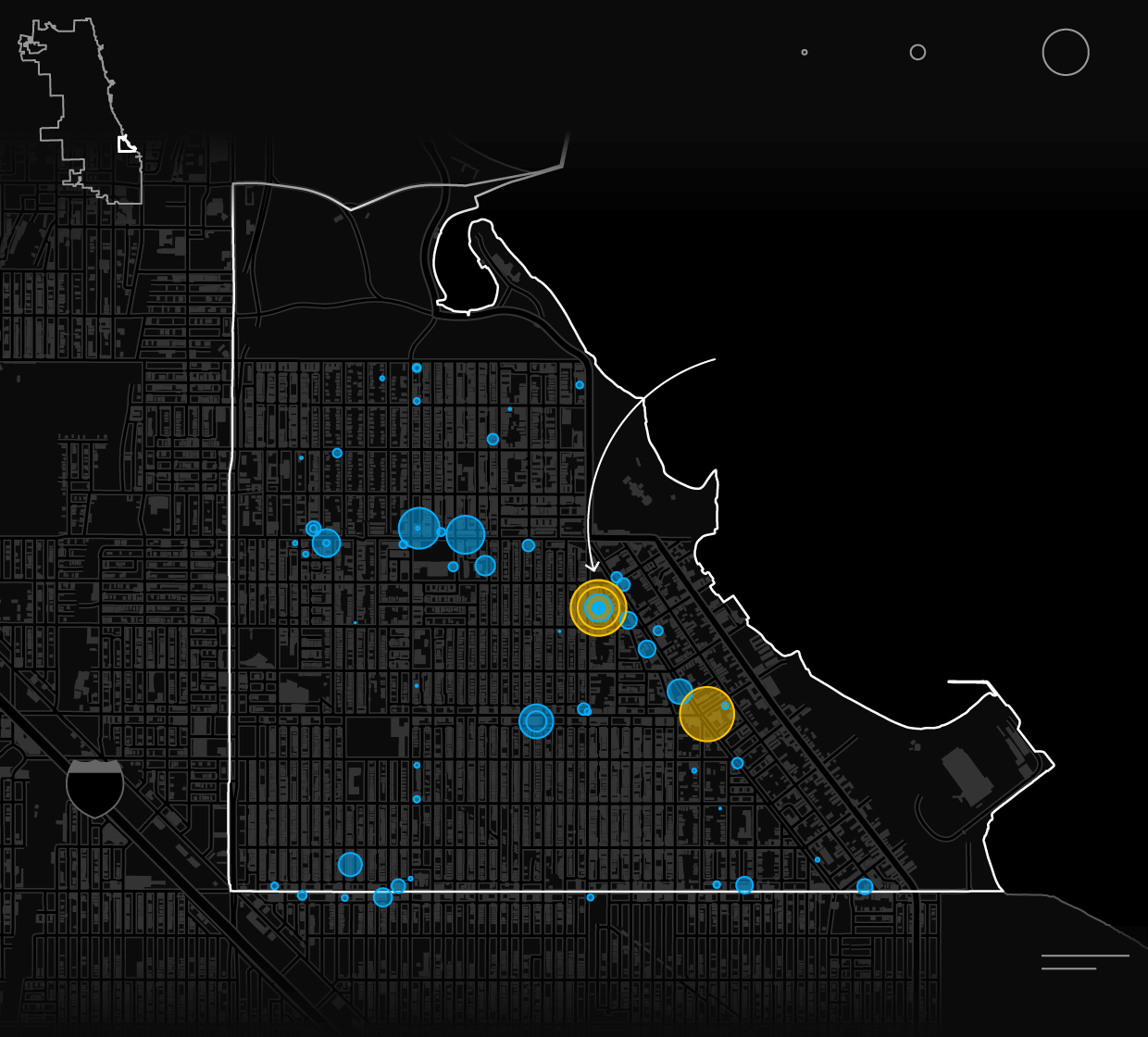

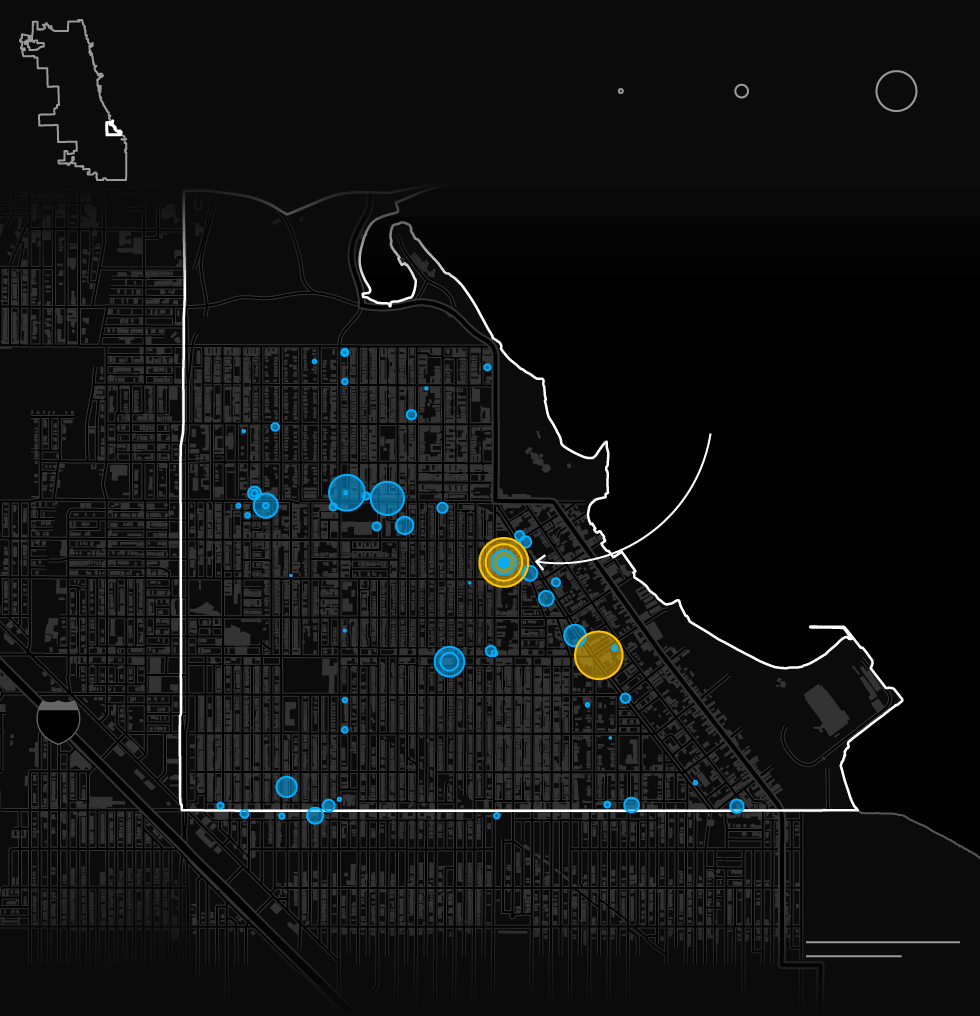

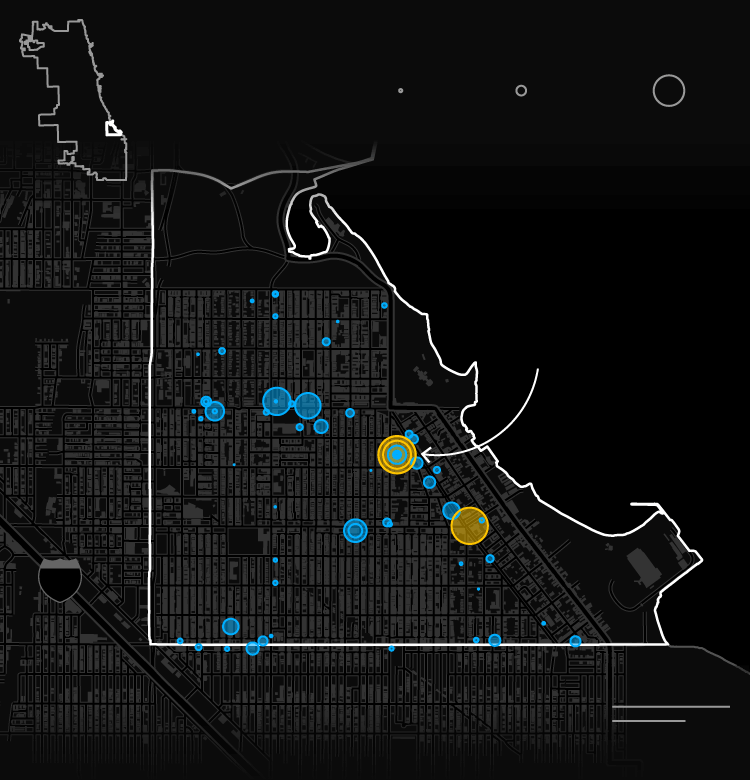

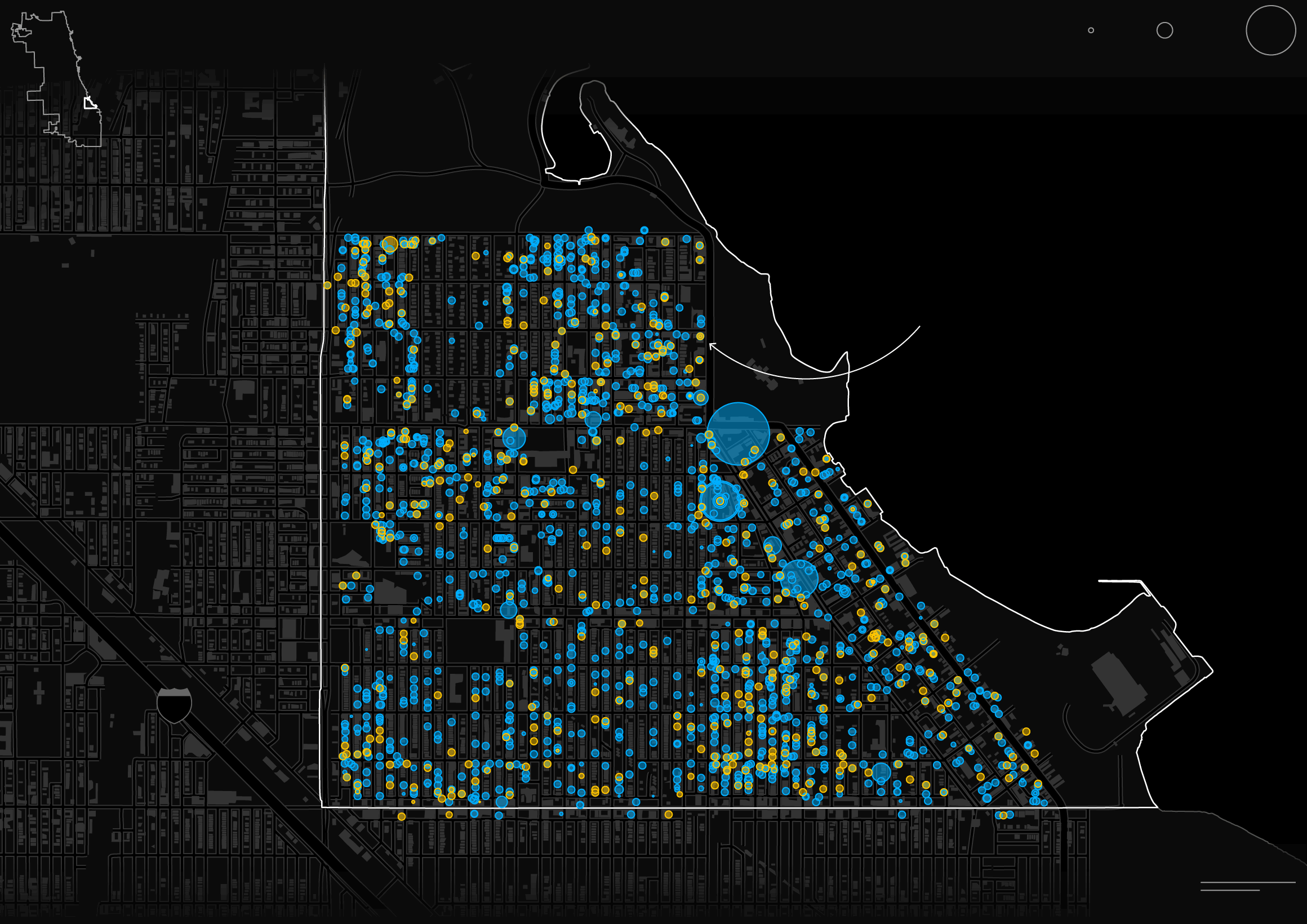

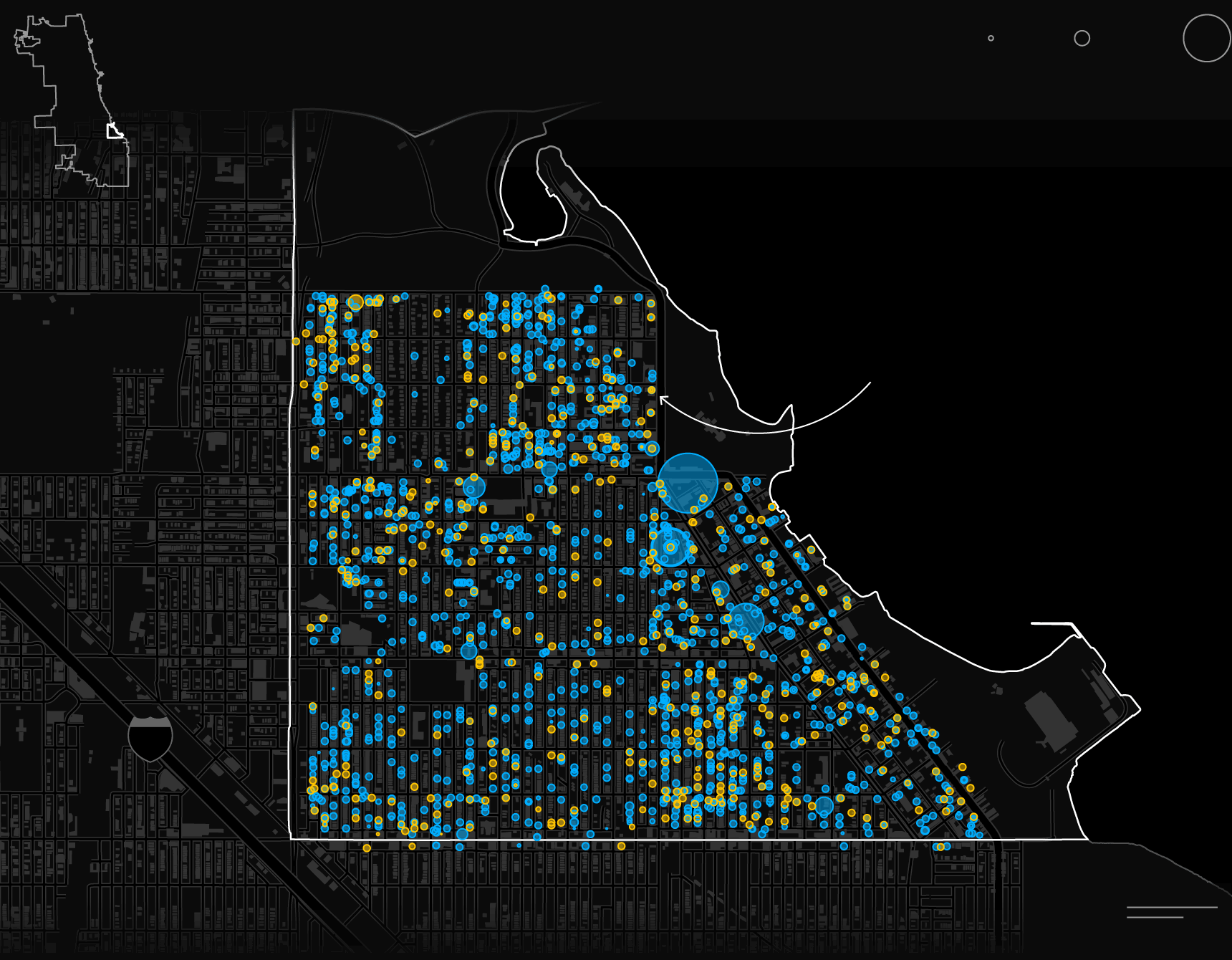

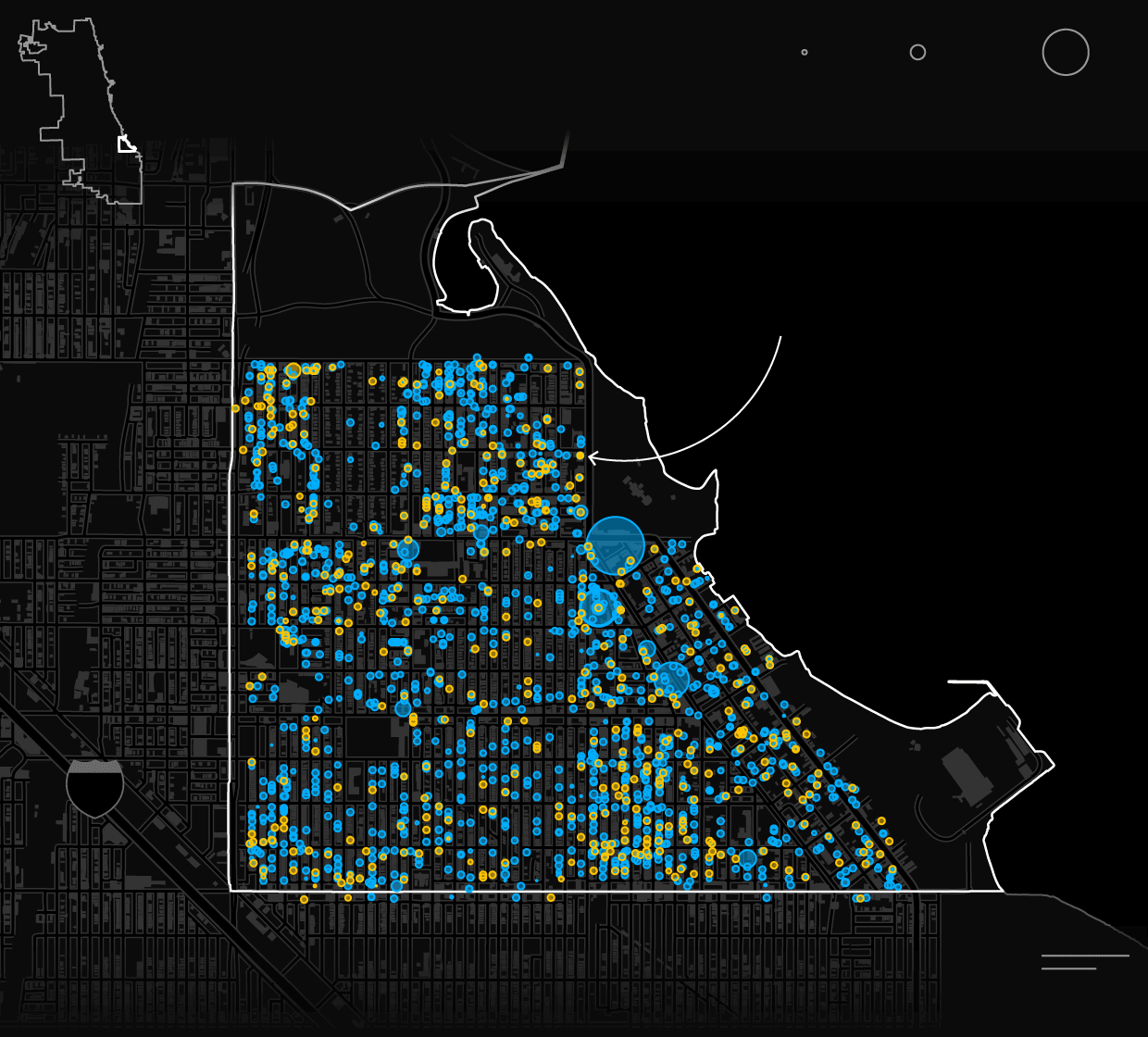

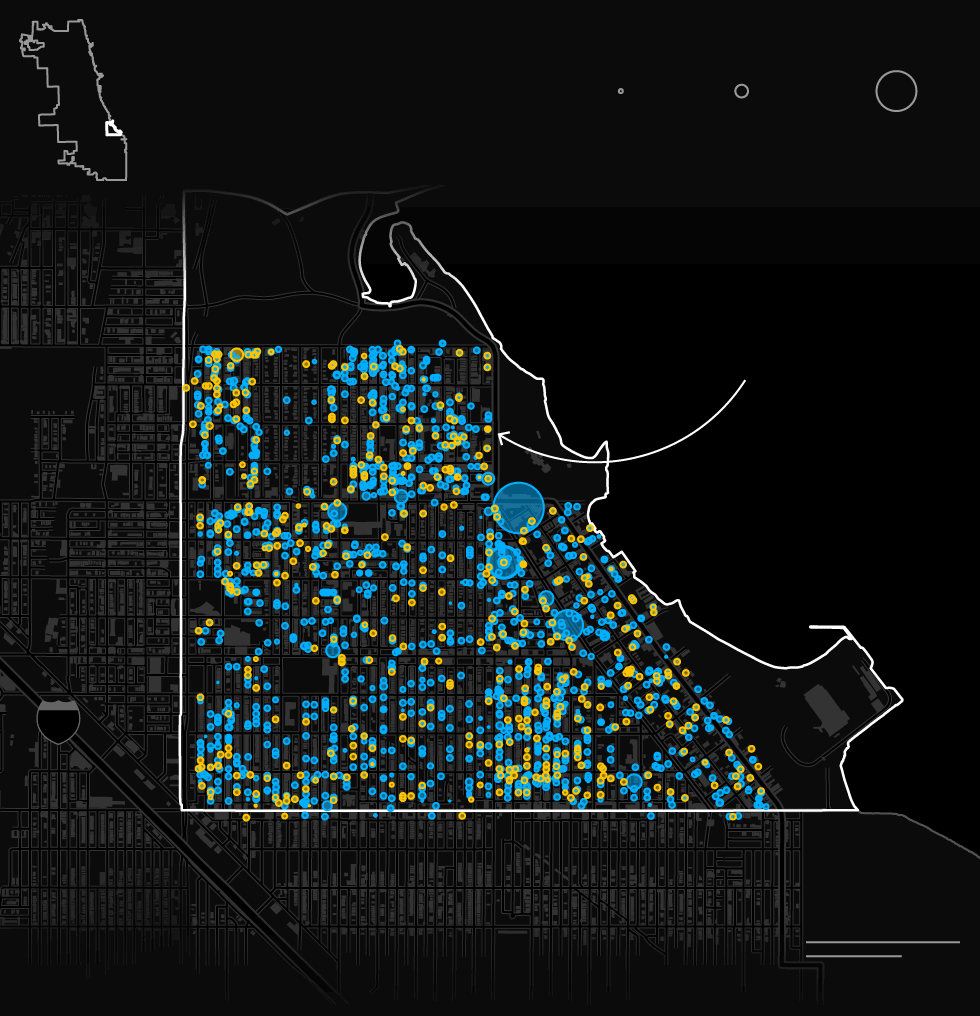

Chicago’s Differing PPP Rollouts

Three zip codes overlapping with Mayor Lori Lightfoot’s Invest South/West economic program illustrate how the Paycheck Protection Program helped Chicago’s major racial and ethnic groups differently.

Early PPP Rounds Favored Richer, Whiter Areas

