Big Oil Seeks Redemption in the Hydrogen Revolution

A three-part series on hydrogen energy

Photo: Bryan van der Beek/Bloomberg via Getty Images

What’s a fossil fuel company to do when the world is planning to give up on fossil fuels? Join the revolution, of course.

That helps explain the enthusiasm of Equinor ASA, Royal Dutch Shell Plc and PetroChina Co. about getting in on the switch to a hydrogen economy. For a century, oil companies have spent colossal sums of money delivering volatile liquid fuel to the power and industrial sectors. If hydrogen is supposed to replace petroleum in that equation, no one has better expertise than Big Oil.

That situation offers both opportunity and danger. As my colleague Clara Ferreira Marques has written, the European Union’s plans to spend 470 billion euros ($558 billion) switching to hydrogen by 2050 can sound almost impossibly ambitious. Still, the oil and gas sector typically spends around $500 billion developing new fields every single year. Shifting just a small share of the fossil fuel sector’s spending into hydrogen should be enough to drastically increase the technology’s scale and competitiveness.

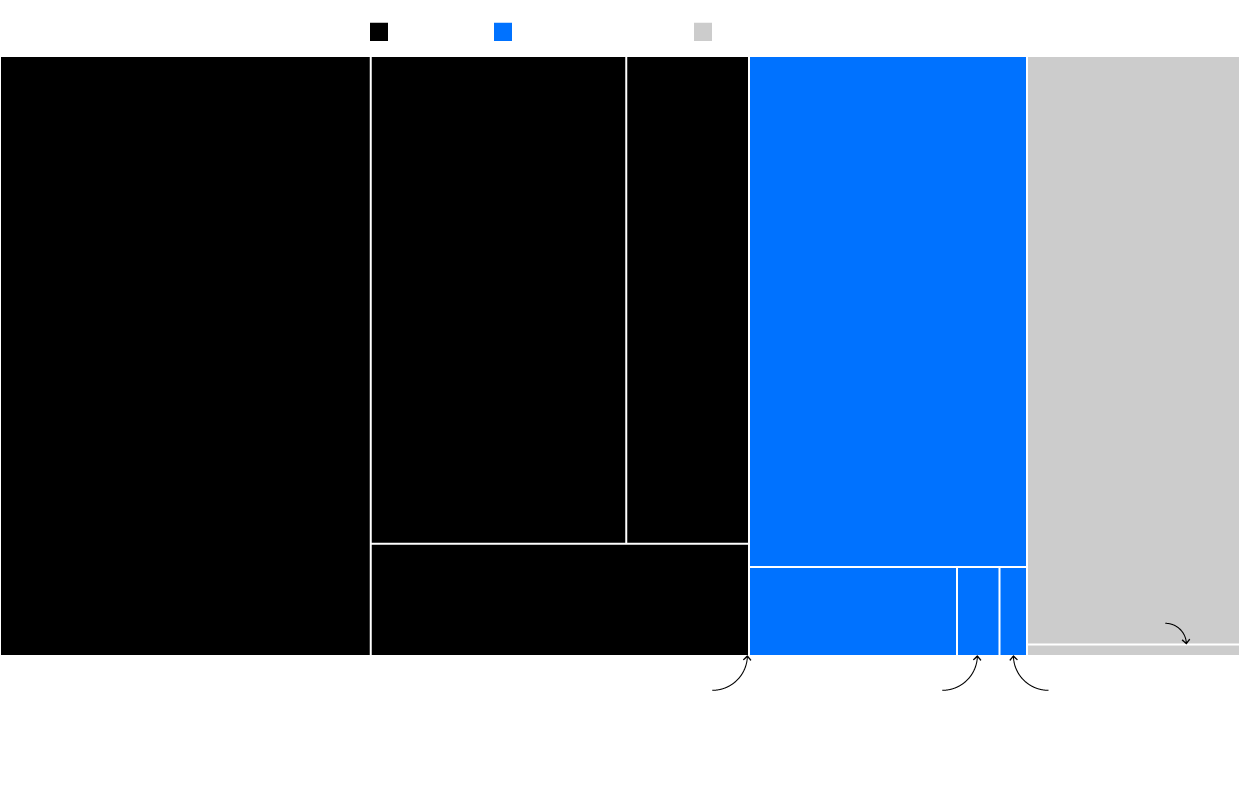

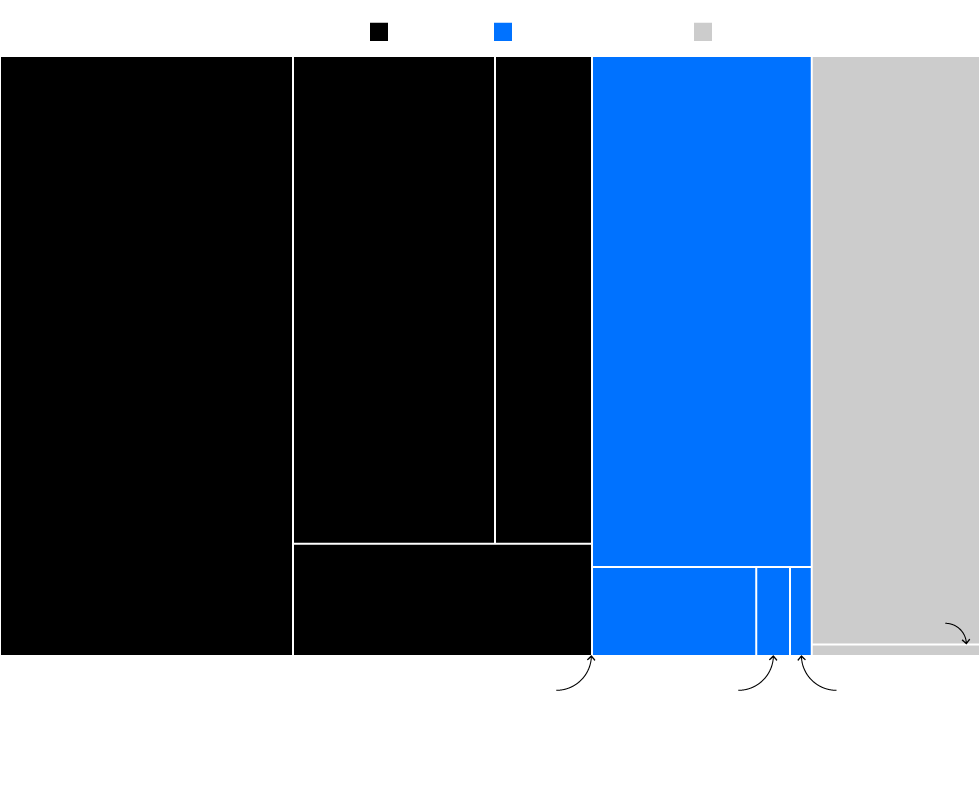

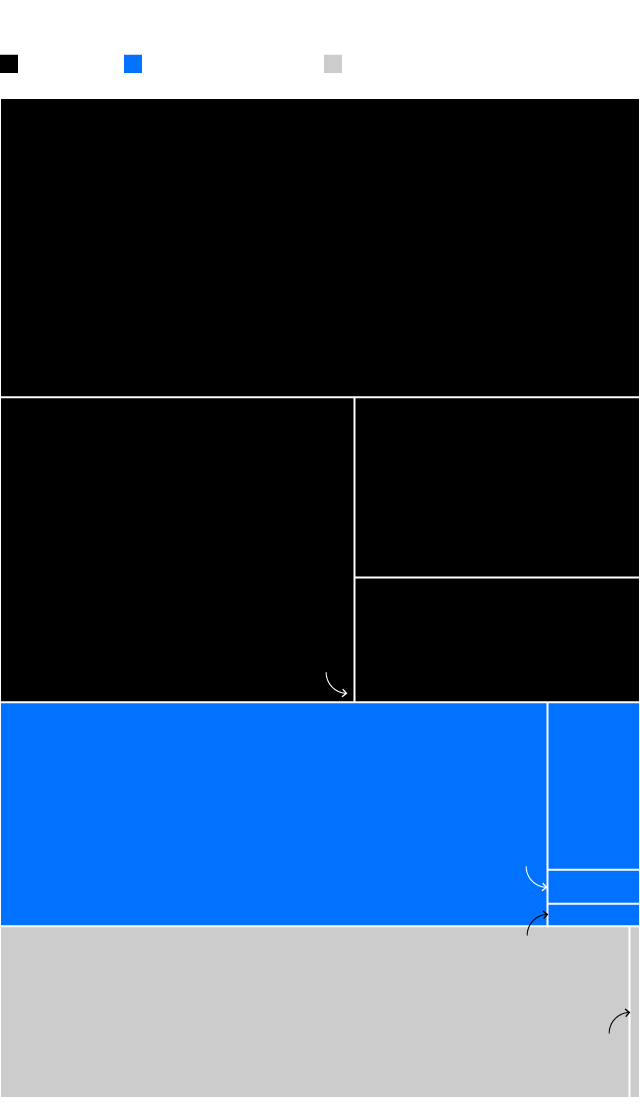

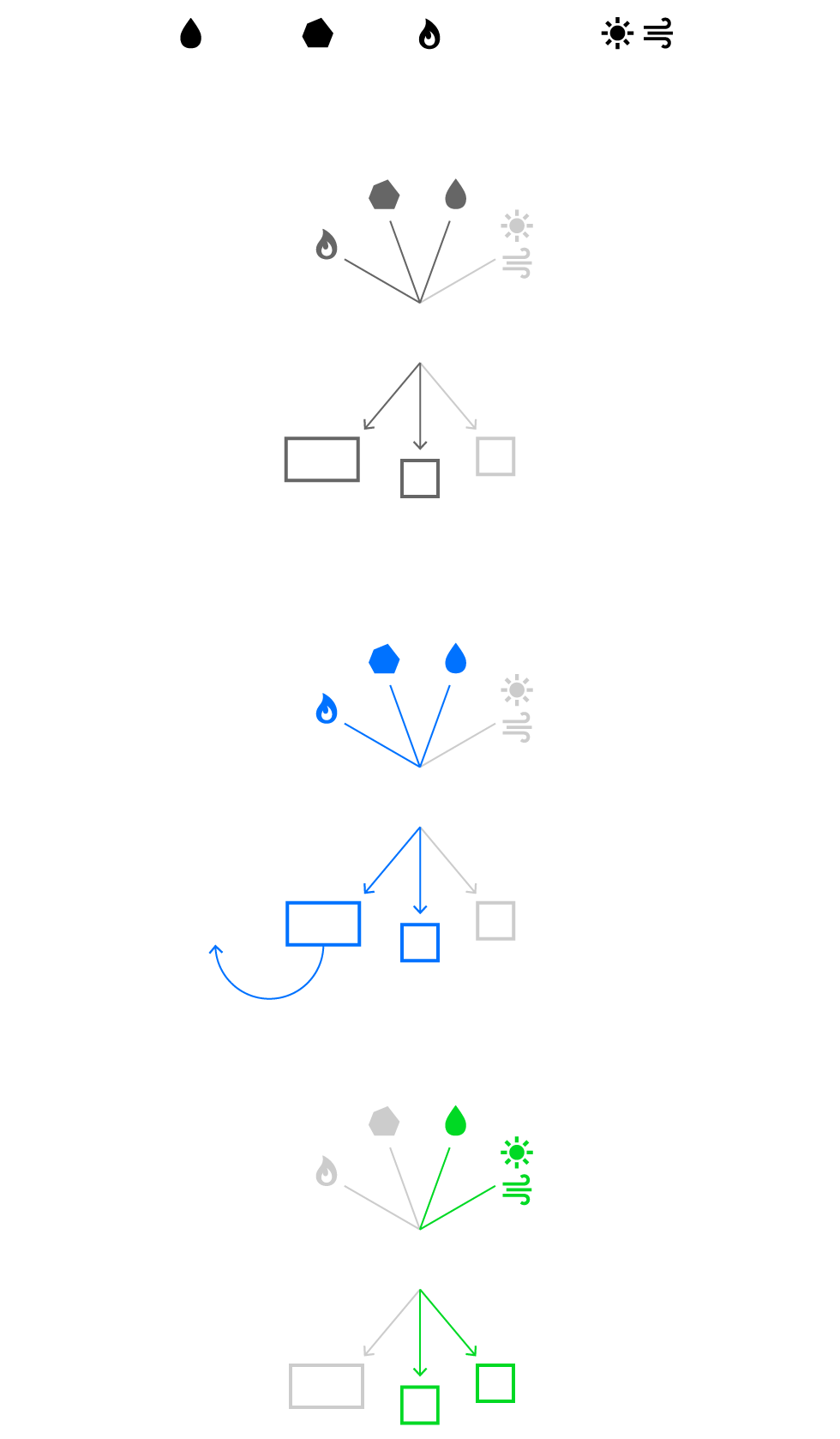

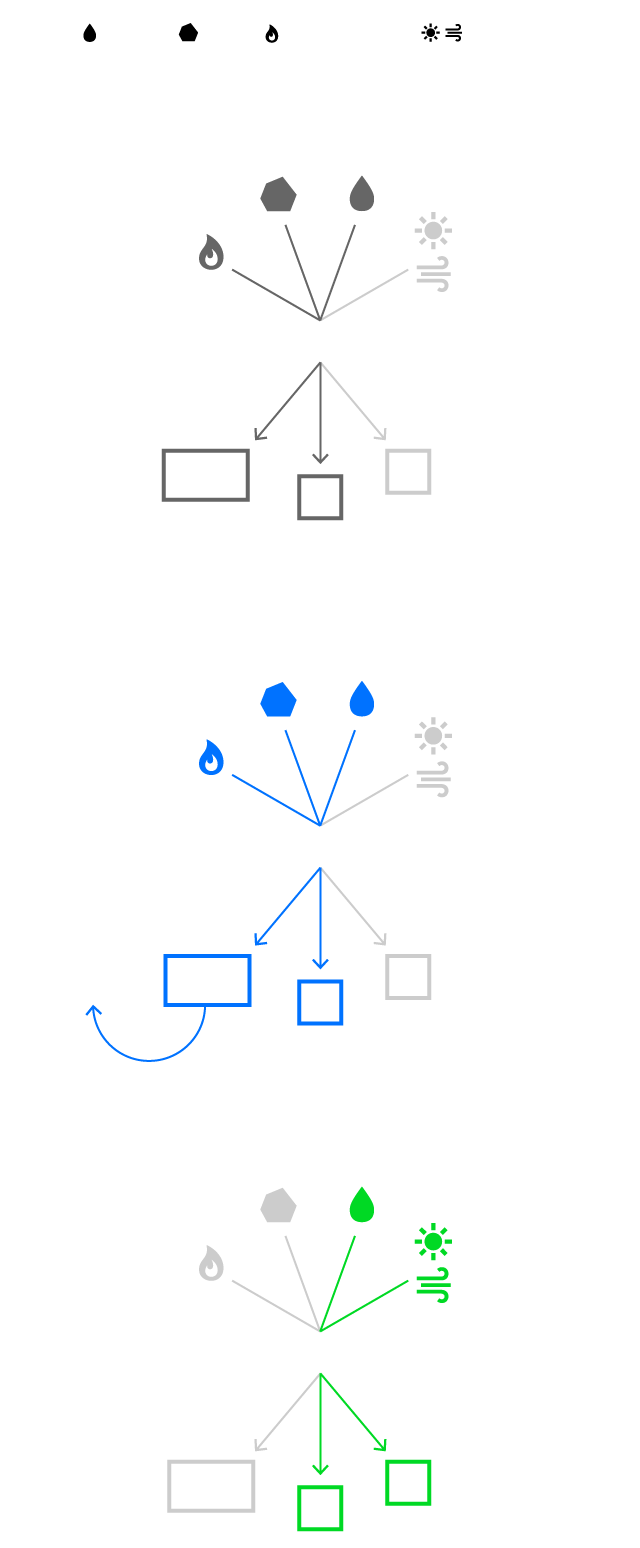

A Sense of Perspective

Global industry spending, 2019

Fossil

Zero-carbon

Grids

$483B

Oil, gas production

$273B

Midstream,

downstream

oil, gas

$131B

Fossil

power

$311B

Renewable power

$273B

Electricity

grids

$4B

Grid-scale

batteries

$90B

Coal production

$39B

Nuclear power

$100M

Industry carbon

capture, storage

$8B

Biofuels

production

$5B

Electric

vehicles

Global industry spending, 2019

Fossil

Zero-carbon

Grids

$483B

Oil, gas production

$273B

Midstream,

downstream

oil, gas

$131B

Fossil

power

$311B

Renewable

power

$273B

Electricity

grids

$4B

Grid-scale

batteries

$90B

Coal production

$39B

Nuclear

$100M

Industry carbon

