Debt, Conflict and Vacancy Imperil Kushners’ Times Square Dream

Jared Kushner’s family averted disaster last year when a Canadian asset manager swooped in to buy their skyscraper in midtown Manhattan, which had been hemorrhaging millions of dollars. Now they’re facing a similar crisis a few blocks away.

At the former New York Times building on West 43rd Street, a graying property in Times Square, the pattern is uncannily similar: Buy at a steep price, pile on too much debt, run up big losses, fight with tenants and flirt with default.

It’s the latest example of overreach for a family that built a fortune on suburban rental properties, only to have its urban ambitions stymied. Kushner Cos. bought the first six floors of the Times building for $296 million in 2015, envisioning a multifloor amusement park in the heart of Times Square. Four years later, a toxic brew of debt, conflict and vacancies has put their investment in jeopardy.

Think of the building as a vertical mall with three-story neon signs beckoning tourists. There are tenants the Kushners inherited: a sprawling sushi restaurant, a below-ground Guitar Center store and a two-story bowling alley with thumping music. And ones they brought in—in the basement, National Geographic Encounter, an exhibit about oceans with humpback whales and sea lions cavorting on digital screens; on the second floor, Gulliver’s Gate, featuring detailed miniatures of the Colossus of Rhodes, the Empire State Building, Jerusalem’s Western Wall and other famous sites, complete with miniature trains and glowing skyscrapers.

The Kushners’ new tenants have a few things in common, including ticket prices exceeding $30, underwhelming crowds and financial trouble. The National Geographic exhibit has paid only partial rent since August, and the Kushners are looking for a new tenant. Gulliver’s Gate paid irregularly, prompting a legal battle that resulted in its rent being cut by almost half this year. Take a walk around the back of the building, and there’s a dusty unfinished space meant for a champagne bar. It never opened. Kushner Cos. has traded lawsuits with the proprietor, an operator of airport restaurants that is alleging fraud, claims the Kushners have denied.

A spokeswoman for the National Geographic exhibit confirmed that the attraction wasn’t paying full rent, but she declined to provide details. Gulliver’s Gate founder Michael Langer said he was “happy we were able to work together for an amicable agreement.” A spokesman for OHM Concession Group, which leased space for the champagne bar, didn’t respond to requests for comment.