This majority-White zip code in West Town, with a median household income of just over $100,000 received 39% of all its PPP money at the start of the program in April 2020, plus an additional 16% the month after. That’s a considerably higher share than for the other two zip codes.

Later PPP Loans Were Smaller

By the time the Biden administration made changes to the final round of PPP loans in February 2021, focusing on minority-owned and smaller businesses, this area had already received almost all of its relief money—$149 million. Those changes proved more meaningful to non-White zip codes, many of which saw a bump in funds.

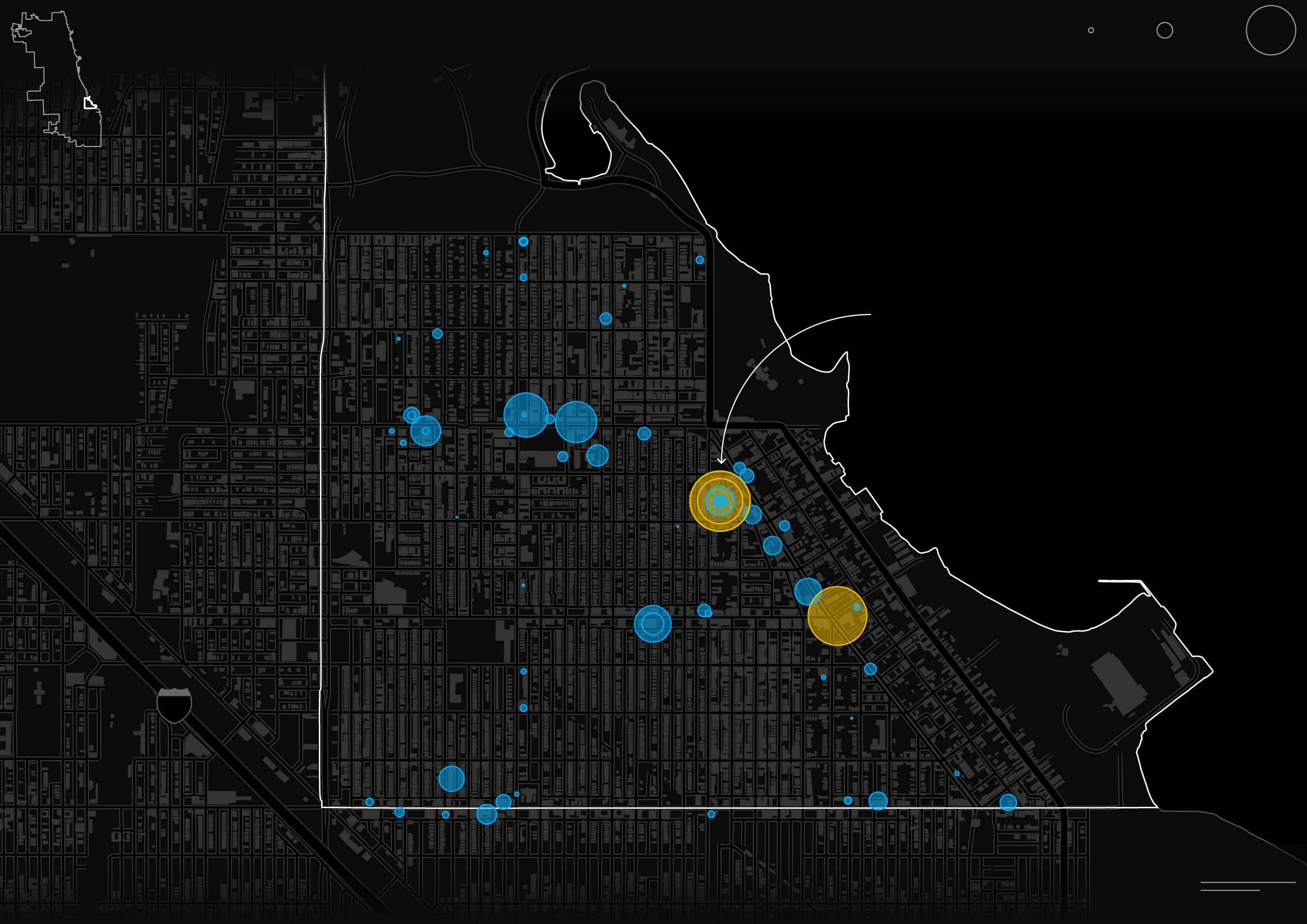

Some Minority Areas Were Overlooked in 2020

This zip code in the majority-Black South Shore neighborhood, with a median income of less than $32,000, has received almost as much total PPP money—$318 million per 100,000 residents—as the wealthier West Town zip code. But little of that came last year when the program favored larger and better-connected businesses.

Loans to Majority-Black Areas Peaked in April 2021

One year later, this neighborhood, bordering Lake Michigan, was blanketed in more than 2,400 PPP loans, representing more than a third of all the money it received. Most Black-owned small businesses are sole proprietorships who don’t have direct employees and many don’t have experience with traditional banking systems. Residential addresses were more likely to be listed on loan applications, compared to earlier rounds.

Hispanic Areas Received the Least of All

Over in the Belmont Cragin neighborhood, this zip code, which is at least 73% Hispanic and has a slightly higher median household income of around $46,000, ultimately got about half as much PPP money as the other two zip codes, a pattern seen across majority-Hispanic areas of Chicago.

