China’s Credit Market Reaches Inflection Point as Stress Builds

China Credit Tracker

Losses are among the worst ever. Borrowing costs are at a record high and big investors are cutting positions.

China’s offshore high-yield credit market is at a critical juncture: It's falling back again in recent days, after key metrics showed stress reaching record levels earlier in March. Market concerns prompted vows for policy action in the middle of last month that helped spark a rally, but that rebound has been fading in recent days amid scant signs of policy details and as Covid lockdowns weigh on sentiment.

Distress in the nation’s $870 billion offshore debt market remained at the highest level, Bloomberg’s China Credit Tracker shows. Losses deepened to a fresh low, while average yields on junk-rated debt, dominated by builders, rose to a fresh high of 24.9%. Rising defaults in the much-larger onshore market also spurred higher stress levels, according to the tracker.

Already contending with a clampdown that triggered record defaults and dwindling home sales, developers need to shore up investor confidence in the embattled sector to sustain their recent rebound. Uncertainty persists about the scale of many property firms’ debt, with a number of them yet to release audited results for last year.

Still Accelerating

China junk dollar notes' losses continue to build on default worries

China’s high-yield offshore market—once one of the world’s most-profitable bond trades—has shrunk as many developers struggle to issue fresh debt. Junk and non-rated builders, which dominate the speculative-grade market, sold about $1.5 billion of dollar notes so far this year, down 91% from the same period in 2021, Bloomberg-compiled data show.

More than half of high-yield developer dollar bonds were trading below 30 cents on the dollar at the end of March, according to Bloomberg Intelligence.

BlackRock Inc. is among the biggest investors in China’s junk property bonds. The firm reduced its exposure in March for the first time in months, after previously doubling down through a period of rising distress. Institutional investors that publicly file their holdings trimmed exposure last month after adding $3.7 billion of dollar bonds in par value terms between early November and the end of February, according to data compiled by Bloomberg.

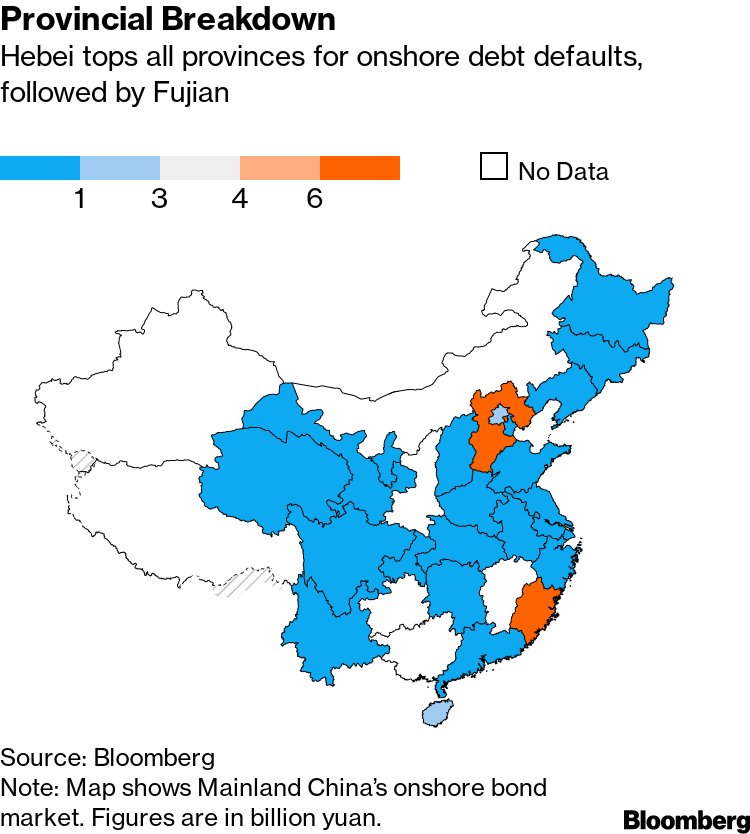

Provincial Breakdown

Hebei tops all provinces for onshore debt defaults, followed by Fujian

China’s property industry has been rocked by at least 17 offshore defaults by developers since authorities began cracking down on excessive borrowing and speculation in the housing market in 2020. Shanghai-based Zhenro Properties Group Ltd., which was considered a rare beacon of strength earlier this year until it warned of a possible failure in February, has become the latest to default.