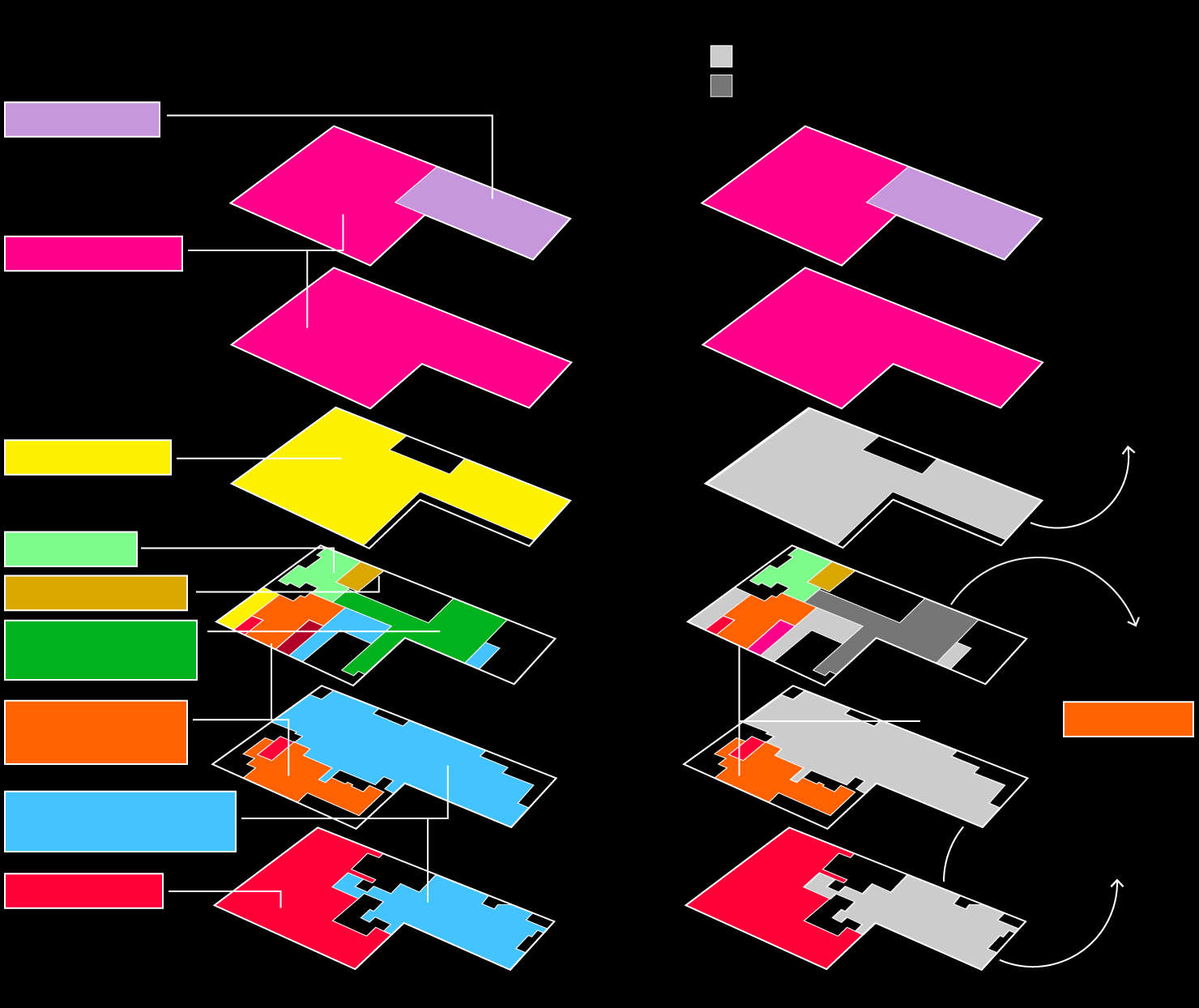

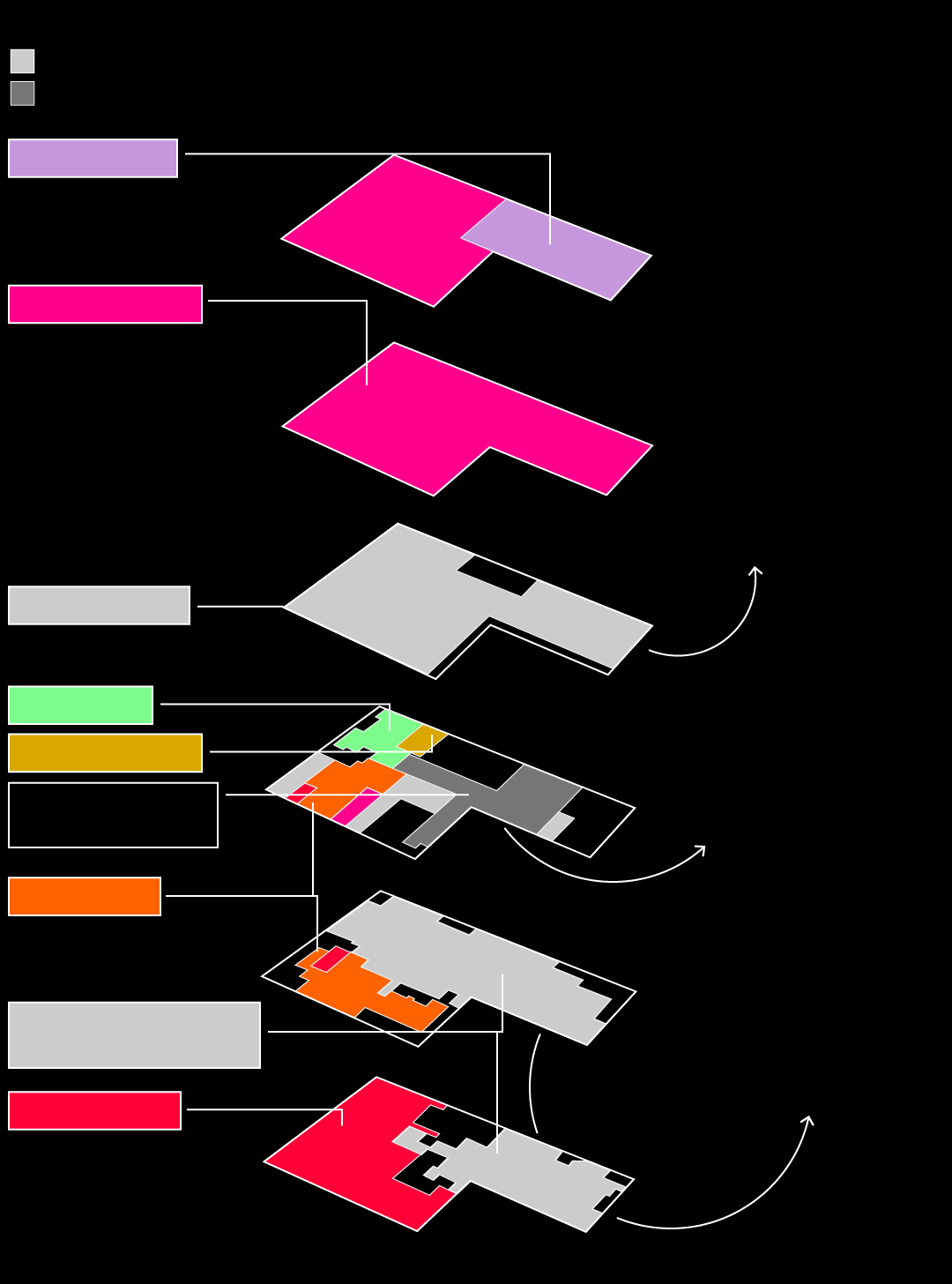

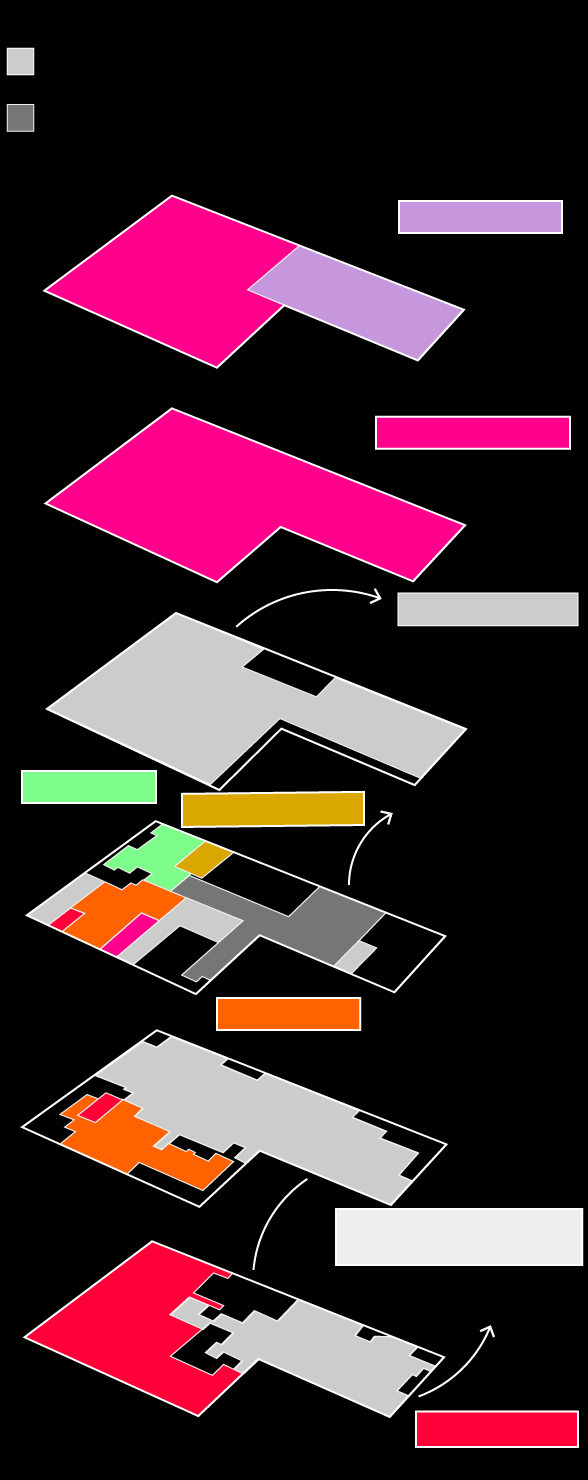

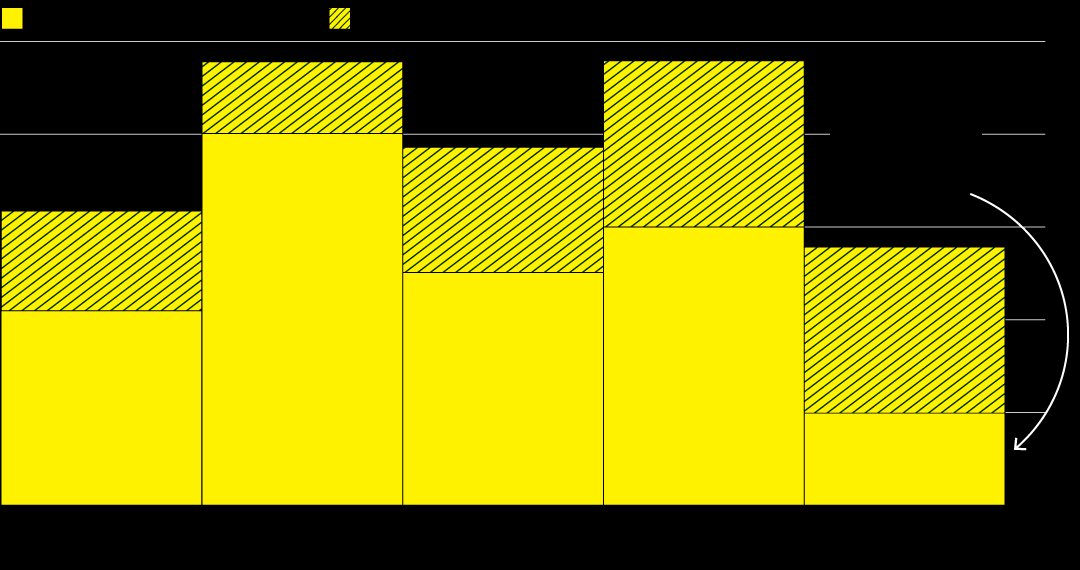

Leased tenants at 229 West 43rd St. at time of 2016 loan

Current tenants

Rental income lower than projected in 2016

Currently empty

Office Condo

4th floor

Bowlmor Lanes

After trading lawsuits, got rent cut by nearly half

3rd floor

2nd floor

Gulliver’s Gate

Haru Sushi

Ground

floor

Los Tacos No. 1

American Market

by Todd English

Never moved in

Cellar

floor

Replaced by The Ribbon

Guy’s American Kitchen+Bar

National Geographic Ocean

Encounter

Hasn’t paid full rent since August 2018

Subcellar

floor

Guitar Center

Leased tenants at 229 West 43rd St. at time of 2016 loan

Current tenants

Rental income lower than projected in 2016

Currently empty

Office Condo

4th floor

Bowlmor Lanes

3rd floor

After trading lawsuits, got rent cut by nearly half