Smallest Businesses Dominated Final PPP Round

This neighborhood received three times as many PPP loans in April 2021 as the prior April, but they were collectively worth just 36% as much.

The PPP was never meant to single-handedly save the economy from the ravages of Covid-19. And in earlier rounds, larger loans that were tagged to companies’ headquarters in majority-White zip codes probably flowed to some individual stores or franchises in minority neighborhoods—meaning the Bloomberg analysis likely undercounts how much financial support some areas got. State and local programs also provided funds.

One long-running problem for smaller and minority-owned businesses is the lack of established relationships with banks that distributed the PPP forgivable loans. A similar lag in federal aid can be seen in U.S. metro areas including Dallas, Houston, Los Angeles and Philadelphia, data show.

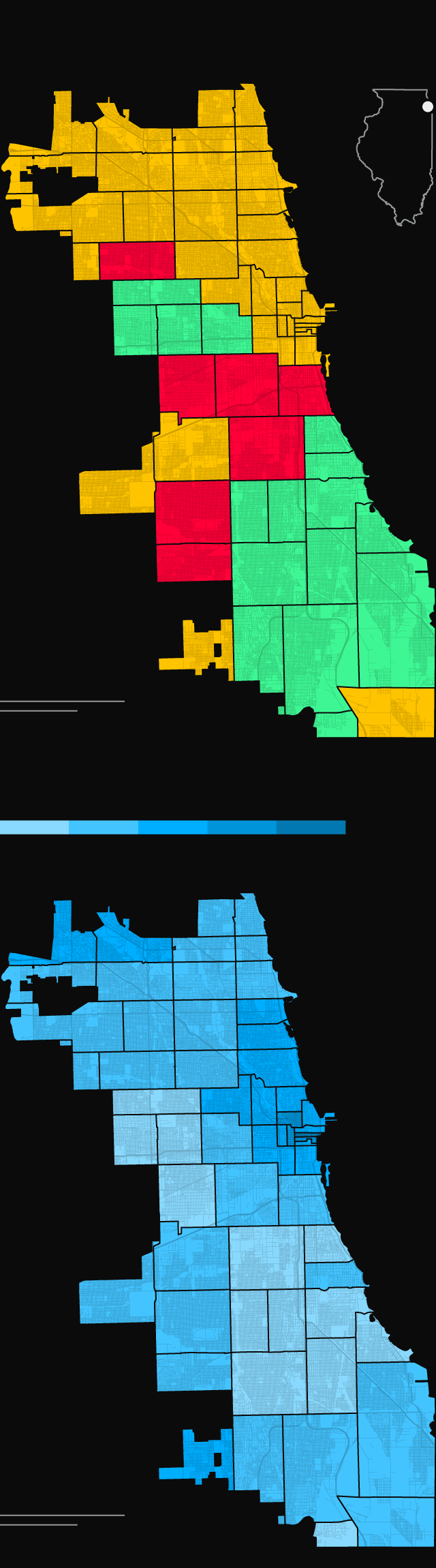

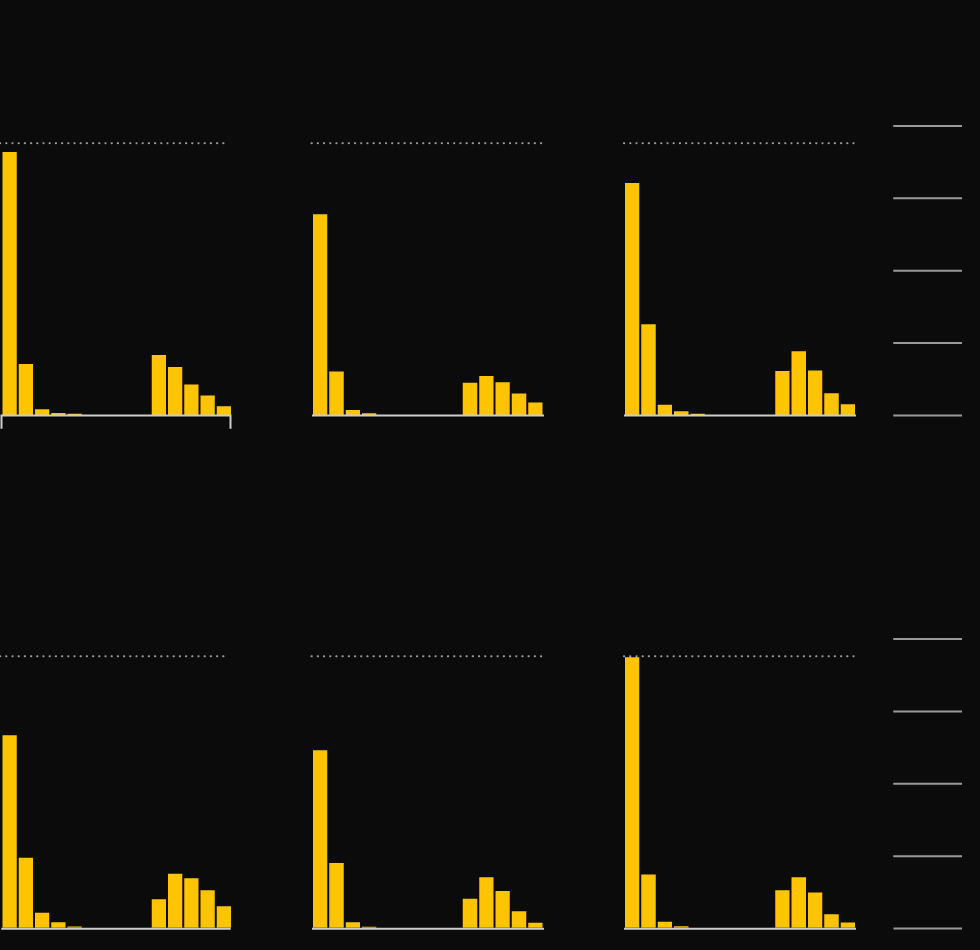

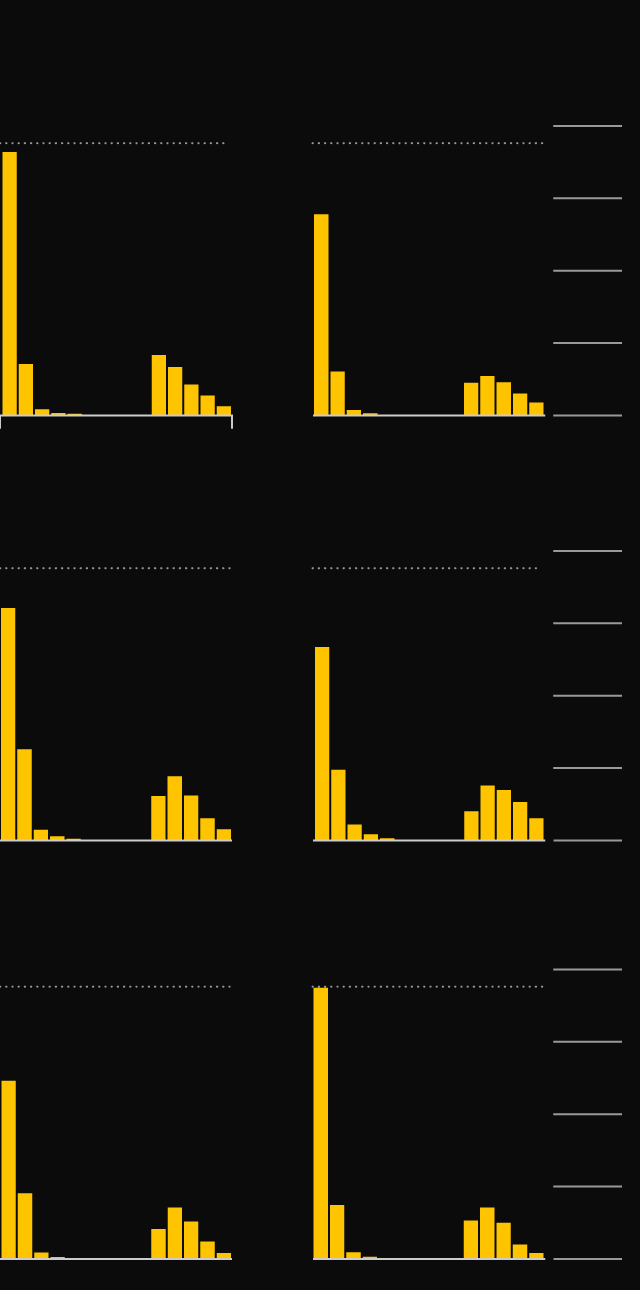

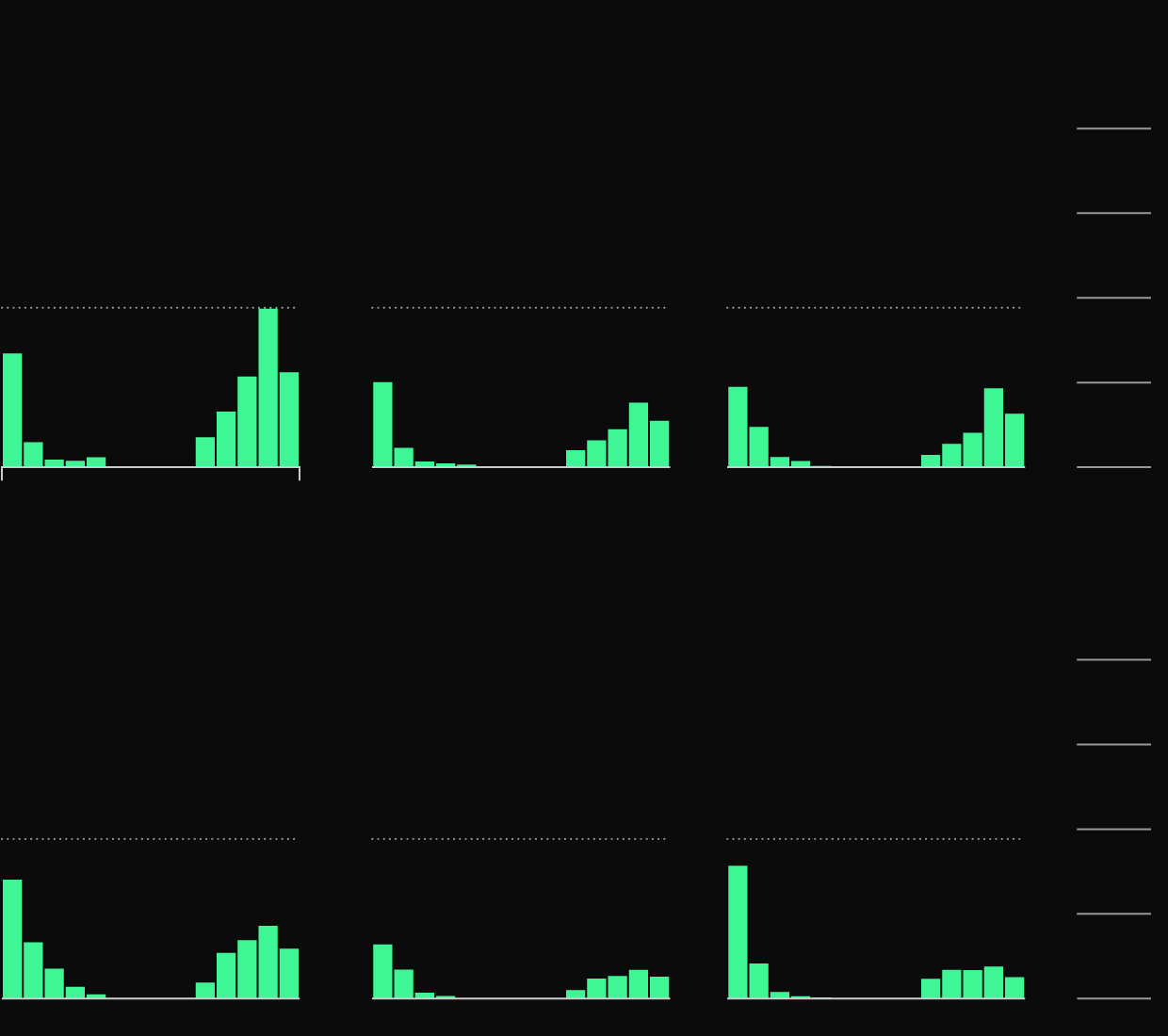

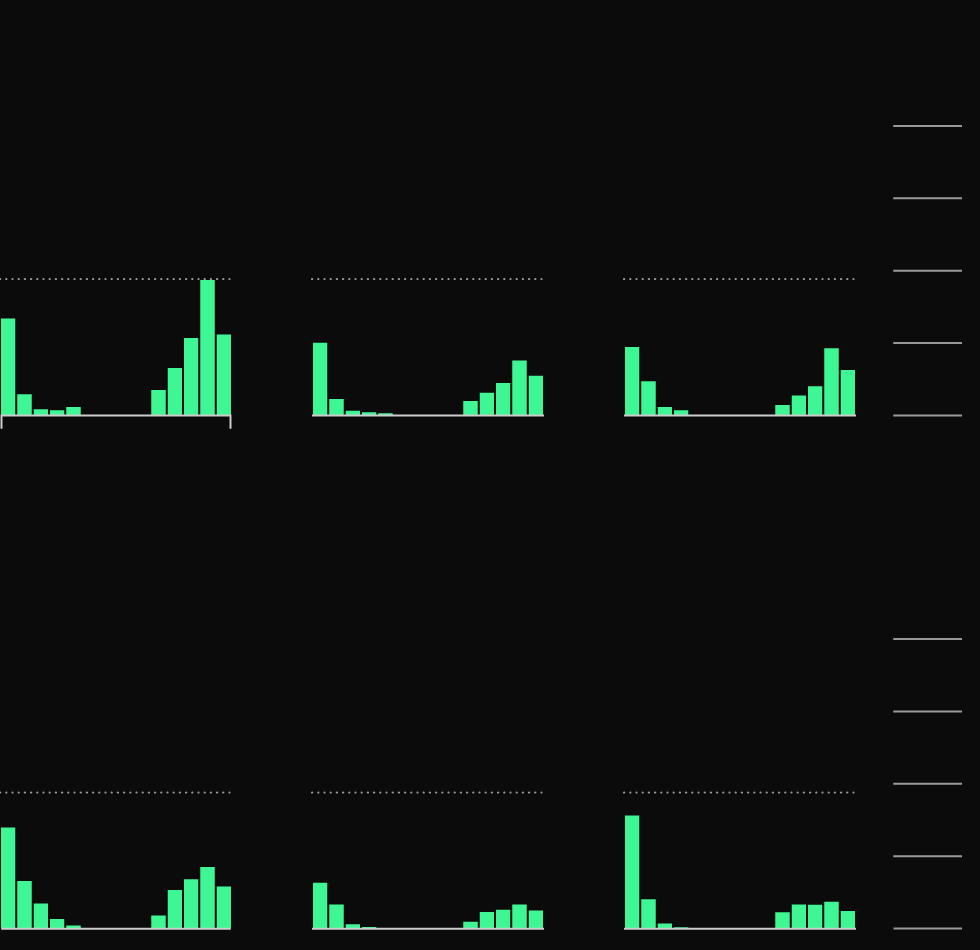

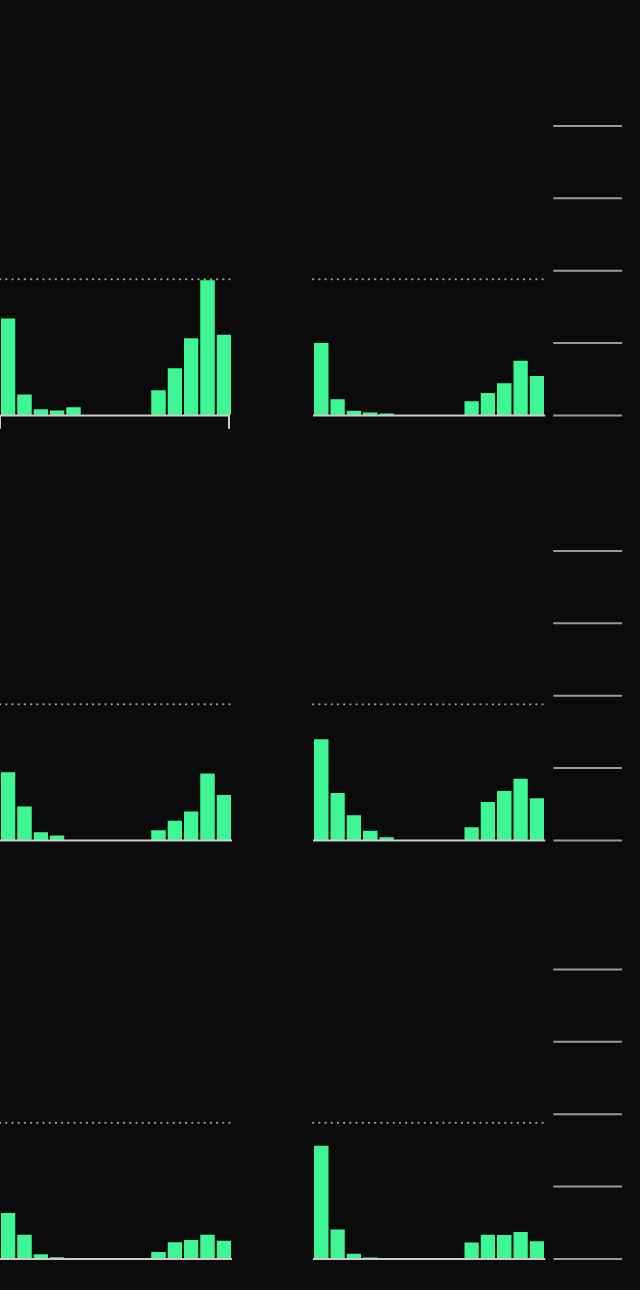

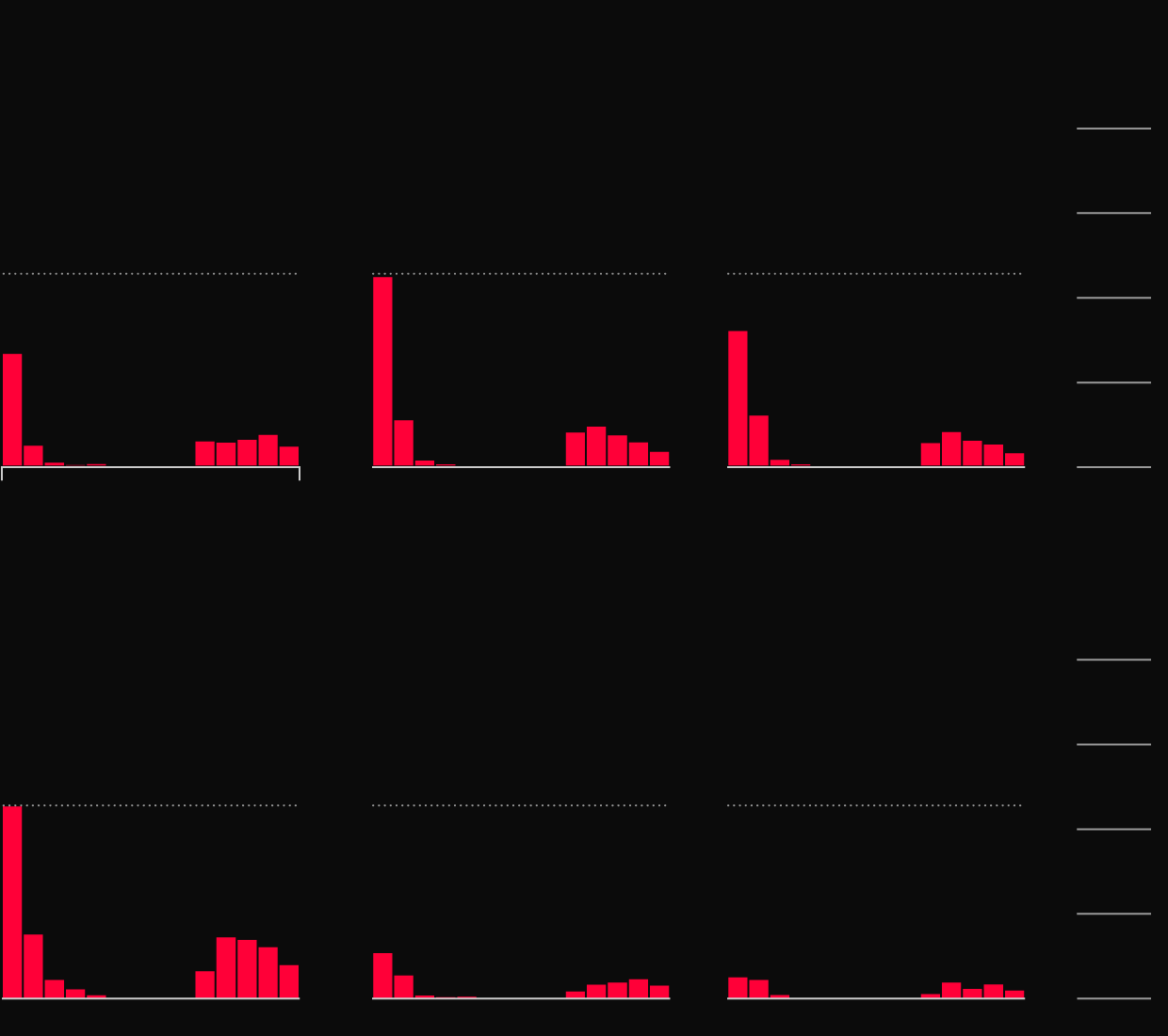

How PPP Reached Minority Areas Differently

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington, DC

$200M

▲

Peak total loan amount

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington,

DC

$200M

▲

Peak total loan amount

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

$200M

150

100

50

0

5/21

4/20

Month loan funded

Los Angeles

Miami

$200M

150

100

50

0

New York

Washington,

DC

$200M

▲

Peak total loan amount

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

Peak total loan amount

▼

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington, DC

$200M

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

Peak total loan amount

▼

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington,

DC

$200M

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

$200M

150

Peak total loan amount

▼

100

50

0

5/21

4/20

Month loan funded

Miami

Los Angeles

$200M

150

100

50

0

Washington,

DC

New York

$200M

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington, DC

$200M

Peak total loan amount

▼

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

Los Angeles

$200M

150

100

50

0

5/21

4/20

