The Missing Piece of the Hydrogen Puzzle

A three-part series on hydrogen energy

Photo: Clemens Bilan/AFP via Getty Images

The universe’s most abundant element is having a good year. Clean hydrogen is enjoying unprecedented support among global political leaders, who see it as a means of decarbonizing hard-to-tackle corners of the economy, while powering up jobs and post-pandemic investment. From Portugal to Chile, ambitious strategies are racking up. That’s good news, because no promising technology needs as much help as this one.

Even if it will account for only a quarter of overall power demand by mid-century at the upper end of forecasts, hydrogen is the missing link in the transition away from fossil fuels. This versatile energy carrier can be used to decarbonize everything from steelmaking to aviation. Yet to deliver on the hype and help the world meet zero-emissions targets, the cost of green hydrogen — as opposed to the kind made with fossil fuels — needs to come down, and faster than it did for wind and solar. That means scaling up the technologies and infrastructure involved.

Green hydrogen, produced by using renewable energy to split water, can cost several times the standard hydrocarbon version. Even carbon capture and storage — which turns hydrogen made with natural gas into cleaner, so-called blue hydrogen by trapping noxious emissions — is only nascent. The same is true of transport networks, storage, regulation and even demand beyond traditional industrial applications, like oil refining or fertilizer production. Without policy support, there’s a risk countries will miss out on this global energy realignment. Worst of all is the threat that hydrogen won’t get past the tipping point fast enough to mitigate a rapidly warming climate.

