Methodology: How Bloomberg News Examined New York City’s Valuation of Class 2 Residential Properties

Introduction

New York’s property tax, which provides more than 40% of the city’s annual tax collections, is demonstrably inaccurate and unfair. Despite multiple attempts over several years, city and state leaders have achieved no meaningful improvements.

A review of the system for taxation of Class 2 properties, which include rental apartment buildings, condominiums and cooperatives and make up 83% of the city’s taxable residential property, shows the system’s complexity contributes to inaccuracy, which in turn shrouds its regressivity and lack of uniformity in assessments. Although condos and co-ops are private residences, state law requires assessors to value all co-op buildings—and any condo building with more than three units—as if they were income-producing properties. City officials say this requirement alone is to blame for their assessments’ well-documented problems, and the requirement does impose significant impediments to fairness and accuracy. But a Bloomberg News study reveals that city officials have compounded that problem with opaque methods and inputs that depart from market realities.

This study examines the methods used by the city’s Department of Finance to value condos and co-ops, measures the fairness and accuracy of those valuations, uncovers the implications of their inequities, and explores the root causes. The results show that the department’s own valuation decisions play a key role in driving the inaccuracies and the unfairness, producing highly regressive valuations that shift the tax burden onto those property owners who can least afford it.

The standard method for valuing income-producing properties is to divide the property’s net operating income (NOI) by a capitalization rate. In adapting this method to the valuation of condos and co-ops, city officials have opted not to rely on widely available market data, but to produce their own hypothetical values for the properties’ NOI based on data from comparable rental apartment buildings, whose owners must submit income-and-expense statements to the city each year. In these instances, our review showed, city officials routinely adjusted the comparables’ NOI values via an opaque process that they declined to describe in detail.

City officials say these adjustments to the comparables’ NOI are necessary to ensure fair comparisons. Yet our analysis of city data shows that officials use only a relatively small portion of the available rental properties as comparables: About 5,000 out of nearly 24,000 possible buildings were used to value approximately 180,000 condos and co-op properties. The resulting hypothetical NOI values used in the city’s valuations are a main driver of regressivity in the city’s Class 2 assessments, our study shows.

For the second factor in their valuation calculations, a capitalization rate, city officials again opted not to use widely available market data for New York. Instead, they say, they derive their own capitalization rate using the Ellwood Formula. That formula requires certain data points, including loan-to-value ratios, mortgage loan interest rates, equity yield and other variables that are not reflected in the city’s records. Several experts have expressed doubts that the city has the necessary data to use the formula. City officials declined to share the department’s capitalization rate method or the data underpinning it, but Bloomberg’s review shows that the city’s rate is far higher than the local market rate. Capitalization rates have an inverse relationship to market values, so our study finds that the city’s inflated capitalization rate plays a central role in producing inaccurately low assessments across the board – an outcome that masks the system’s regressivity.

In constructing a capitalization rate, the department adds in what it has called an effective tax rate to account for upcoming property taxes. The intended purpose is to balance out the amount of the previous year’s property tax, which is included in the net operating income figures the department uses. But in setting the size of the add-in, officials assume they will value properties accurately, producing an effective tax rate of 5% or more. Our study, however, reveals that the department’s actual effective tax rate is about 0.5%, or less than 1/10 of the value the city loads into its capitalization rate. This step alone greatly increases the city’s putative cap rate relative to actual market rates – contributing to inaccurately low valuations.

Methodology

Our examination consists of three studies. The first is an analysis of comparable rental properties and the net operating income data used by the department to value condos and co-ops. The second is a sales ratio study of condominiums. The third is a sales ratio study of rental apartment buildings. Each is described in more detail below.

The study period for the comparable rental properties analysis covers 2012 through 2020. The sales ratio studies cover FY 2017 through FY 2019. (Issues with the consistency and completeness of the city’s bulk property tax bill data preclude the analysis of effective tax rates for FY2012 through FY2016 and for FY2020. Sales and assessment ratio results for those periods were similar to our findings from the data covering FY2017 through FY2019.)

The data. We relied on data from New York City’s Open Data Portal as well as from the department’s website. Often, the same data set appears on both sites, and, in some cases, there are slight variations. In such cases, Bloomberg conducted extensive analyses of both versions before deciding which to use. Whenever possible, we relied on data from the Open Data Portal.