Month loan funded

Miami

New York

Washington,

DC

$200M

Peak total loan amount

▼

150

100

50

0

Actual loan amount per 100k people

Chicago

Houston

$200M

150

100

50

0

5/21

4/20

Month loan funded

Los Angeles

Miami

$200M

Peak total loan amount

▼

150

100

50

0

New York

Washington,

DC

$200M

150

100

50

0

In Houston, the recovery is uneven among Black businesses—restaurants are doing well but commercial real estate isn’t. Overall they aren’t bouncing back as fast as some other ethnic groups, said Carol Guess, interim president of Greater Houston Black Chamber of Commerce.

“It’s because of the same reasons that have always plagued Black businesses—operating under the slimmest of margins and also lack of access to capital,” she said.

The same goes for Latino entrepreneurs, according to Laura Murillo, president of the city’s Hispanic Chamber of Commerce: “Many of them did not have bank relationships.”

One city stands out for its robust economy across racial lines: Atlanta. The city’s longtime status as a hub for Black Americans probably helped, with a deep bench of business groups that worked at funneling aid.

“You’ve got some pretty substantial organizations that were all connected and working together to get the word out and encourage people,” said Grace Fricks, who runs a nonprofit called ACE that makes loans to underserved businesses in North Georgia.

In Chicago, by contrast, dozens of small Black-owned businesses haven’t restarted operations and don’t plan to reopen, according to clients of the Chicago Urban League, a century-old Black advocacy group.

The delay in access to capital is contributing to closures because the owners didn’t get the intended “breathing room,” said Karen Freeman-Wilson, chief executive officer of the league.

“Some were not able to recover,” she said.

Before the pandemic, Chicago Mayor Lori Lightfoot had earmarked minority neighborhoods in her signature Invest South/West economic redevelopment plan to infuse capital into under-invested areas and projects have been announced gradually over the last year and a half.

Chicago also helped funnel more than $100 million in grants and loans to small businesses to help cover the holes left by PPP.

“This is decades in the making and that’s true across many other cities. So we have to close that gap,” Samir Mayekar, deputy mayor for economic and neighborhood development, said in an interview. “We are focused on wealth building in our Black and Brown communities especially.”