2nd floor

Gulliver’s Gate

Haru Sushi

Ground

floor

Los Tacos No. 1

American Market

by Todd English

Never moved in

Cellar

floor

Guy’s American

Kitchen+Bar

Replaced by The Ribbon

National Geographic

Ocean Encounter

Hasn’t paid full rent since August

Subcellar

floor

Guitar Center

Current tenants at 229 West 43rd St.

Rental income lower than projected at time of 2016 loan

Currently empty

Office Condo

4th floor

Bowlmor Lanes

3rd floor

After trading lawsuits, got rent cut by nearly half

2nd floor

Gulliver’s Gate

Haru Sushi

Ground

floor

Los Tacos No. 1

Never moved in

American Market

by Todd English

The Ribbon

Cellar

floor

National Geographic

Ocean Encounter

Hasn’t paid full rent since August

Subcellar

floor

Guitar Center

Current tenants at 229 West 43rd St.

Rental income lower than projected at time of 2016 loan

Currently empty

4th floor

Office Condo

3rd floor

Bowlmor Lanes

Gulliver’s Gate

2nd floor

After trading lawsuits, got rent cut by nearly half

Haru Sushi

The American Market by Todd English never moved in

Los Tacos No. 1

Ground

floor

Blue Ribbon

Cellar

floor

National Geographic

Ocean Encounter

Subcellar

floor

Hasn’t paid full rent since August 2018

Guitar Center

The missteps have added up. Kushner Cos. assumed that all these tenants would be paying rent when it piled $370 million of loans onto the building in an October 2016 refinancing, most of it from Deutsche Bank AG. In March, the company defaulted on one high-interest chunk of its debt to other lenders, and the property has often run at a loss after accounting for loan payments, according to data compiled from disclosures to investors. While there’s always room for improvement, spaces for so-called experiential retailers require custom designs and can take years to fill.

