China Credit Investors Brace for More Surprises From Hidden Debt

China Credit Tracker

China’s credit markets are ushering in the new year with a fresh bout of stress, as scrutiny of hidden debt among the nation’s developers adds to turmoil in a sector facing mounting bills and limited fundraising options.

Transparency concerns are resurfacing ahead of earnings season, as investors try to avoid nasty surprises. After months of plunging sales, developers are preparing to open their books for the first time since a government clampdown on debt in the sector triggered a liquidity crisis.

Distress in the nation’s $870 billion offshore debt market remained elevated during a volatile January, Bloomberg’s China Credit Tracker shows. Returns on dollar bonds tumbled to the lowest in nearly two years, while the relatively stable onshore market saw bond defaults hit a five-month high.

The slump stems in part from worries that unreported debt may create unforeseen liquidity pressure, with liabilities like trust loans, private bonds and high-yield consumer products receiving preferential treatment over public bonds.

Concerns about unreported debt at Logan Group Co., China’s 20th-largest developer by sales last year, helped drag down the broader sector in recent days as bondholders question the liquidity of firms whose finances were long considered more sound than the likes of China Evergrande Group. Logan has denied having private debt guarantees.

Fears of an auditor exodus have added to the turbulence after resignations at at least three developers last month. There are mounting worries that earnings could reveal fresh risks or may even be delayed if auditors don’t receive enough information to sign off on results.

Dive into the methodology behind Bloomberg’s China Credit Tracker

Bondholders are learning to price in these risks: bad-debt manager China Huarong Asset Management Co. last year triggered an unprecedented crisis of confidence in the firm’s financial health after it failed to meet its results deadline. It got a state-led rescue after reporting a record loss of $15.9 billion in 2020.

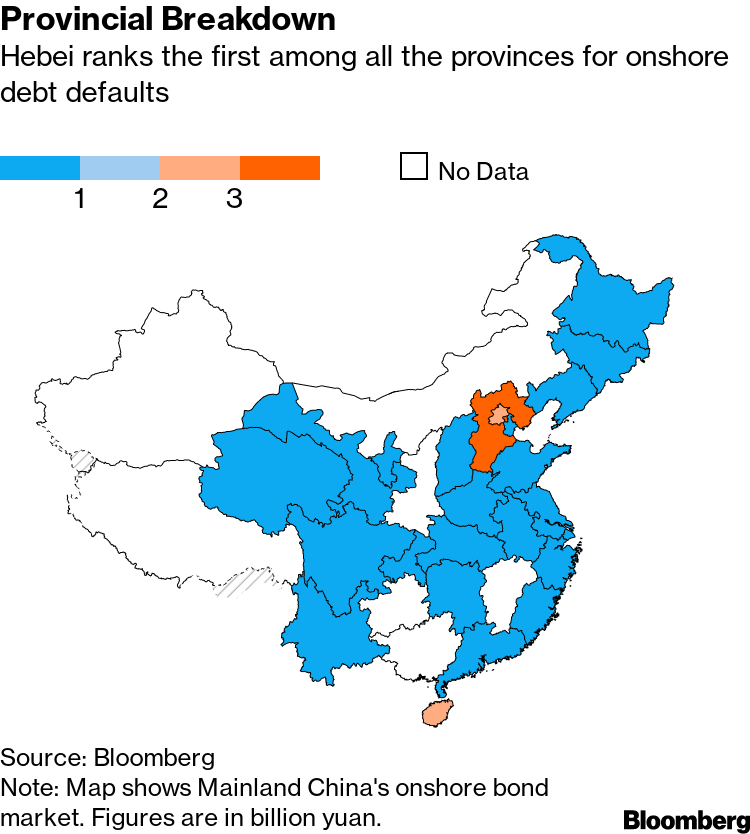

Provincial Breakdown

Hebei ranks the first among all the provinces for onshore debt defaults

Real estate firms face lower maturities in February which may offer a brief reprieve. Still, after months of being trapped out of the offshore primary market, borrowers like Yuzhou Group Holdings Co. are still trying to delay repayments. What’s more, signs of policy easing are yet to offer much relief to the bulk of China’s private, stressed developers.

Maturity Wall

Monthly maturities for Chinese firms that could struggle to repay their debt

The slump in property sales persisted for a sixth month in January, with top developers seeing a steeper decline in transactions. With more state firms stepping in to buy land—local government financing vehicles represented half of the top 20 buyers of land by yuan amount last month—private builders also face weakened project pipelines this year.