Chicago’s South Shore neighborhood, one of 10 areas of focus in Lightfoot’s program, offers a glimpse of the complex challenges—complicated even more by Covid-19.

Soul vegan eatery Majani, in the South Shore neighborhood.

Soul vegan eatery Majani, in the South Shore neighborhood.

Soul vegan eatery Majani, in the South Shore neighborhood.

Soul vegan eatery Majani, in the South Shore neighborhood.

Soul vegan eatery Majani, in the South Shore neighborhood.

Tsadakeeyah Emmanuel opened a vegan soul food restaurant Majani with his wife in 2017.

He’s since added two locations elsewhere in the city, but a few weeks ago, the 58-year-old restaurateur decided to close the restaurant closest to downtown office high rises, due to a lack of volume and labor.

His biggest worry for the remaining restaurants? Crime.

Emmanuel, who got two PPP loans worth a total of $122,000, is keeping the South Shore and Pullman places on the South Side open based on a determination to serve healthy food to his home community even in the face of shooting incidents nearby and one break-in in July.

“We are not immune,” he said. “We are just undeterred.”

Across the street from Majani, Chef Sara’s Cafe kept filling orders through the pandemic, even when business was down to a quarter of the normal level.

Sara Phillips, 72, got about $4,500 from two rounds of PPP. She didn’t want more because she didn’t want to accumulate debt.

She says she feels blessed that customers are coming back slowly. Around the neighborhood, some restaurants and a clothing store shuttered.

Stephane Bamigbade, 39, hasn’t reopened yet. She shuttered her five-year-old Little Bugs Learning Center in the Humboldt Park neighborhood in July 2020 when the lease expired. Her landlord indicated that many capital expenses related to spacing, ventilation and other mitigations for Covid-19 would largely fall on her. She just couldn’t afford those costs.

Stephane Bamigbade at her daycare center’s future location in Schiller Park, near O’Hare airport.

Stephane Bamigbade at her daycare center’s future location in Schiller Park, near O’Hare airport.

Stephane Bamigbade at her daycare center’s future location in Schiller Park, near O’Hare airport.