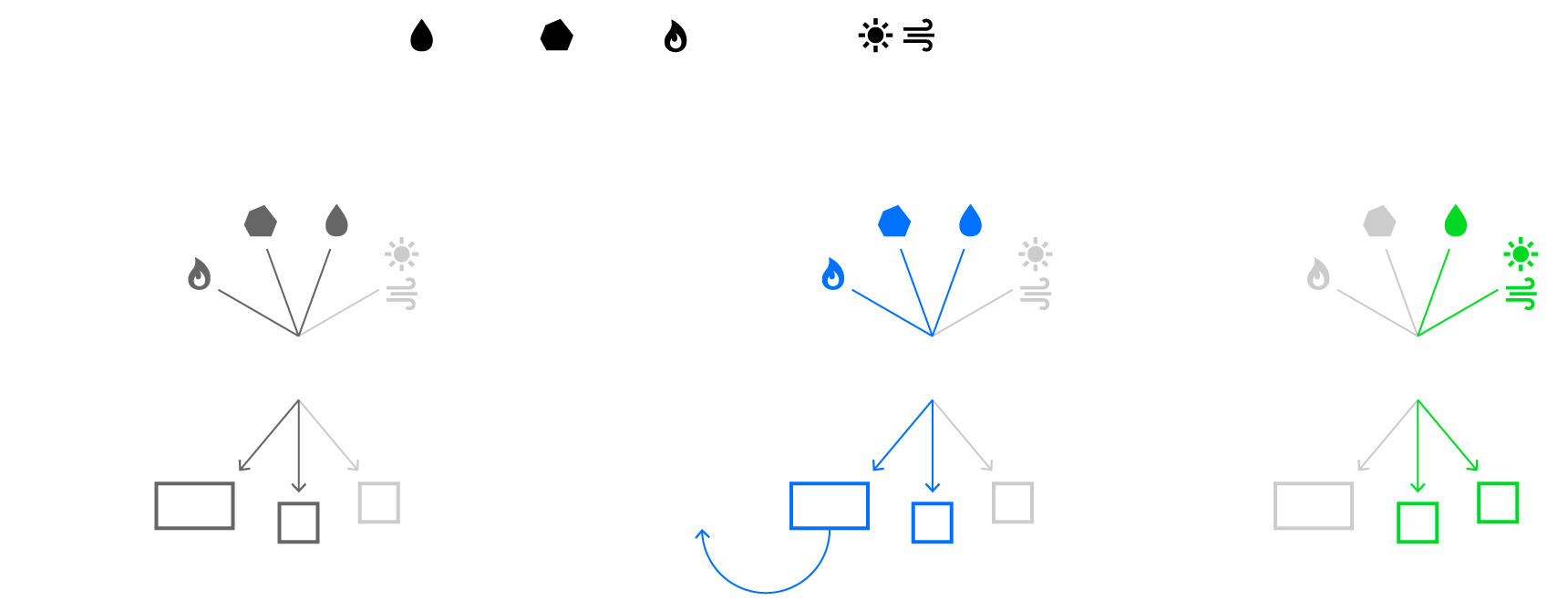

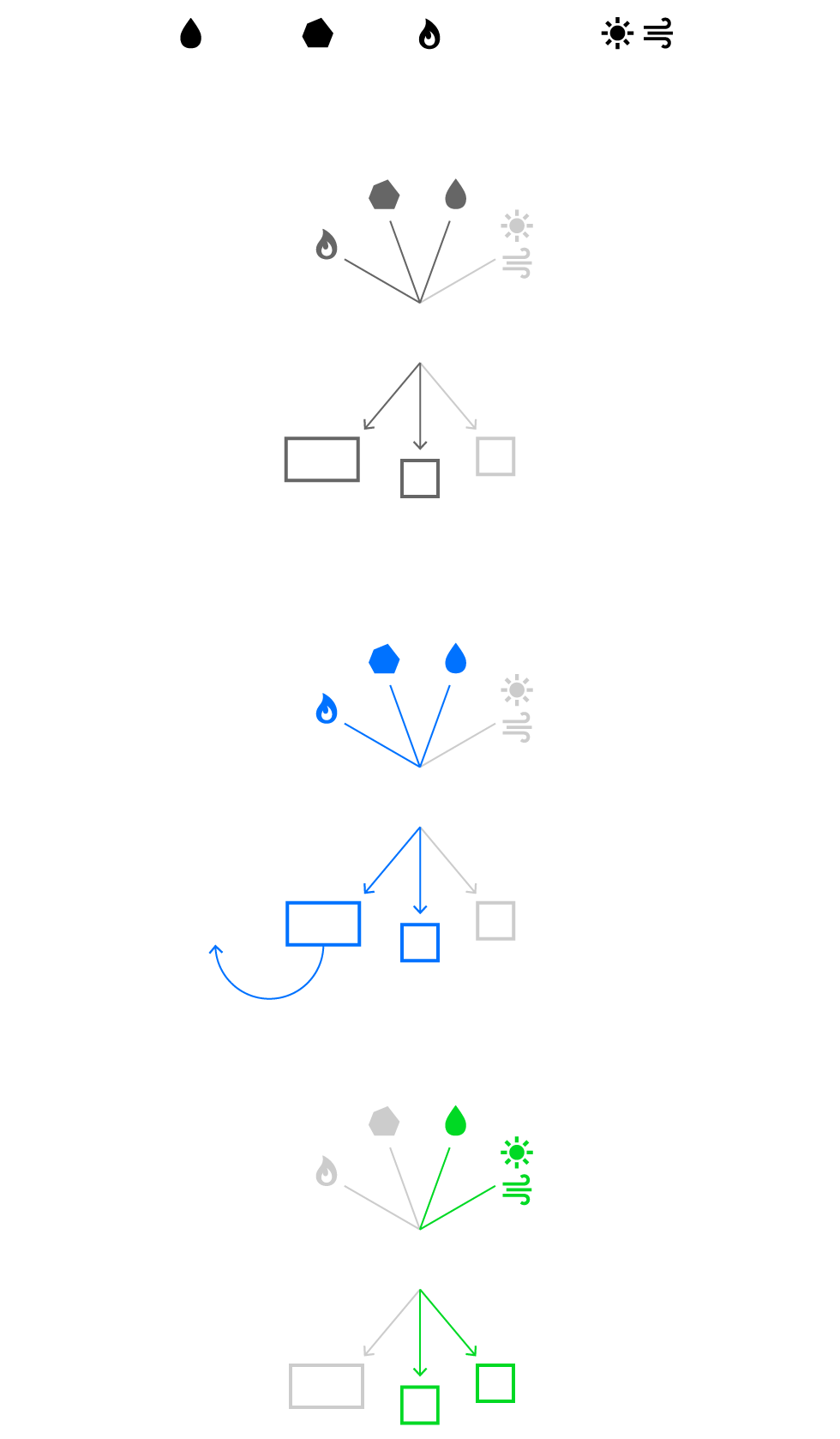

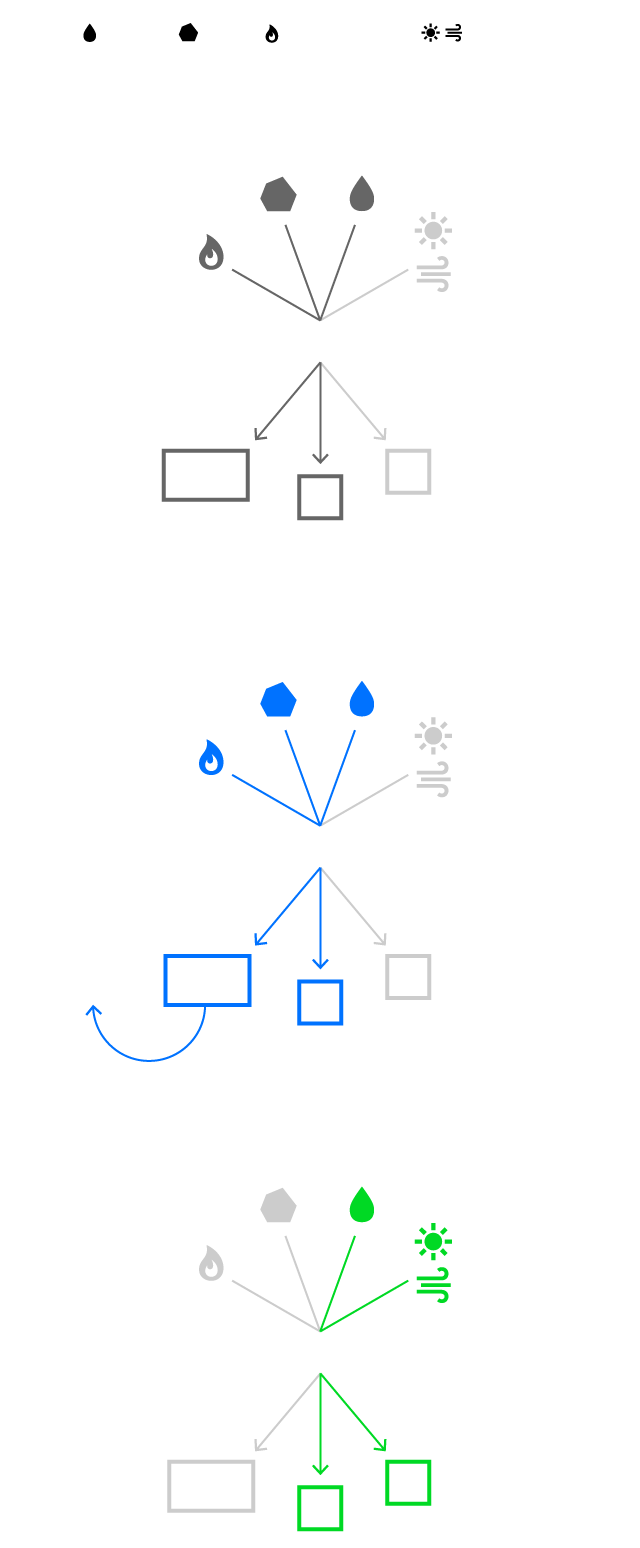

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon dioxide as a byproduct

Blue hydrogen captures and stores

most of the carbon dioxide output

Green hydrogen’s

byproduct is oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

CO

O

CO

O

CO

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon dioxide as a byproduct

Blue hydrogen captures and stores

most of the carbon dioxide output

Green hydrogen’s

byproduct is oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

CO

O

CO

O

CO

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil

fuels and produces carbon

dioxide as a byproduct

Blue hydrogen captures

and stores most of the

carbon dioxide output

Green hydrogen’s

byproduct is

oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

O

CO

CO

CO

O

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon as a byproduct

or

Gasifier/reformer

CO

O

2

H

Blue hydrogen captures and stores

most of the carbon output

or

Gasifier/reformer

Carbon

capture,

storage

CO

O

2

H

Green hydrogen’s byproduct is oxygen

Electrolyzer

CO

O

2

H

Coal

Solar/wind

Inputs:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon as a byproduct

or

Gasifier/reformer

O

CO

2

H

Blue hydrogen captures and stores

most of the carbon output

or

Gasifier/reformer

Carbon

capture,

storage

O

CO

2

H

Green hydrogen’s byproduct is oxygen

Electrolyzer

O

CO

2

H

