China's $12 Trillion Onshore Credit Market Brushes Off Defaults

China Credit Tracker

China’s $12.3 trillion local credit market is proving more resilient than its offshore counterpart to a historic crackdown on the property sector and a record wave of defaults.

Stress in the domestic market eased to the lowest level on Bloomberg’s China Credit Tracker in May, further diverging from the elevated scores seen offshore. Average spreads on riskier AA-rated local bonds over respective government notes that month narrowed to their tightest level since at least 2011.

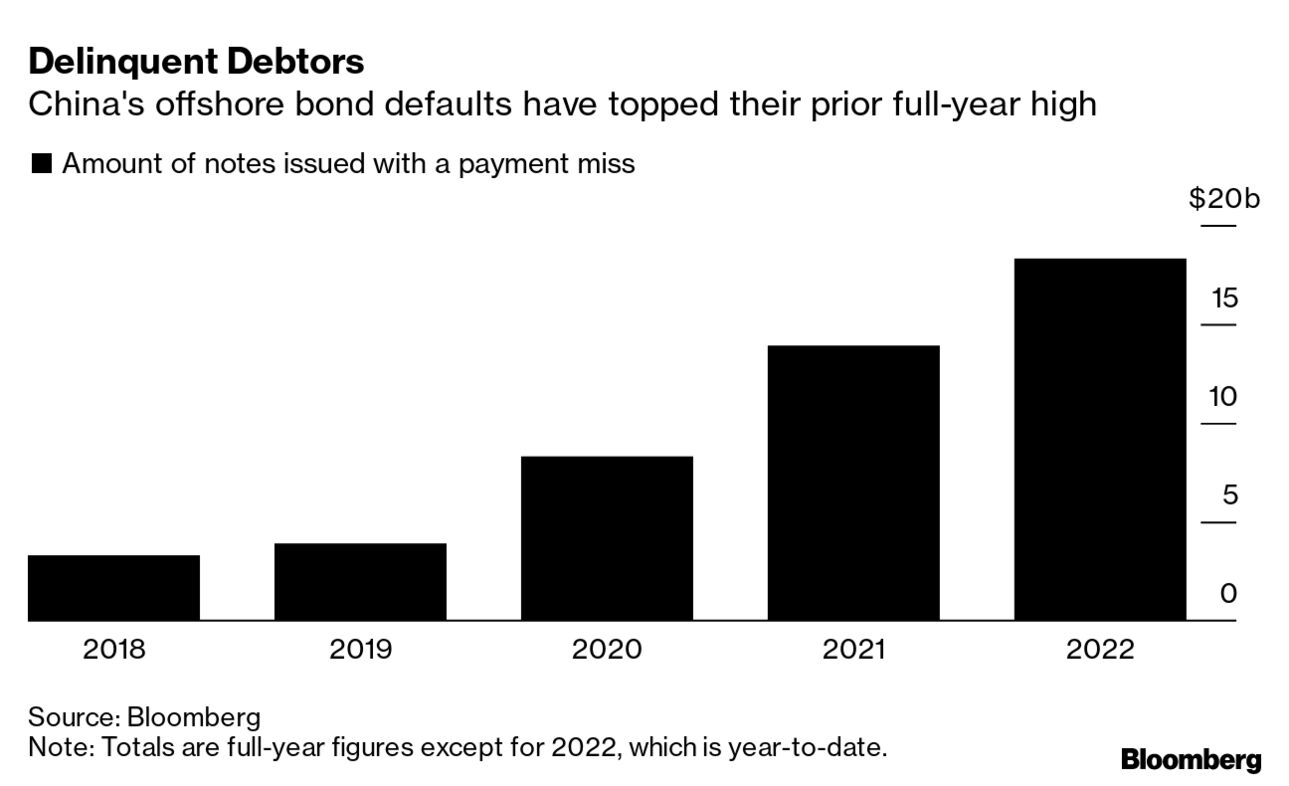

That’s in stark contrast to the much smaller offshore bond market where beleaguered developers have driven a historic $18 billion of defaults, five times more than among local debt.

Preserving calm in China’s domestic market is a priority for authorities as they roll out an ambitious campaign to reduce financial risk and curb moral hazard. Policymakers need to strike a careful balance: allowing more payment failures is necessary to debunk assumptions that the state will save borrowers, but too much stress could trigger contagion and systemic risk to the broader market. The economic costs of the nation’s strict Covid-zero policy will add to the challenge.