Stephane Bamigbade at her daycare center’s future location in Schiller Park, near O’Hare airport.

Stephane Bamigbade at her daycare center’s future location in Schiller Park, near O’Hare airport.

She eventually got PPP funds but if the money had arrived sooner, she said she may have considered staying in the same area. Instead, Bamigbade is working on reopening a daycare center in Schiller Park, a suburb near O’Hare International Airport.

“It’s been stressful,” she said. “Not working for a whole year and half.”

Beauty salons were the single most common PPP recipient in Chicago, receiving an average of just $21,240 per loan, data show, about one-third the overall average.

Monica Abernathy, the 41-year-old owner of A Polished Work Nail Spa Lounge, was one of them. But it took a while to get help: She was denied a PPP loan at first because her technicians are contractors, and got $6,000 in a subsequent round.

Like many other sole proprietors, Sherry Spellers, 52, failed to secure PPP aid for her Amour Salon & Suites in Bronzeville. She relied on other loans and grants to stay afloat. She said she needs the flexibility of self-employment to care for her son, whose safety she constantly worries about amid street violence. There is “no plan B,” she said.

Sherry Spellers, owner of Amour Salon & Suites,

in Bronzeville.

Sherry Spellers, owner of Amour Salon & Suites,

in Bronzeville.

Sherry Spellers, owner of Amour Salon & Suites,

in Bronzeville.

Sherry Spellers,

owner of Amour Salon & Suites, in Bronzeville.

Sherry Spellers,

owner of Amour Salon & Suites, in Bronzeville.

When PPP loans arrived on time and in adequate amounts, they helped instill confidence and kept employees on the job.

“We stayed open the whole time,” said Nicolás Guerrero, 40, who with his father owns the 10-year-old Guerrero’s Tacos & Pizza in the Humboldt Park neighborhood.

The business has retained its six employees, three of whom are family members, using part of a $33,000 PPP loan to pay salaries that it got in 2020.

The funds also helped ease costs for the business at a time when meat prices were spiking and gave hope that “we’re going to make it,” Guerrero said.

For businesses in minority communities of Chicago, the struggle to reopen—and stay open—is an ongoing challenge for the labor market recovery, and for policy makers who vow that this time they won’t leave anyone behind.