In that sense, 2020 has been encouraging, with plenty falling into place. Net-zero goals are suddenly everywhere. The cost of water-splitting electrolyzers has fallen — by 40% between 2014 and 2019 for those made in North America and Europe, according to BloombergNEF, and still further in China. Momentum is picking up, too. In the ten months through August, consultancy Wood Mackenzie says the announced project pipeline for green hydrogen expanded from 3.5 gigawatts to 15 gigawatts — and some forecasts are even higher, though industry figures range widely. Governments are also redefining energy plans and the global supply map. Eurasia Group estimates countries representing about half of the world’s gross domestic product now have credible hydrogen strategies. That number rises to 70% once the U.S., Canada and Russia finalize their plans. But who is doing it right? And can national-level policies even work?

There’s no simple answer. Economic development, resource endowment and geography play a role in any outcome, and not all disadvantages can be conquered. Large-scale, local supply chains, as seen in Europe, will work best at first. For much of the world, blue hydrogen will need to be deployed alongside green to achieve the required scale. But it’s all easier with a coherent blueprint that does at least four things: leverages existing advantages; encourages green hydrogen production with flagship projects, including funding to bridge the transition; supports the development of transport and storage resources; and boosts demand. For nations that are also significant consumers, like Japan, there’s the need to consider diverse sources of supply, too.