capture, storage

$8B

Biofuels

production

$5B

Electric

vehicles

Global industry spending, 2019

Fossil

Zero-carbon

Grids

$483B

Oil, gas production

$273B

Midstream, downstream

oil, gas

$131B

Fossil power

$100M

Industry carbon

capture, storage

$90B

Coal production

$39B

Nuc-

lear

$311B

Renewable power

$8B

Biofuels

$5B

Electric vehicles

$273B

Electricity grids

$4B

Grid-scale batteries

Note: Doesn’t include end-use investment, except electric vehicles and carbon capture and storage.

The risk, though, is that Big Oil doesn’t really have the climate’s interests at heart. Blue hydrogen — produced from fossil fuels, but with its carbon dioxide byproduct sequestered underground or consumed in other processes — may offer an intermediate step toward zero-carbon green hydrogen. On the other hand, it may end up like coal power with carbon capture and storage: a technology hailed a decade ago as a promising way of reducing emissions but now seen as a costly dead end that provided cover for a last burst of dirty coal investment in Asia.

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon dioxide as a byproduct

Blue hydrogen captures and stores

most of the carbon dioxide output

Green hydrogen’s

byproduct is oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

CO

O

CO

O

CO

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon dioxide as a byproduct

Blue hydrogen captures and stores

most of the carbon dioxide output

Green hydrogen’s

byproduct is oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

CO

O

CO

O

CO

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil

fuels and produces carbon

dioxide as a byproduct

Blue hydrogen captures

and stores most of the

carbon dioxide output

Green hydrogen’s

byproduct is

oxygen

or

or

Gasifier/reformer

Gasifier/reformer

Electrolyzer

Carbon

capture,

storage

O

CO

CO

CO

O

O

2

2

2

H

H

H

Coal

Solar/wind

Raw materials:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon as a byproduct

or

Gasifier/reformer

CO

O

2

H

Blue hydrogen captures and stores

most of the carbon output

or

Gasifier/reformer

Carbon

capture,

storage

CO

O

2

H

Green hydrogen’s byproduct is oxygen

Electrolyzer

CO

O

2

H

Coal

Solar/wind

Inputs:

Water

Natural gas

Gray hydrogen uses fossil fuels and

produces carbon as a byproduct

or

Gasifier/reformer

O

CO

2

H

Blue hydrogen captures and stores

most of the carbon output

or

Gasifier/reformer

Carbon

capture,

storage

O

CO

2

H

Green hydrogen’s byproduct is oxygen

Electrolyzer

O

CO

2

H

With all the excitement around green hydrogen, there’s even a chance that we miss the strides being made by its highest-emission cousin, grey hydrogen — in particular the variety made from gasification of coal. That process already accounts for about 5% of China’s coal consumption. India will invest 4 trillion rupees ($54 billion) in the technology by 2030, with an aim of converting 100 million metric tons to natural gas and chemicals, coal minister Pralhad Joshi said earlier this year.