In the domestic bond market, China Fortune Land Development Co.’s approved debt restructuring plan has pushed Hebei's defaults to the highest among provinces. That's followed by Fujian, where Yango Group Co. has missed bond payments on a combined 7 billion yuan of principal and interest so far this year. Several developers with roots in that that province, known for their aggressive debt-fueled land acquisitions, have also been caught up in the property crisis.

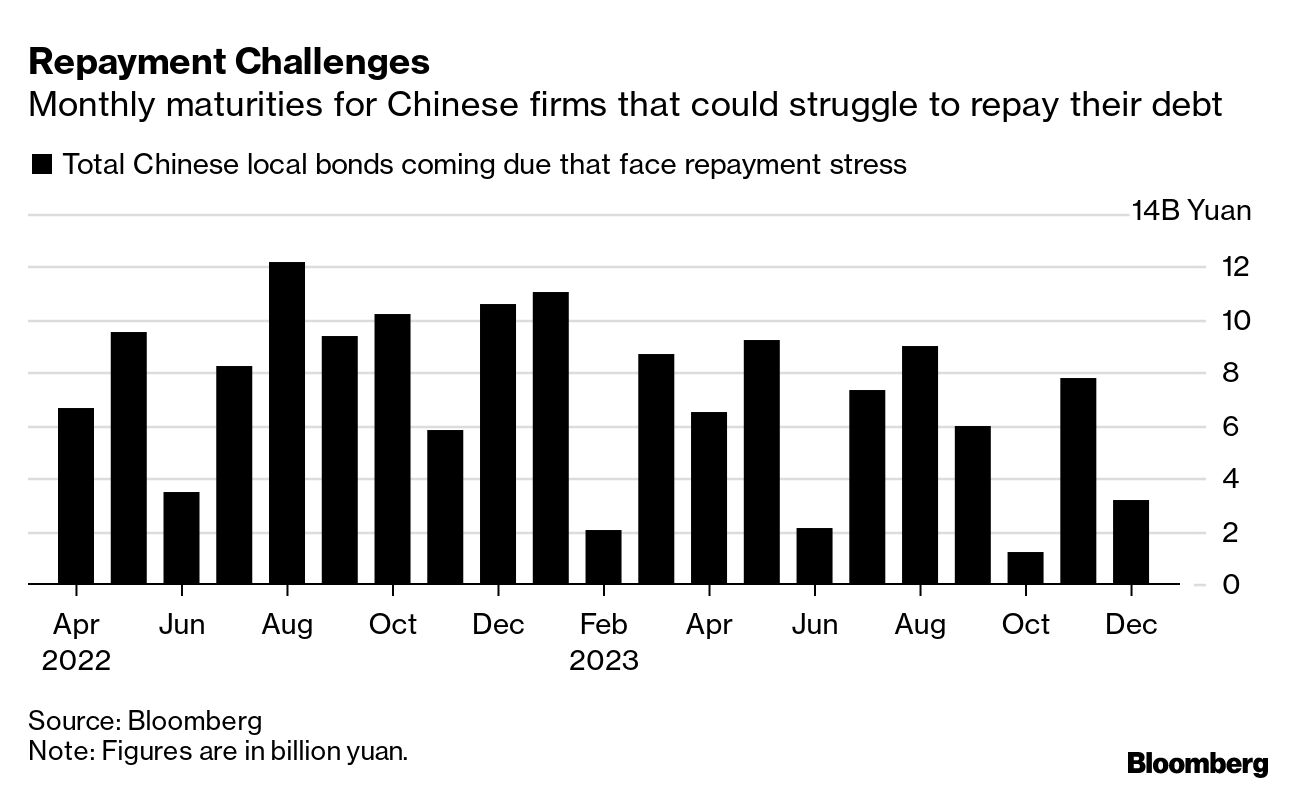

Repayment Challenges

Monthly maturities for Chinese firms that could struggle to repay their debt

After months of being trapped out of the offshore bond market, there are some tentative signs that property developers may find a way to access funding. CIFI Holdings Group Co., which unlike some of its peers has released audited 2021 results, recently sold a convertible bond and is proposing to issue additional notes.

Better-quality firms may also follow in the footsteps of Greentown China Holdings Ltd., which in January sold a so-called credit-enhanced bond with a standby letter of credit. Still, demand for these types of notes from developers remain relatively untested during the sector’s credit crunch and a guarantee by a bank means the debt typically offers lower yields.