The European Union’s roadmap, published in July, does much of this — even if it leans heavily on member states to support the 470 billion euros ($558 billion) of investment it sees for renewable hydrogen alone by 2050. Indeed, there’s a lot to like, including an ambitious target of 40 gigawatts in electrolyzer capacity by 2030. BNEF estimates that would cut the cost of producing hydrogen from renewables in the bloc by 60% to just $1.50 per kilogram — below forecasts for the blue version. And while 40 gigawatts may not sound like much, as Martin Lambert at the Oxford Institute for Energy Studies notes, the largest electrolyzer under construction in Europe has a capacity of just 10 megawatts. The Brussels plan also mentions so-called carbon contracts for difference, an important means of covering the cost gap for investors between old and new technology, while the carbon price remains too low.

The plan builds on current advantages, such as relying on Europe’s industrial clusters — obvious sources of demand and the focus of early production — and existing natural gas infrastructure, rather than depending on road transport, which is expensive for a low density gas that takes up too much space. We’re seeing the beginnings of the structure and regulation for a hydrogen market, too.

Finally, Europe is tying in geopolitically strategic partners, envisaging 40 gigawatts of electrolyzer capacity from neighbors — probably Morocco to the south and Ukraine to the east. A good hydrogen strategy, as for early adopters like Japan, is about energy security too, supporting a strategic reserve of power from multiple sources.