Here is a list of the data sets used in our analyses:

* Property Tax Assessment Roll Data, FY2012-FY2020

* Detailed Annual Sales Reports by Borough, FY2012-FY2020

* Automated City Register Information System (ACRIS) data, FY2012-FY2020

* Tax bill data from Open Balance Summary, FY2017-FY2019

* DOF Condominium Comparable Rental Income, FY2013-FY2020

* DOF Cooperative Comparable Rental Income, FY2013-FY2020

Rental comparables analysis

We examined the degree to which the Department of Finance (DOF) alters the net operating income of comparable properties to arrive at its estimated values. Our analysis found that in any given year, the department derived as many as 100 different net operating incomes from the same comparable rental building. Differences among these values averaged as much as 130% in any given year.

We also calculated the department’s capitalization rates by using its estimated values and the derived net operating incomes that were provided in the city’s data. Our analysis then compares the department’s cap rates with market rates compiled by Real Capital Analytics, a real estate data provider. The results show that the rates used by the department are roughly three times higher. These higher rates drive down the department’s estimated property values by about 70%.

Manhattan Cap Rates

Note on property IDs. The study evaluates condos and co-ops separately because the city identifies the buildings differently. Every co-op building is taxed as one entity, so there is one borough-block-lot number, the unique parcel ID, for each building. Each unit in a condo building, on the other hand, is taxed separately, requiring a different identification method. We use the first six digits of the 10-digit borough-block-lot-number and the unique condo number assigned to each building to match the buildings to assessment records. Then we add the department’s values by aggregating the value for all the units in a condo building.

The city comparable rental data is arranged so that there is one record for each condo or co-op building valued, with corresponding fields added at the end for as many as three comparable rental buildings used to value each property. In order to examine the comparables, our analysis rearranges the data so that each building for every tax year gets its own row, regardless of whether it’s a comparable or the building being valued. Identifiers are added so that the buildings can be distinguished and, if they are comps, traced back to the building being valued.

Sales ratio studies

Both of our sales ratio studies, for condos and for rental sales, rely on the same methods, which are taken from the International Association of Assessing Officers (IAAO) standards. The studies compare arm’s-length sales to the department’s estimations of fair market values as well as assessed values and property tax bills.

The sales data is filtered to capture condominiums and rental properties using the city’s tax class and building class codes. (Note: It’s not practical to conduct a sales ratio study on co-op buildings because they’re valued and taxed as single parcels but sold as individual units through shares in a cooperative. Nonetheless, because the department values co-ops using the same methods as condos, it’s reasonable to conclude that outcomes would be similar.)

Although the department provides the sales data on its website, sales used in the study were also checked against ACRIS, New York’s system used to compile deeds, mortgages and other property records, to ensure they were arm’s-length transactions and that they did not include multiple parcels or bulk sales. The study also uses IAAO methods to trim outliers, meaning ratios that fall far from the median ratio – in this case, ratios over or under 1.5 times the interquartile range (IQR). Sales under $10,000 were also thrown out to ensure we eliminated transactions that were not conducted at arm’s length.

Valid sales were then matched with assessment roll data using the borough-block-lot numbers if the sale dates fell within the fiscal year for which the valuations were used to calculate property taxes. Simple ratios of the estimated market values to actual market sales were then calculated.