The story of how the Kushner family purchased a Times Square building only to see it founder during an economic boom is one of zealous overconfidence and a passion for trophy properties, according to more than a dozen people interviewed by Bloomberg News. It’s also a tale of how the real estate market encourages excessive risk-taking, rewarding those who use steep leverage on speculative properties even as they pass potential losses to others. Most of the debt on the Times building has been transferred to investors – it’s their problem now. Meanwhile, Kushner Cos. allocated some of the loan to pay itself $59 million, according to public filings.

Wells Fargo & Co., which manages the loan, has placed it on a watchlist for troubled debt and taken control of the property’s accounts. At one point, the building also drew the attention of federal prosecutors. The U.S. attorney for the Eastern District of New York subpoenaed records about the refinancing in 2017. What investigators were looking for, whether the Kushners were a subject and if the matter is ongoing is unclear. Spokesmen for Deutsche Bank and Wells Fargo declined to comment, as did Jared Kushner’s attorney, Abbe Lowell. Representatives for Kushner Cos. didn’t respond to numerous requests for comment.

The former Times building and Kushner Cos. were both struggling when they came together in 2015. The 18-story landmark with a mansard roof had been the newspaper’s headquarters for almost a century, until the company moved a few blocks away in 2007. That same year, Africa Israel Investments Ltd. bought the building at 229 West 43rd St. for $525 million and began searching for a way to repurpose it, exploring everything from luxury condos to a Disney-themed hotel. When those plans fizzled, the company, led by Russian-Israeli diamond merchant Lev Leviev, decided to sell part of the site as a retail complex.

The rapid growth of internet shopping made many real estate investors skeptical. But Charles Kushner, founder of the company that bears his name and father of now-presidential adviser Jared Kushner, was still bullish on retail when Leviev’s brokers pitched him. He had reason for his optimism. In 2011, as Kushner Cos. was straining under a mountain of debt at its 666 Fifth Ave. skyscraper, selling the building’s stores for $1 billion helped pay off some of it and buy time.

Four years later, 666 Fifth Ave. was again operating at a loss. The Kushners were supposed to have improved the property and raised rents. Instead, they had been shopping a plan to knock it down and build a glittering high-rise twice as tall with a five-story shopping center at its base.

The Kushners needed an infusion of cash, and the bottom six floors of the Times building offered a tantalizing opportunity. Tens of thousands of people walk by daily. The building was about half leased, but if the family could fill it quickly and bolster its rent rolls, Kushner Cos. could refinance at a higher valuation, taking any gains as profit.

Charles Kushner’s view wasn’t widely shared, and financing the deal was a struggle. The company considered selling a Chicago office building it owned and sheltering the gains from the sale in the Times Square property, a common tax-planning strategy known as a 1031 exchange, according to a person familiar with the matter. But the Chicago sale never materialized, so the Kushners turned to well-capitalized firms they’d done business with in the past. None accepted the invitation to join them as an equity partner, the person said.

In the end, they relied almost exclusively on loans – all but $1 million of the $296 million purchase price was covered by debt, most of it from a division of Brookfield Asset Management Inc., the Canadian real estate company that would later rescue the Kushners by taking out a 99-year lease on 666 Fifth Ave. for $1.3 billion.

Theoretically, anything goes in Times Square, where Madame Tussauds’ lifelike wax sculptures and Mars Corp.’s shrine to M&M’s have co-existed for more than a decade. But it’s also possible to miscalculate. Leviev had made a go of it with the horror-themed Jekyll & Hyde Club. It closed amid terrible reviews months before the Kushners bought the property.

The building’s spaces in the basement and upper floors were slower to lease than anticipated, and by time the Kushners took control in 2015, the property remained about half leased. At Kushner Cos. headquarters in 666 Fifth Ave., Charles Kushner was frustrated that the building was still losing money, according to one person who heard him complain. Jared Kushner, the company’s chief executive officer at the time, told staff that they needed more cash flow, the person recalled, and that they needed it quickly.

The Kushners found it. The first big tenant to sign was Gulliver’s Gate, which had been in talks with Leviev. Plans for an aquarium were scuttled after other tenants complained about potential water damage and fishy aromas. Then came SPE Partners, an entertainment development company with a license from National Geographic, which would take about 60,000 square feet for a waterless and odor-free exhibit. A tiny storefront was leased to Los Tacos No. 1, a popular Mexican taqueria. Airport restaurant operator OHM signed on for a champagne bar, meaning the building was fully leased by August 2016.