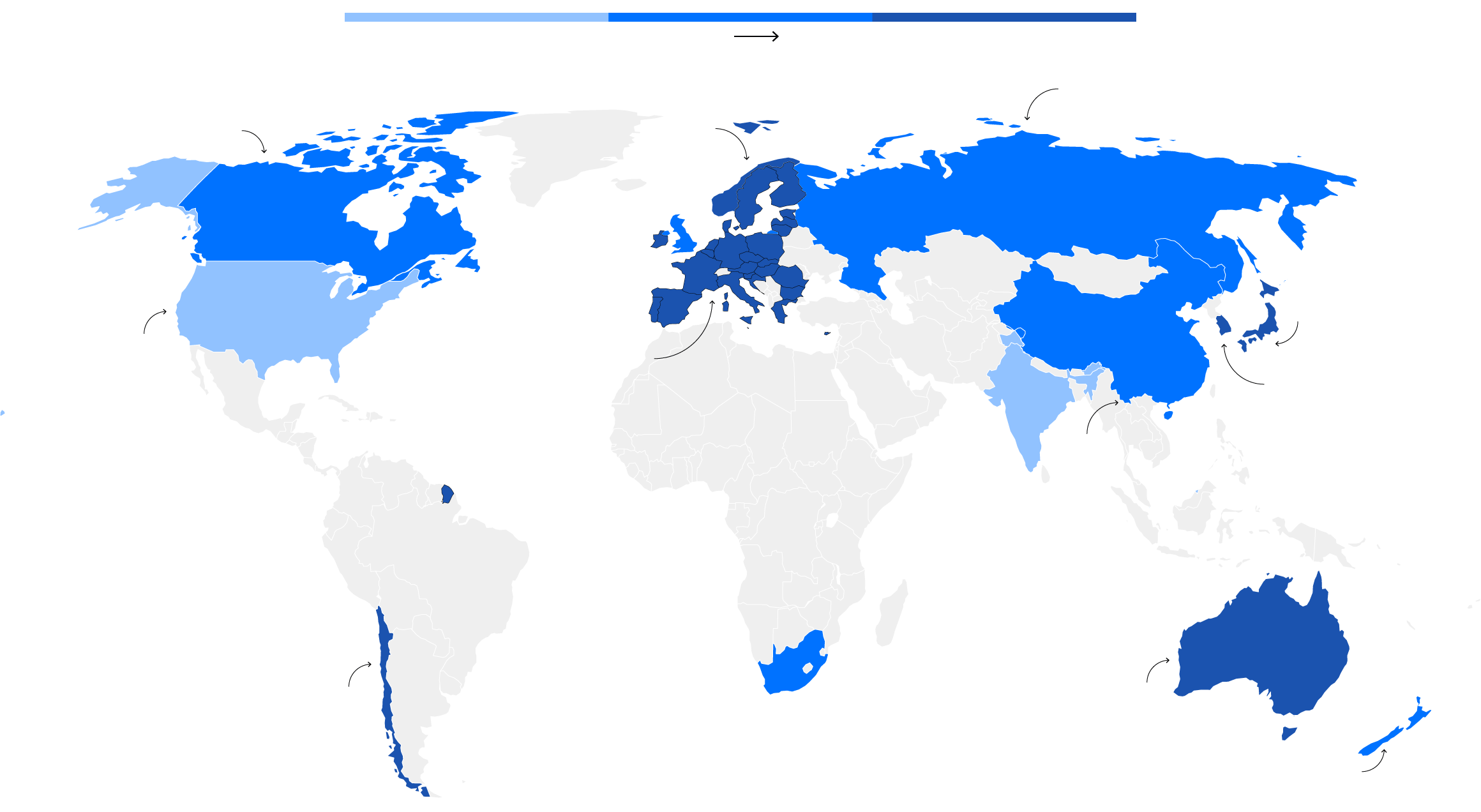

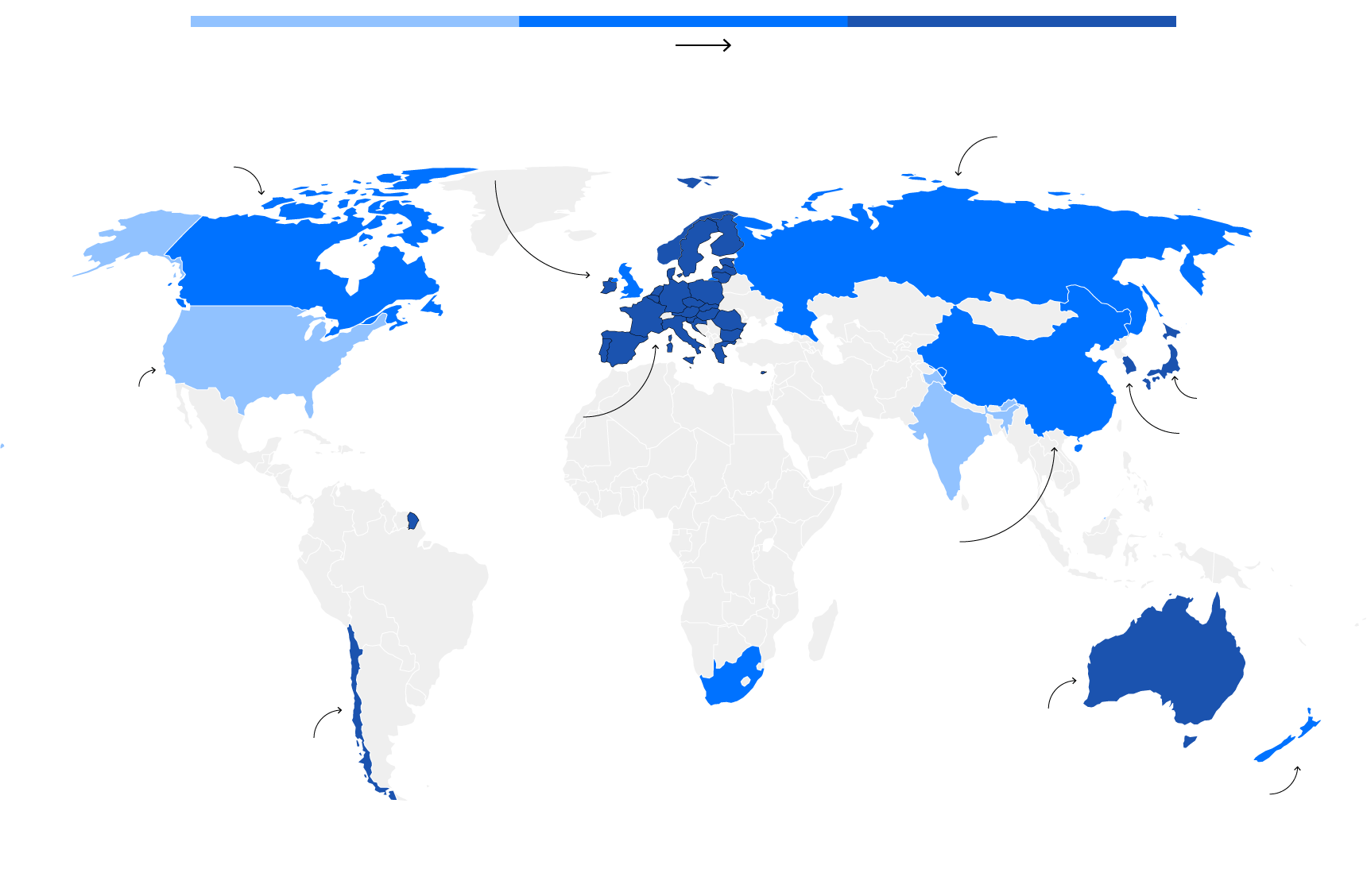

Green Goals

National hydrogen strategy, more robust plans

Hydrogen could be used to meet 27% of Canada’s primary energy needs

The Nord Stream 2 gas pipeline could deliver hydrogen from Russia to Europe

EU aims to install 40GW of renewable hydrogen electrolyzers by 2030

Japan was the first to adopt a comprehensive hydrogen strategy

Most hydrogen production in the U.S. uses natural gas

Germany’s $10B strategy outspends the rest

South Korea wants to lead in the production and use of hydrogen vehicles

China is already the world’s largest producer, but mostly from coal

Australia aims to be among the top three exporters of hydrogen to Asian markets by 2030

Chile aims to produce the world’s cheapest green hydrogen by 2030

New Zealand published a vision for hydrogen in 2019

National hydrogen strategy, more robust plans

The Nord Stream 2 gas pipeline could deliver hydrogen from Russia to Europe

EU aims to install 40GW of renewable hydrogen electrolyzers by 2030

Hydrogen could be used to meet 27% of Canada’s primary energy needs

Japan was first to adopt a comprehensive strategy

Most hydrogen production in the U.S. uses natural gas

Germany’s $10B strategy outspends the rest

South Korea wants to lead in the production and use of hydrogen vehicles

China is already the world’s largest producer, but mostly from coal

Australia aims to be among the top three exporters of hydrogen to Asian markets by 2030

Chile aims to produce the world’s cheapest green hydrogen by 2030

New Zealand published a vision for hydrogen in 2019

National hydrogen strategy, more robust plans

Hydrogen could be used to meet 27% of Canada’s primary energy needs

The Nord Stream 2 gas pipeline could deliver hydrogen from Russia to Europe

EU aims to install 40GW of renewable hydrogen electrolyzers by 2030

Germany’s $10B strategy outspends the rest

Japan was first to adopt a comprehensive strategy

Most hydrogen production in the U.S. uses natural gas

China is the world’s largest producer, mostly from coal

Chile aims to produce the world’s cheapest green hydrogen by 2030

Australia aims to be among the top three exporters of hydrogen to Asian markets by 2030