Not So Clean

Emissions ranges for hydrogen energy and fossil fuels

e/MJ

0

20

40

60

80

100g CO

2

Blue: gas

Natural gas

Crude oil

Coal

Grey: gas

Green

Emissions ranges for hydrogen energy and fossil fuels

e/MJ

100g CO

0

20

40

60

80

2

Blue: gast

Natural gas

Crude oil

Coal

Grey: gas

Green

Emissions ranges for hydrogen energy and fossil fuels

0

25

50

75

100g CO

e/MJ

2

Blue:

tgas

Natural

gas

Crude

oil

Coal

Grey:

gas

Green

Note: Hydrogen with as little as 36.4 grams CO2e/MJ is counted as “grey hydrogen,” but most emits considerably more.

A first step for investors is to make careful distinctions between the types of projects and their progress toward being built. Those concerned about decarbonization should treat all announcements of downstream spending (such as vehicle fueling networks) with a pinch of salt. In most cases, there’s no guarantee that they won’t just use grey hydrogen — which is usually more carbon-intensive than traditional fossil alternatives. That’s particularly the case in countries like China and India, where governments may see grey gas produced from coal as the best way to support jobs in a declining local mining industry while reducing dependence on imported petroleum.

Pressure Drop

Hydrogen energy cost ranges

0

1

2

3

4

5

6

7

$8/kg

Grey: gas

Grey: coal

Blue: gas

Green

Hydrogen energy cost ranges

0

1

2

3

4

5

6

7

$8/kg

Grey: gas

Grey: coal

Blue: gas

Green

Hydrogen energy cost ranges

0

2

4

6

$8/kg

Grey: gas

Grey: coal

Blue: gas

Green

More importantly, though, Big Oil needs to recognize what it can bring to the party and where it’s not needed. The key area of overlap between the current petroleum economy and a hydrogen future is likely to be in midstream infrastructure: pipelines, ships and storage facilities.

Salt caverns — artificial caves already widely used to store oil and gas, including the U.S. strategic petroleum reserve — are likely to be critical nodes in the hydrogen network. A few are already in use for industrial hydrogen, but many more will be needed. One study earlier this year estimates there’s capacity to store about 7.3 petawatt-hours of hydrogen in salt caverns near Europe’s coasts, equivalent to nearly two years of the continent’s electricity demand. Depleted oilfields can play a similar role in areas where salt formations aren’t available. No industry understands this geology better than the petroleum sector.

Engineered infrastructure will also be crucial. In the Netherlands, a consortium including Shell is planning to put green hydrogen produced by a giant 10-gigawatt offshore wind farm through pipelines serving the declining Groningen gasfield, which would otherwise be scrapped. At the port of Rotterdam, another group is hoping to spend about 2 billion euros re-powering the local industrial cluster with blue hydrogen instead of conventional fuel.

Still, the most important role for fossil fuels may prove more humdrum. For all Big Oil’s technical expertise, its dominant position in the existing energy system may prove most critical. Some 84% of the world’s primary energy still comes from oil, gas and coal. That gives fossil fuel companies an outsize share of cashflow and investment dollars — and, as we’ve argued, more spending is what’s needed to make green hydrogen competitive with dirtier alternatives.