The safest buildings to lend to have longtime tenants with proven ability to pay the rent. But the Kushners filled the Times Square property with one-of-a-kind tourist attractions, most of them untested businesses posing unique risks.

“We’re not Gap or Apple, not one of those companies that is known to the market,” Eiran Gazit, a co-founder of Gulliver’s Gate, explained in a November phone interview. “We are a private company and small. There were some landowners who turned us down and are still empty. The Kushners were willing to accept us.” Gazit, who left the company last year and doesn’t speak for the business, said he had met with 17 property owners before signing with the Kushners.

Still, it was a booming market, and Deutsche Bank’s commercial-mortgage unit, which issued a total of $11 billion of New York real estate loans in 2015, was eager to help.

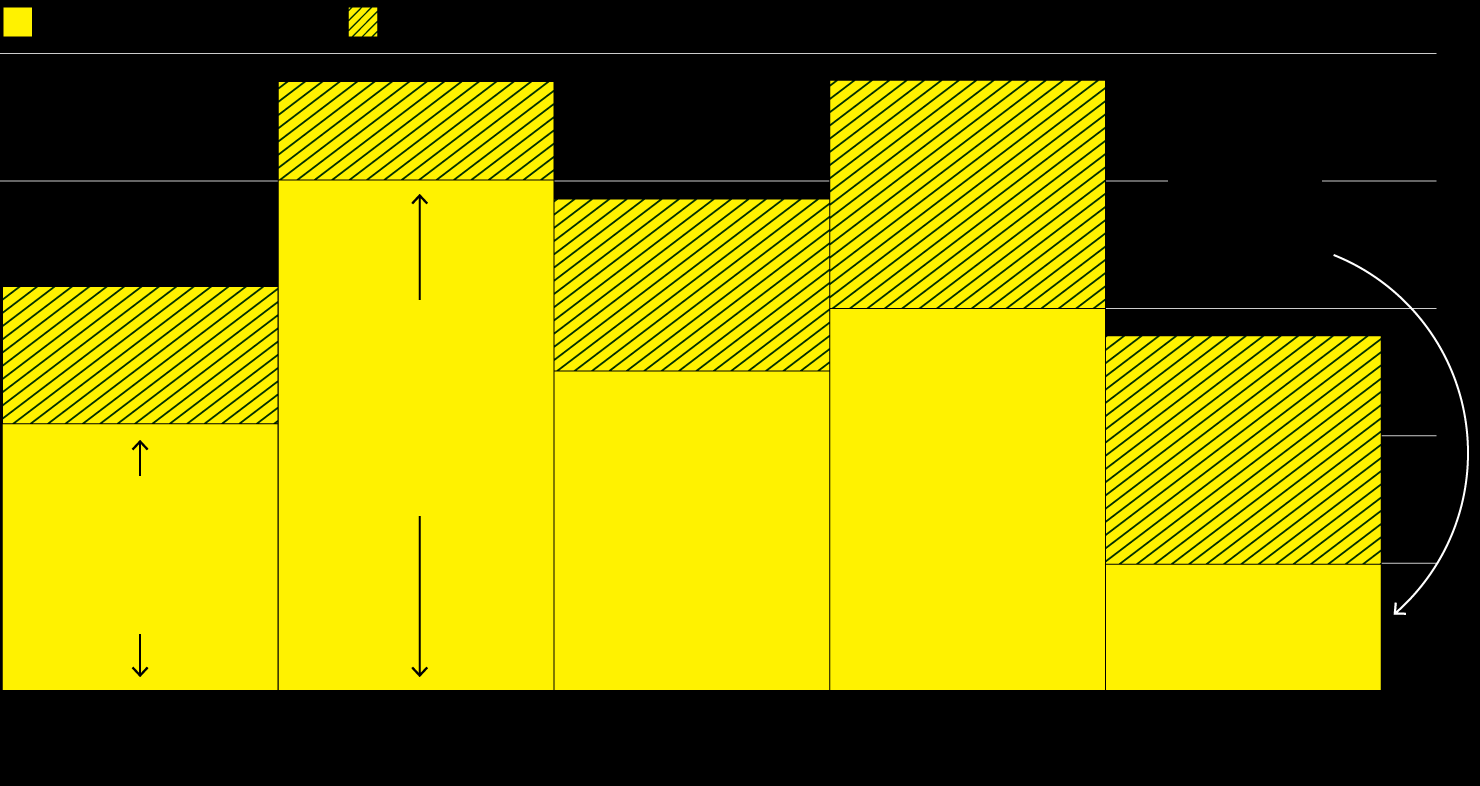

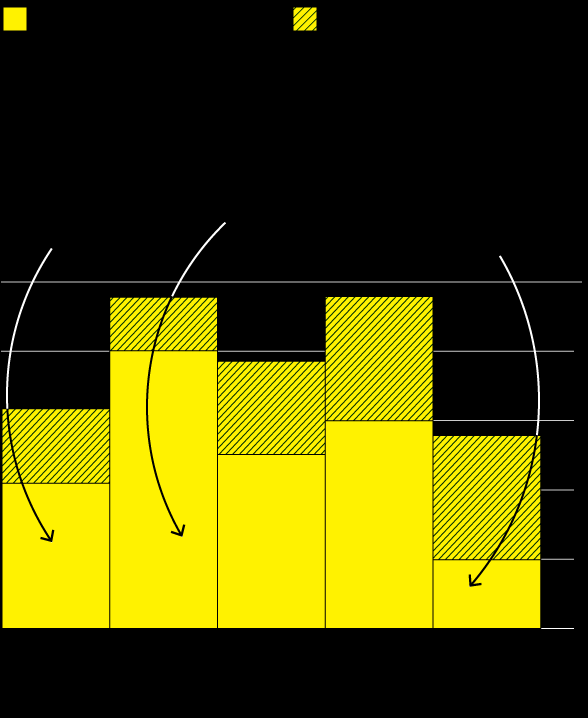

How much was the building worth? That hinged on how much it would make. Total rent of $16 million in 2014, when much of the property was empty, was too conservative. Now that it was fully leased, the Kushners expected $24 million annually, according to a prospectus prepared in connection with the refinancing. Bankers were also optimistic about the Kushners’ ability to slash expenses to $3.9 million a year, about $1.5 million less than 2014, the prospectus said. With an enlarged rent roll and an austere cost structure, net operating income would almost double to $21.5 million, enough to cover about $18 million in interest payments.

Accepting those lofty numbers required no small amount of faith. Only two of the new tenants had moved in, and none was yet paying rent. Nonetheless, the net income figure was used to appraise the property at $470 million, according to the loan documents. By that math, the Kushners had increased its value more than 50% in one year.

The Kushners’ looming income crash

Net operating income

Expenses

$25M

20

If National Geographic leaves and space remains vacant

15

A Deutsche Bank prospectus projected NOI would almost double, implying a $470 million valuation

10