China is counting on a stable government-bond market to raise much-needed public funding, even as foreign investors -- who own more than 10% of China’s sovereign debt market -- are selling the notes in the longest streak of outflows since 2015. Citic Securities Co. predicts local authorities will sell at least 1.5 trillion yuan ($225 billion) this month alone to help pay for extra fiscal stimulus needed to support the economy. Chinese banks are the main buyers of government debt.

Delinquent Debtors

China's offshore bond defaults have topped their prior full-year high

So far, stress in the debt-saddled property sector has been largely contained to the offshore market, even after high-profile defaults at giants like China Evergrande Group and Kaisa Group Holdings Ltd. That’s partly because global investors have absorbed the bulk of losses as borrowers prioritize making payments or seeking extensions on their local bonds, even when failing to repay their dollar debt.

Onshore Resilience

China's local bonds had mostly positive returns despite property angst

That’s kept returns in the local corporate bond market positive for 21 of the past 24 months, even as China junk bonds saw their ninth-consecutive month of losses in May.

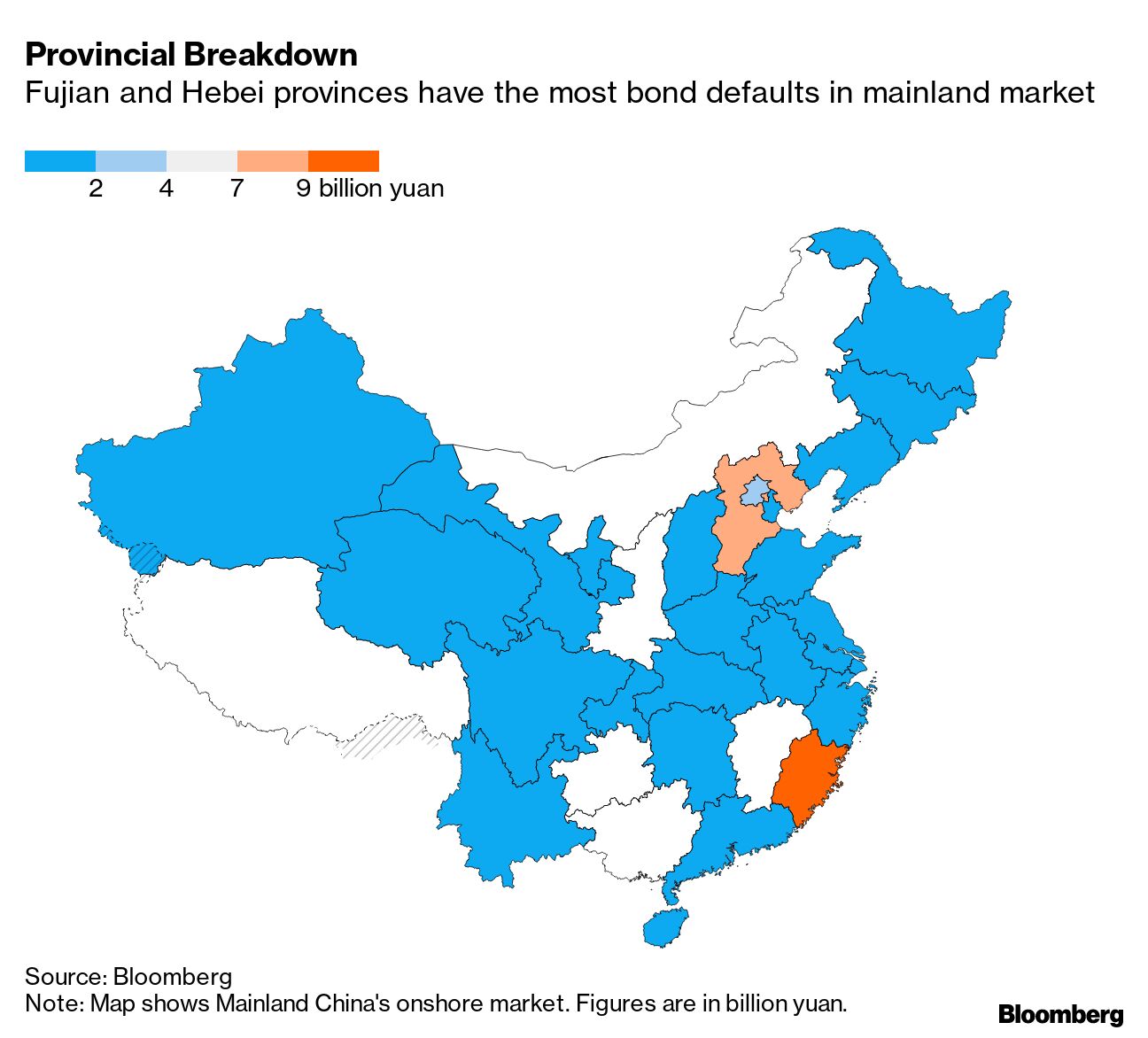

Provincial Breakdown

Fujian and Hebei provinces have the most bond defaults in mainland market

After more than a year of prolonged difficulties for developers, policymakers have stepped up efforts to ease the credit crunch by cutting key interest rates and reviving tools that mitigate credit risk. The sale of new credit-guaranteed local bonds by a small cohort of builders is one such method.