New Zealand published a vision for hydrogen in 2019

National hydrogen strategy, more robust plans

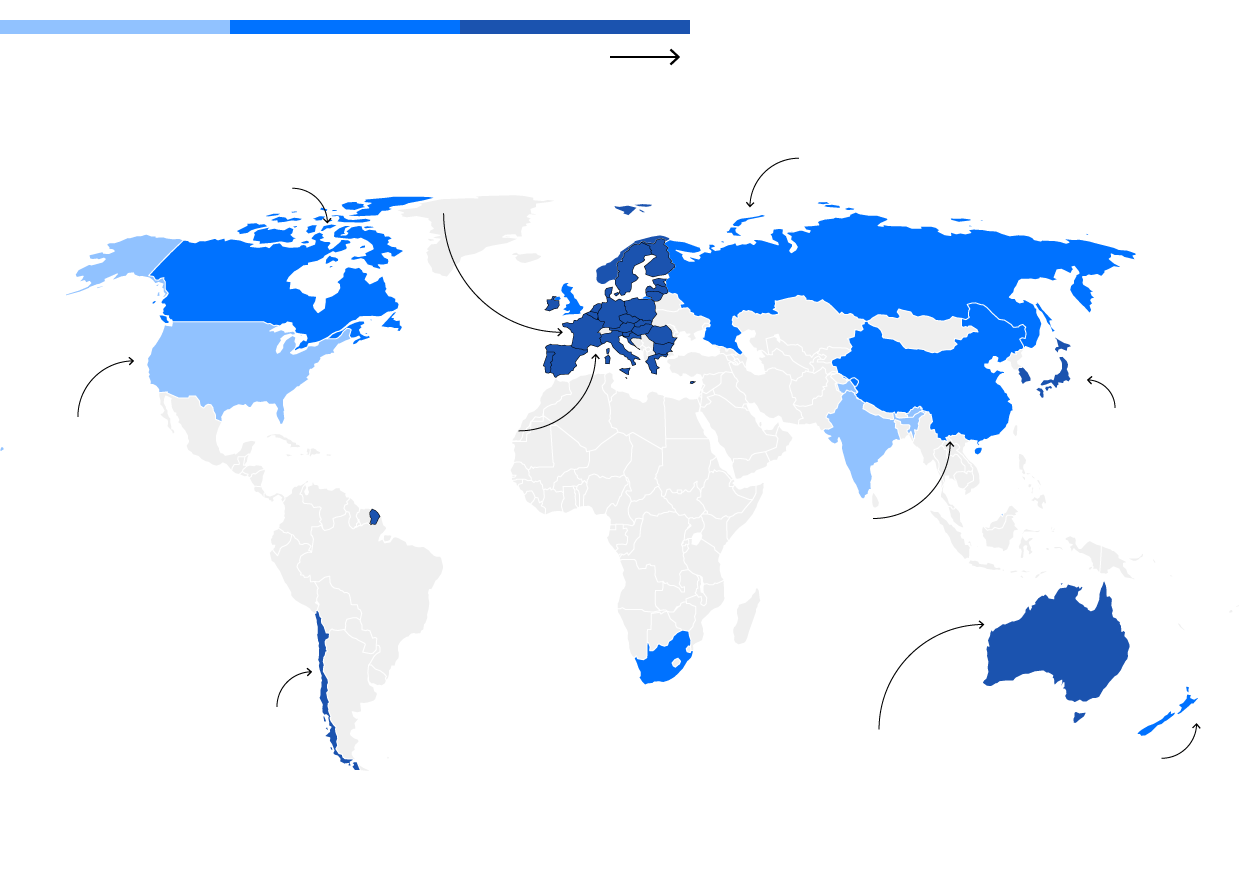

Australia

Aims to be among the top three exporters of hydrogen to

Asian markets by 2030

Brunei

Hydrogen demonstration plant; exports to Japan

Canada

Hydrogen could be used for 27% of primary energy needs

Chile

Aims to produce world’s cheapest green hydrogen by 2030

China

World’s largest producer, mostly from coal

EU

Aims to install 40GW of renewable hydrogen electrolyzers

by 2030

France

Hydrogen production capacity of 6.5GW through electrolysis

by 2030

Germany

$10B strategy outspends the rest

India

Plans to set targets but not currently part of renewable

energy aims

Japan

First to adopt a comprehensive strategy

Netherlands

Aims to scale up electrolysis to about 500MW of installed

capacity by 2025 and 3–4GW of installed capacity by 2030

Published a vision for hydrogen in 2019

New Zealand

Norway

Aims to increase number of hydrogen pilots and

demonstration projects

Portugal

Aims to close energy deficit, turn country into an exporter;

Sines project aims for 1GW capacity electrolyzers by 2030

Russia

The Nord Stream 2 gas pipeline could deliver hydrogen

to Europe

Wants to lead in the production and use of hydrogen vehicles

South Korea

Aims to install 4GW of electrolyzers by 2030

Spain

U.K.

Trials of hydrogen-powered train began in September

Most hydrogen production uses natural gas

U.S.

National hydrogen strategy, more robust plans

Aims to be among the top three exporters

of hydrogen to Asian markets by 2030

Australia

Brunei

Hydrogen demonstration plant;

exports to Japan

Hydrogen could be used to meet 27%

of country’s primary energy needs

Canada

Aims to produce world’s cheapest

green hydrogen by 2030

Chile

World’s largest producer, mostly from coal

China

EU

Aims to install 40GW of renewable

hydrogen electrolyzers by 2030

Hydrogen production capacity of 6.5GW

through electrolysis by 2030

France

$10B strategy outspends the rest

Germany

India

Plans to set targets but not currently

part of renewable energy aims

First to adopt a comprehensive strategy

Japan

Netherlands

Aims to scale up electrolysis to about

500MW of installed capacity by 2025,

3–4GW of installed capacity by 2030

Published a vision for hydrogen in 2019

New Zealand

Aims to increase number of hydrogen

pilots and demonstration projects

Norway

Portugal

Aims to close energy deficit, turn country