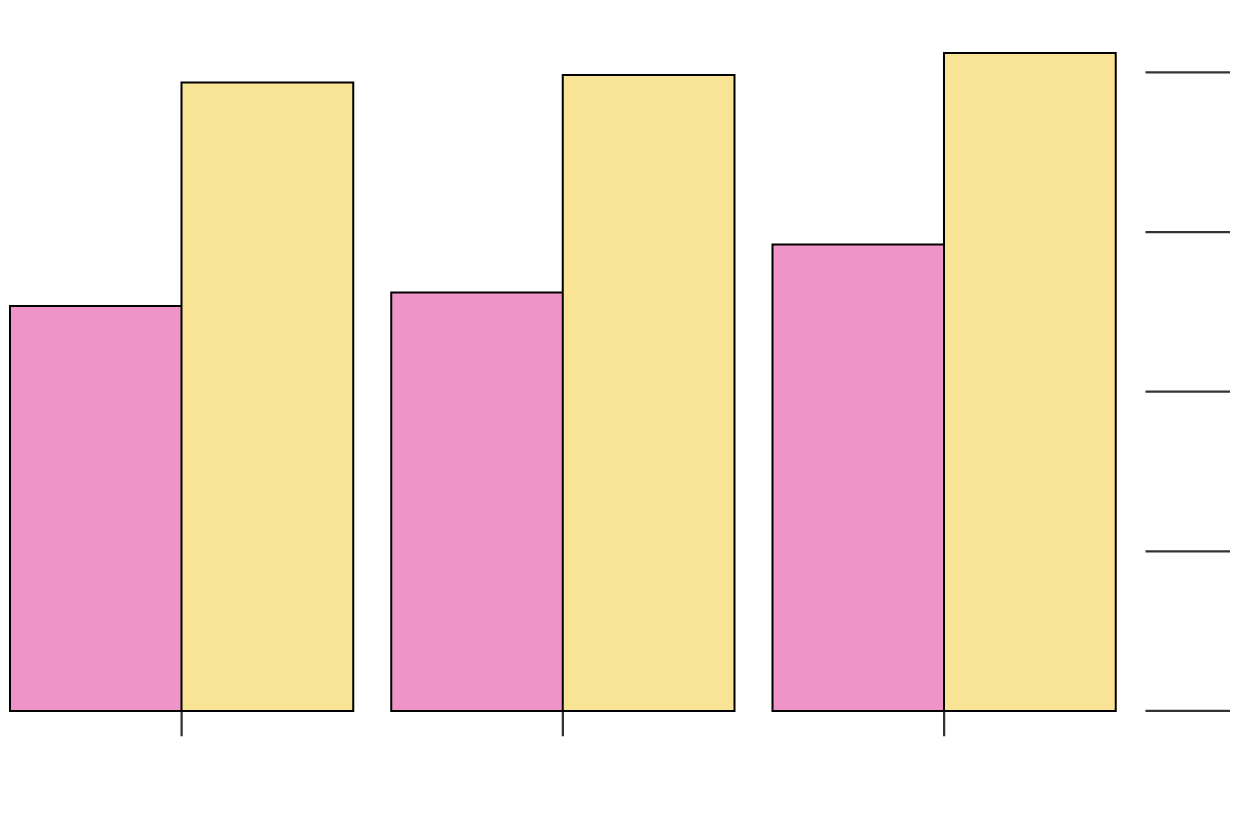

In sales ratio studies, a ratio of 1 means the assessment office perfectly estimated the property’s fair market value. Any ratio over 1 means the office overestimated the market value, while those under 1 indicate that values were underestimated. Our analysis for condo properties shows that even before assessment limits mandated by state law are applied, the department grossly undervalues them relative to their market values, capturing less than 20% of actual sales prices on average from 2017 through 2019.