The building’s net operating

income before its

purchase for $296 million in 2015

5

0

2014

2016

(projected)

2017

2018

Starting April 2020*

(projected)

Net operating income

Expenses

$25M

If National Geographic leaves and space remains vacant

20

15

A Deutsche Bank prospectus projected NOI would almost double, implying a $470 million valuation

10

The building’s NOI before its purchase for $296 million in 2015

5

0

2014

2016

(projected)

2017

2018

Starting April 2020*

(projected)

Net operating income

Expenses

A Deutsche Bank prospectus projected NOI would almost double, implying a $470 million valuation

The building’s NOI before its purchase for $296 million in 2015

If National Geographic leaves and space remains vacant

$25M

20

15

10

5

0

2014

2016

(projected)

2017

2018

Starting

April 2020*

(projected)

At that valuation, the $370 million of loans they received in the refinancing looked sober. Most of that amount was used to pay off the existing Brookfield mortgage, with another $26 million placed into reserves. But $59 million went as a payout to Kushner Cos., an astounding return on its original $1 million investment.

“In less than a year, we’ve repositioned the property and transformed it into a top-flight entertainment destination,” Kushner Cos. President Laurent Morali told the Commercial Observer, the trade publication owned by the Kushner family, which broke the news.

The Kushners inauspiciously held their 2016 holiday party at the site of their financial coup: Guy’s American Kitchen & Bar on the West 44th Street side of the Times Square building. The restaurant—named for spiky-haired restaurateur and TV personality Guy Fieri—was the subject of a scathing New York Times review that described a watermelon margarita that tastes like “radiator fluid and formaldehyde.” It would close a year later.

But the Kushners were just at Guy’s for the cavernous space: They brought in a kosher caterer. They had plenty to celebrate. Jared’s father-in-law was going to the White House, the Times Square refinancing was complete, and the family was closing in on a deal with a Chinese insurer to save the overleveraged 666 Fifth Ave.