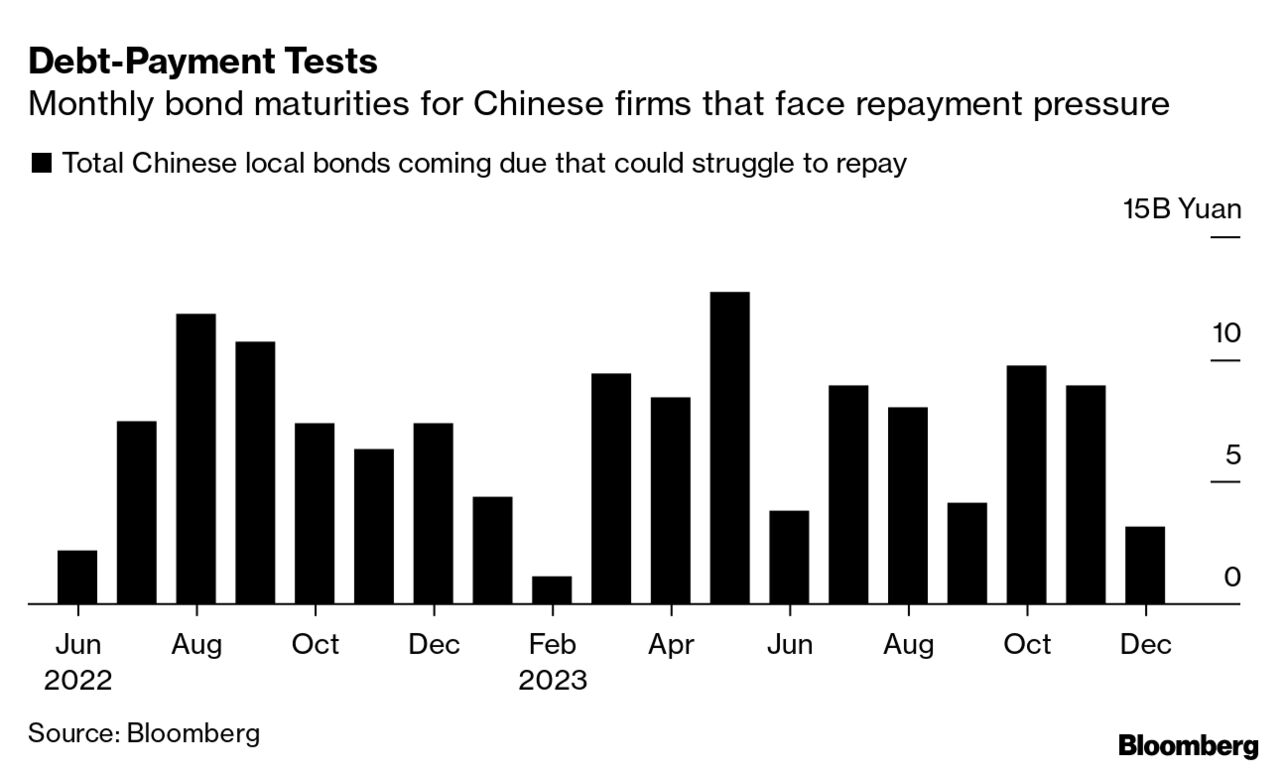

Debt-Payment Tests

Monthly bond maturities for Chinese firms that face repayment pressure

While the guarantees to insure against default are “symbolic” in that they only cover part of the principal, “we believe the government also arranged for securities firms to provide protection,” according to S&P Global Ratings analysts including Wilson Ling. It’s another sign that Beijing is focused on boosting confidence.

Such measures have so far underwhelmed investors, but the resilience of China’s local bond market over the past two years could attract more global buyers. A recent move to make it easier for foreigners to access corporate bonds via the exchange market may signal a desire to encourage more overseas capital, though this currently makes up a very small portion of the buyers.