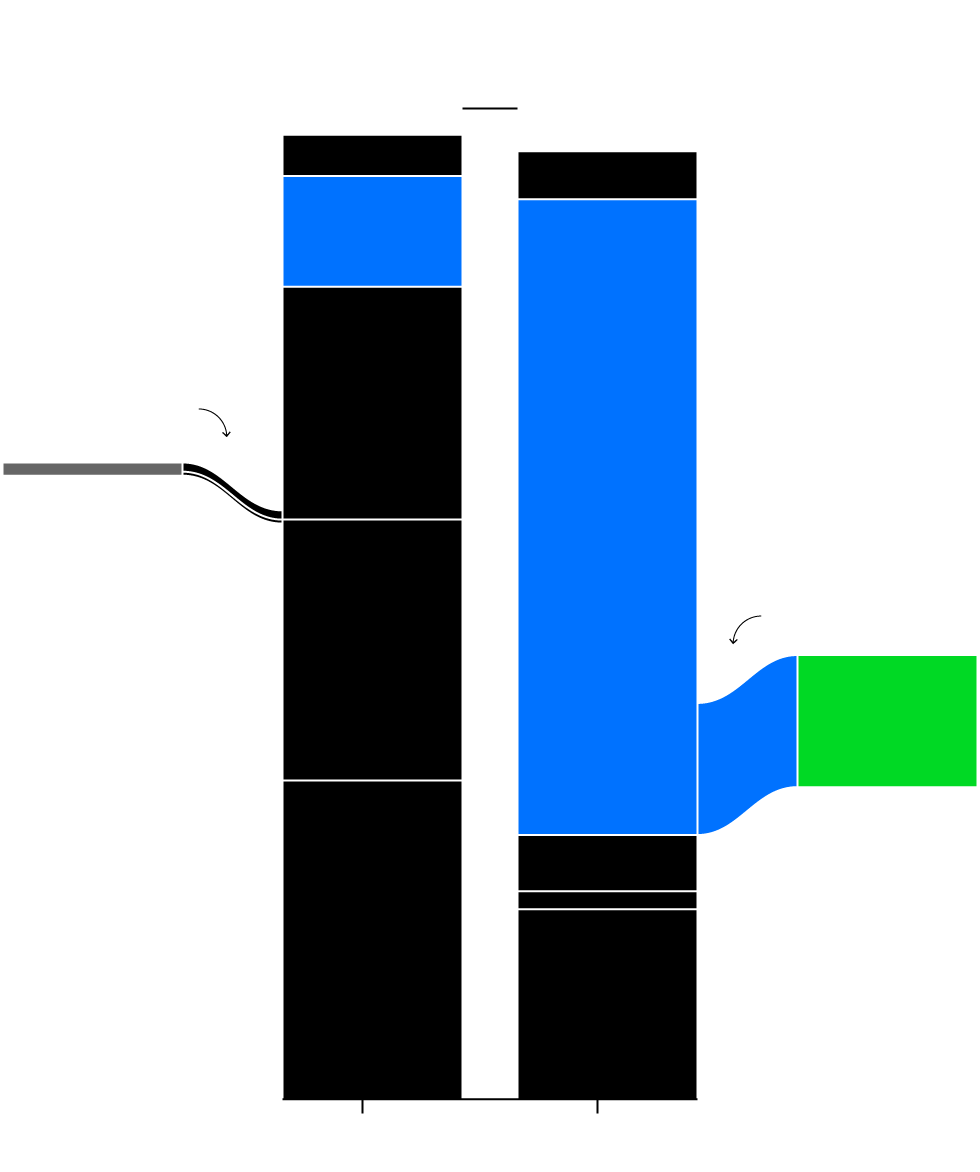

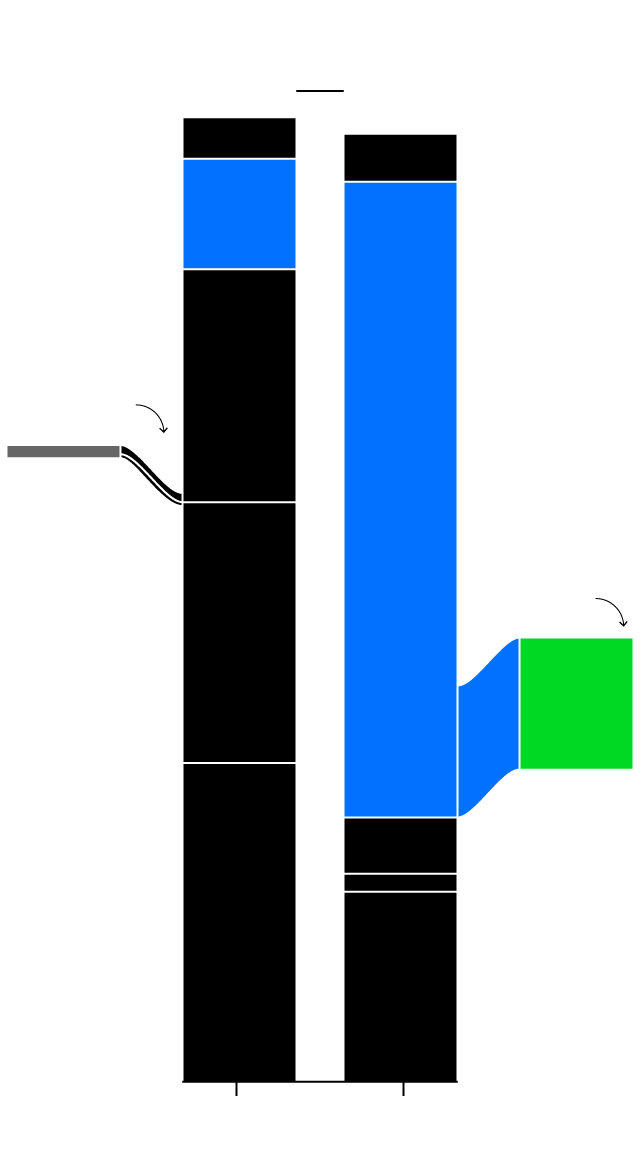

The scale of the challenge is vast. The world will need to produce 80 exajoules of hydrogen a year by 2050, according to the Hydrogen Council. Doing that with electrolyzers, the only viable zero-carbon pathway, would require more electricity than the entire world produced in 2019. That will need about nine times more wind and solar generators than exist worldwide to date, according to BloombergNEF.

Gas Bubble

Energy generated

600 exajoules

Nuclear

Nuclear

Renewables

Currently, most

hydrogen energy

is made from gas

and coal, about

8 exajoules

All hydrogen

energy should

be made from

renewables

by 2050, about

80 exajoules

Natural gas

Gray hydrogen

Renewables

Coal

Green

hydrogen

Natural gas

Coal

Oil

Oil

0

2019

2050 forecast

Energy generated

600 exajoules

Nuclear

Nuclear

Currently, most

hydrogen

energy is made

from gas and

coal, about

8 exajoules

Renewables

By 2050, all

hydrogen

energy

should be

made from

renewables

about 80

exajoules

Natural gas

Gray hydrogen

Renewables

Coal

Green

hydrogen

Natural gas

Coal

Oil

Oil

0

2019

2050 forecast

Energy generated

600 exajoules

Nuclear

Nuclear

Renew-

ables

Most

hydrogen

energy is

made from

gas and coal,

about 8

exajoules

By 2050, all

hydrogen

energy

should be

made from

renewables,

about 80

exajoules

Natural

gas

Gray

hydrogen

Renew-

ables

Coal

Green

hydrogen

Nat. gas

Coal

Oil

Oil

0

2019

2050 forecast

It’s going to prove difficult to do that without a spending boom that will make the past decade’s outlay on renewable power look modest. Still, if there’s any industry that’s in a place to deliver such a splurge, it’s one that’s been synonymous with bold, transformative investment since the days of John D. Rockefeller. To conquer the 21st century energy industry, oil’s giants should remember the lesson of their rise to dominance in the 19th: Go big, or go home.