A Record Rally in Chinese Dollar Bonds Falters With Warning Signals Ahead

China Credit Tracker

An unprecedented rally in Chinese developers’ junk dollar bonds is losing steam, pushing the market toward a crossroads as investor views diverge and borrowers greet banks’ deal pitching frenzy with caution.

The country’s high-yield dollar notes, dominated by those of real estate firms, lost 1.8% to 78 cents last week, a Bloomberg index shows, ending a record 13-week winning streak that was fueled by Beijing’s sweeping property rescue campaign and optimism about a reopening economy.

The earlier rebound from a record low in November helped push the stress gauge for China’s offshore credit market in January to level 2, down from 3 in December. It marked a fresh low for Bloomberg’s China Credit Tracker since data compilation began in May 2021. The tracker indicates rising levels of stress via a band of 1 to 6.

The pause to the bull run coincides with other signs of a market reaching a critical juncture, as investors debate the merits of chasing further policy-induced upside against caution arising from a persistent housing slump and default risks. Meantime, global investment banks are renewing efforts to end a yearlong drought in developers’ dollar bond sales, only to find borrowers still wary of prohibitively expensive financing costs.

“The key is whether it’s a U-shaped or L-shaped recovery. But there is no certainty in that,” said Zhi Wei Feng, senior analyst at Loomis Sayles Investments Asia Pte. “No more default and some successful cases of debt restructuring progress are key to discerning whether the policies are effective enough to support a U-shaped recovery.”

Some investors say the recent rally offers enough evidence that the worst of China’s property crisis is over. BEA Union Investment Management Ltd., which was underweight Chinese builders’ dollar debt for over a year, re-entered the sector late last year and still believes such bonds offer “the most attractive buying opportunities” in China’s credit market.

Once one of the hottest trades in the world, Chinese developers’ dollar bonds have imploded in the last two years as a government crackdown on high debt and a housing slump caused yields to surge and defaults to hit records. The turnaround has emerged since November, when Beijing stepped up efforts to salvage the ailing housing market, pushing average yields down to about 16% from a record 31%.

But to others, the recent rally was more of a reflection of better sentiment rather than material improvement in industry fundamentals.

“The sense of euphoria was caused by investors’ fear of missing out instead of rekindled interest in property bonds,” said Eddie Chia, portfolio manager at China Life Franklin Asset Management Co. “The rally could morph into volatility any time as investors shift their focus to fundamentals in the next few months.”

There are plenty of warning signals. China’s home sales continued to slump in January, even after policy makers expanded stimulus for the sector and the nation abandoned its Covid restrictions faster than expected. That prompted developers to flag the worst earnings in years.

“Homebuyers are still wary of buying houses from defaulted developers,” said Ben Bennett, head of investment strategy and research at Legal & General Investment Management Ltd. “Investors are still waiting for better clarity on how home sales and the financing plans will turn out.”

The diverging outlooks are also showing up in the primary dollar bond market, where global investment banks are renewing efforts to revive developers’ debt sales following a yearlong drought.

Driving the momentum were the two recent offerings by major conglomerate Dalian Wanda Group Co.’s property arm after a 16-month absence. Bankers are urging borrowers to seize the issuance window as much as they can. However, many developers appear reluctant and prefer to wait until yields drop further.

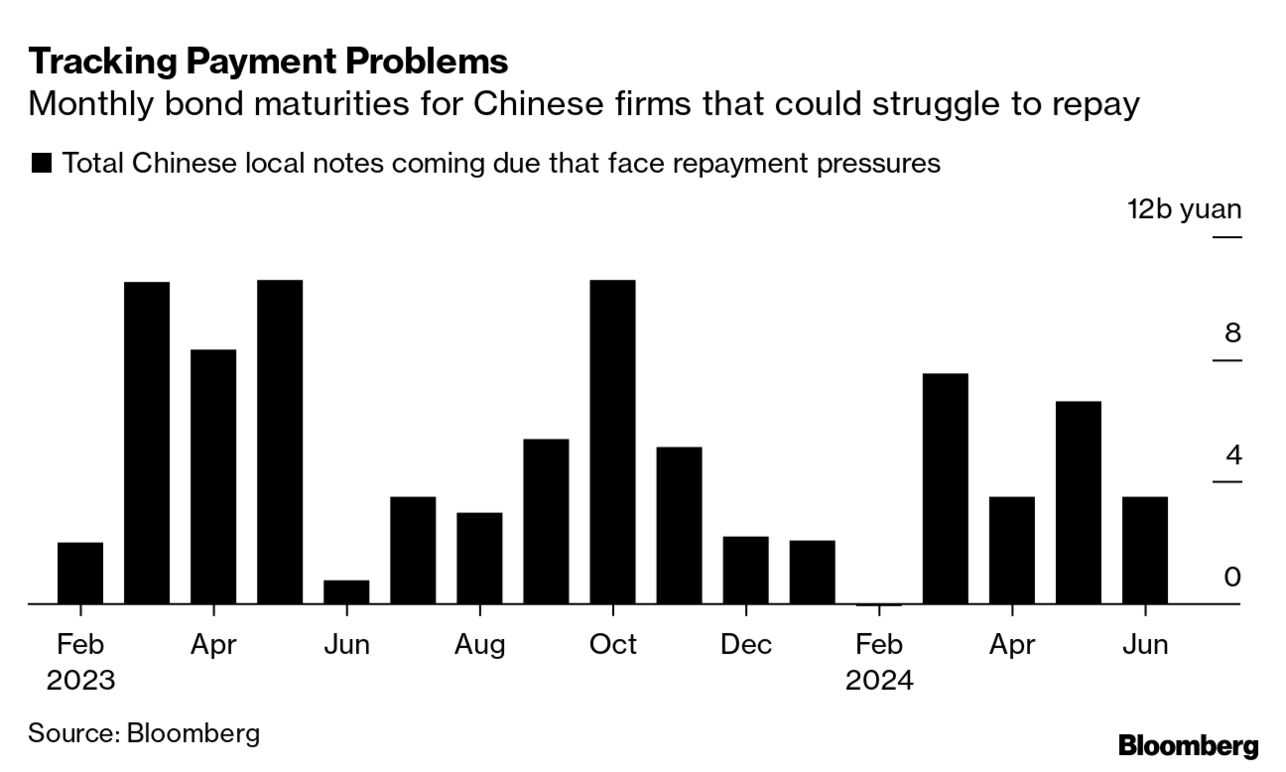

Tracking Payment Problems

Monthly bond maturities for Chinese firms that could struggle to repay

In the onshore credit market, stress eased to level 4 last month from December’s record level 6, after a reopening-induced selloff in government and high-grade corporate paper subsided.

Official defaults in the local bond market remain scarce, thanks to various types of support from easier access to funding to debt compromises with investors to preserve stability.

Provincial Default Breakdown

One issuer from Fujian and Hebei has missed a local bond payment in 2023

But beneath the surface, stress continues to manifest itself in other forms, notably the maturity extensions that distressed developers keep imposing on bondholders. Times China Holdings Ltd. became the latest such example, after a key onshore unit proposed a holistic restructuring plan for all its yuan bonds to some creditors