It was a bittersweet occasion, according to two people who attended. As Charles Kushner hobnobbed with other New York real estate barons, Jared, who would soon be leaving for Washington and stepping away from day-to-day operations, said his goodbyes.

The euphoria didn’t last. In March 2017, Anbang Insurance Group Inc., the Chinese insurer, pulled out of the deal, and Jared’s interactions with the CEO of a Russian state-owned bank came under scrutiny. That led to journalists asking questions about the involvement of Deutsche Bank and Leviev, who’s friendly with Russian President Vladimir Putin.

At the Times building, the first signs of strain emerged that September. Passersby could peek through windows where the champagne bar was scheduled to open months earlier. The space was empty and unimproved. No work was being done. Wells Fargo, which became manager of the loan after the refinancing, put the property on its watchlist, citing lower-than-expected income to cover debt payments. It was an ignominious designation. And then things got worse.

If there’s one common complaint the Kushners’ Times Square tenants have about their landlord, it’s that the company promised more than it delivered.

For OHM, the dispute was about a hallway. The company said in a lawsuit filed in New York Supreme Court that it was promised the space for its champagne bar, but it turned out it was needed for shared use. The hallway covered about 2,000 square feet, or one-sixth of the leased space, according to the suit, which accused Kushner Cos. of fraud and breach of contract. The company denied the claims as “salacious and false” and evicted OHM for failing to open on time. The litigation is ongoing.

Gulliver’s Gate alleged in a lawsuit that Kushner Cos. billed it for 5,700 square feet more than it actually had. The company, which disputed the allegation in court papers, sued the attraction for nonpayment of rent.

The attraction had its own share of troubles as business got off to a rocky start. It missed payments to Kushner Cos. and other vendors. But Gulliver’s Gate had one advantage: A space like the one it occupied on the second floor could take years to fill and would require more cash from the Kushners in the form of tenant improvements and a free-rent period after a new tenant moved in. In April, after a months-long legal battle, Charles Kushner capitulated and agreed to cut the rent by almost half starting early next year.

The battle over the National Geographic exhibit hasn’t spilled into court. But it has been costly. SPE Partners stopped paying full rent in August amid a dispute over shared expenses and racked up more than $3 million in unpaid bills by late last year, according to Wells Fargo. Lenders have approved the lease termination, and the space is now being marketed. Still, lenders won’t let the Kushners evict the exhibit, fearing a hole too big to fill, according to a person familiar with the matter. In April, Kushner Cos. told lenders it expects the digital dolphins to remain in place “for a few more months,” Wells Fargo told investors.

One of the National Geographic exhibit’s biggest backers, Fairfax, Virginia-based real estate firm Peterson Companies, sold its stake late last year. A person familiar with the deal said the company didn’t want to continue pouring money into a venture that had lost millions. Angela Sweeney, chief marketing officer for Peterson, said the separation was amicable and declined to comment on the terms.

As the hits came, Kushner Cos. missed a March payment on an $85 million mezzanine portion of its loan, which was promptly restructured on terms that haven’t been disclosed. Last year’s expenses, about $9 million, were more than twice estimates, according to Wells Fargo data. OHM’s absence and Gulliver’s reduced rent have chopped about $5 million off the revenue estimates, and a National Geographic exit could more than double that figure. If that situation doesn’t change, the building won’t be able to cover debt payments.

If the worst happens and the Times Square building goes belly-up, Kushner Cos. and Deutsche Bank won’t bear the brunt of it. That’s because the Kushners put so little money down and took out so much, and because Deutsche Bank sold most of the debt soon after it was issued.

Losses would instead be borne by a broad base of investors, most of whom probably don’t even know they’re exposed. The debtholders are now a series of trusts that also hold other commercial mortgage loans. Those trusts were sliced up and sold to investors as commercial mortgage-backed securities, similar in structure to vehicles that hold home loans.

The Times Square loan has an extra wrinkle that makes things even riskier for its new owners. Kushner Cos. pays only interest until the loan comes due in 2026. The company had a similar deal at 666 Fifth Ave. In the wake of the financial crisis, the issuance of such interest-only loans diminished. But as the economy recovered and more money was chasing deals, lenders loosened underwriting parameters, according to mortgage-securities data provider Trepp. Now more than half of all new commercial loans are interest-only, according to an April report by Trepp. They’re riskier because borrowers don’t pay down principal over time, increasing lender exposure in the event of a downturn.

Whether the Kushners can salvage their Times Square dreams depends on filling the property with reliable tenants. Or finding another savior to swoop in with a sweetheart offer.