into an exporter; Sines project aims for

1GW capacity electrolyzers by 2030

Russia

The Nord Stream 2 gas pipeline could

deliver hydrogen to Europe

Wants to lead in the production and

use of hydrogen vehicles

South Korea

Aims to install 4GW of electrolysers

by 2030

Spain

U.K.

Trials of hydrogen-powered train began

in September

Most hydrogen production uses natural gas

U.S.

Note: Black outlines demarcate EU countries, and don’t necessarily indicate a national strategy exists.

National programs that are emerging have some of these EU traits. Portugal, for example, targets up to 2.5 gigawatts of electrolyzer capacity by 2030, using cheap solar and wind power to close its energy deficit and turn itself into an export hub. That includes production incentives, but also consumption-side support — like tax provisions — to encourage substitution, as well as plans to blend hydrogen into the gas network to stimulate demand.

That’s encouraging even if, as Rohitesh Dhawan of Eurasia Group points out, demand already exists, which means effort should focus on low-carbon production. Indeed, if we use green hydrogen in older industrial applications, rather than the grey type made from fossil fuels, we would already be seeing gains. Producing hydrogen currently amounts to around 830 million metric tons of carbon dioxide per year, according to the International Energy Agency, equivalent to Britain and Indonesia’s emissions combined.

There are still plenty of big questions, not least around funding. Globally, BNEF estimates the industry will need $150 billion of subsidies by 2030, and far more in investment overall. Portugal and Spain alone require a combined 14.8 billion euros, but as of October had committed less than 1 billion. Chile, which wants to produce some of the cheapest hydrogen from renewable electricity and become a leading exporter in the next decade, provides only $50 million in government funding for its plan, outlined last month.

It’s true that government support isn’t everything. Having legislation in place since 2006 hasn’t helped Argentina get very far, and a lack of federal support hasn’t stopped California. But it would help with a range of agenda items, from reaping security dividends to finding a role for hydrogen in developing countries with more fragmented energy systems.

Plenty of big economies, not least China and the U.S., have yet to outline granular plans and detailed support. There’s everything to gain from that jump start. Or hydrogen won’t get moving fast enough.