NYC Class 2 Condos - Grossly Undervalued

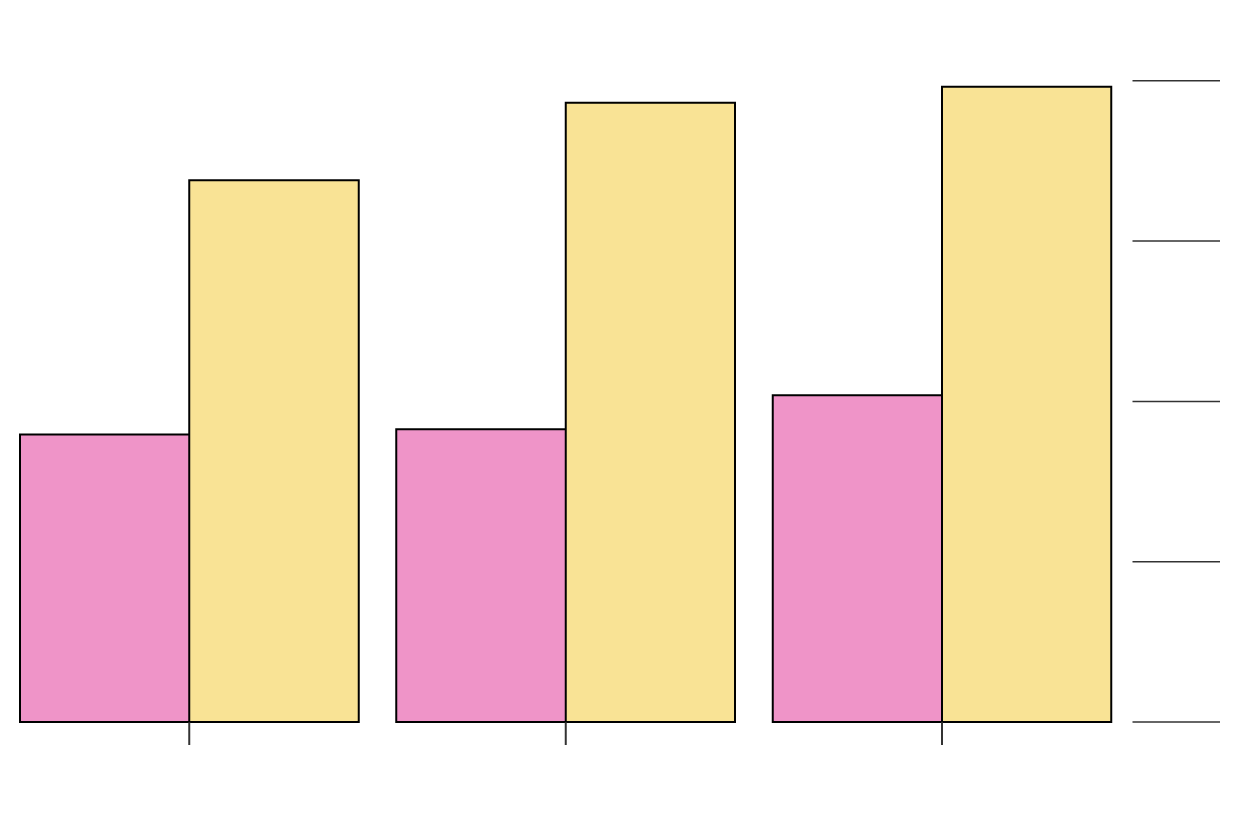

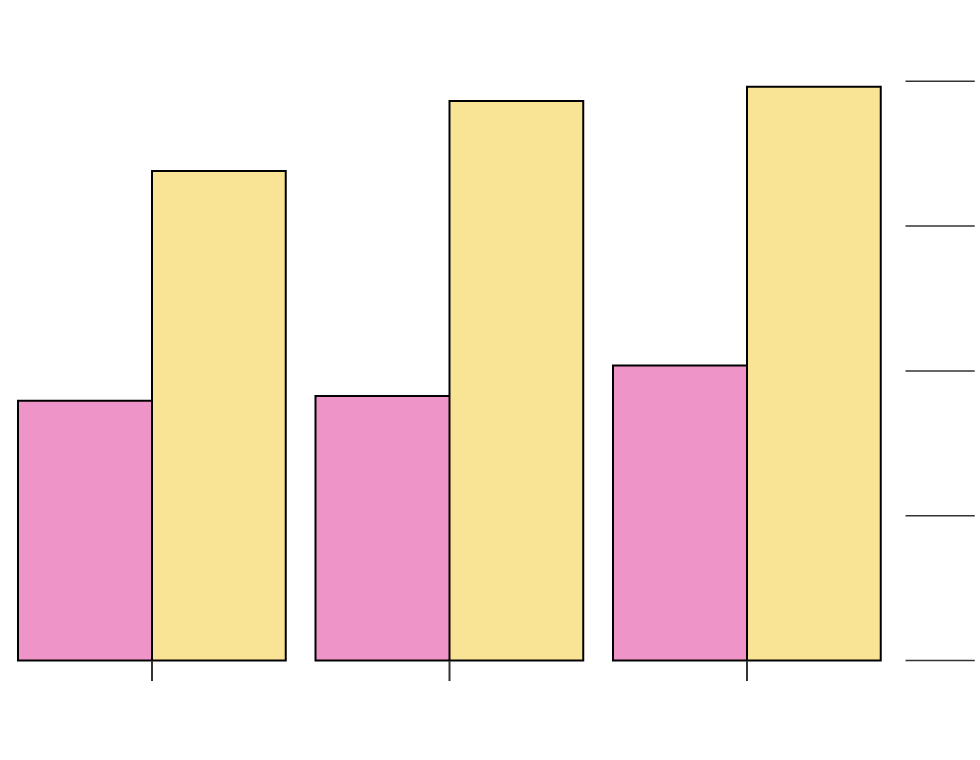

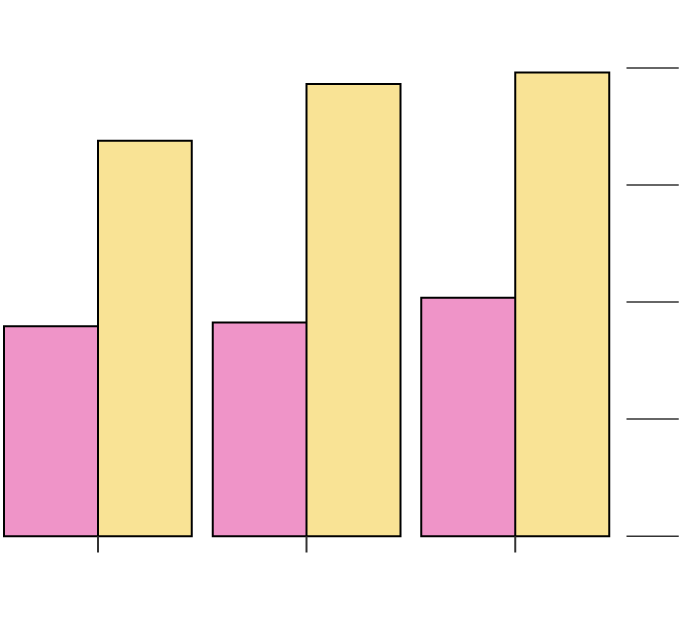

Our analysis for rental buildings shows that the department captures roughly 50% more of their actual sale prices than it does for condos. This means rentals shoulder a greater share of the property tax burden than do condos and co-ops, although they should be treated the same.

Larger % of value captured for rentals

- Condos

- Rentals

Market Value

40%

39.63%

38.63%

33.80%

30%

20%

20.38%

18.27%

17.95%

10%

0

2017

2018

2019

Fiscal Year

Market Value

40%

39.63%

38.63%

33.80%

30%

20%

20.38%

18.27%

17.95%

10%

0

2017

2018

2019

Fiscal Year

Market Value

40%

39.63%

38.63%

33.80%

30%

20%

20.38%

18.27%

17.95%

10%

0

2017

2018

2019

Fiscal Year

Once the ratios were calculated, we ran tests recommended by the IAAO on them to determine the assessments’ fairness and accuracy.

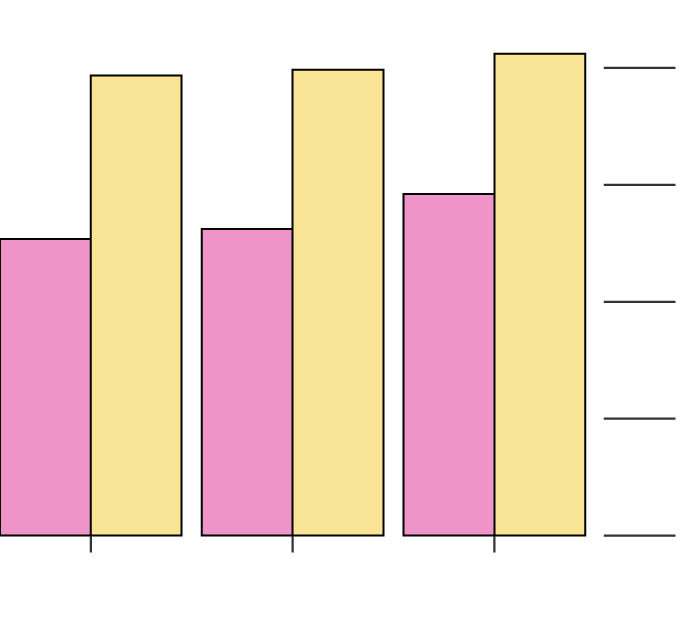

Uniformity

We tested assessments’ uniformity – that is, whether they treated all properties in Class 2 the same – by measuring the ratios’ distribution relative to the median. The resulting score, called the coefficient of dispersion, or COD, approximates the average percentage error. The IAAO’s standards for both residential and income-producing properties in large urban areas calls for COD to be from 5 to 15.

Our analysis found that in each year of our study, the COD for condo evaluations exceeded 30, indicating a pronounced lack of uniformity.

Lack of Uniformity

Regressivity

We also tested the assessments for regressivity, or the degree to which higher-priced properties were undervalued and lower-priced properties were overvalued, by measuring how our sales ratios changed relative to price. IAAO standards call for the resulting values, called price-related differentials, or PRDs, to be from 0.98 to 1.03. Any number above 1.03 indicates an undervaluation of higher-priced properties and an overvaluation of lower-priced properties.

Our analysis found that PRDs for condo valuations exceeded the standard considerably in each year of the study, indicating deep regressivity.

Deeply Regressive

Binned scatter plots. Our analysis visualizes this regressivity using binned scatter plots, which is a method used to analyze large data sets. Binned scatter plots divide data into an equal number of bins based on some variable—in our case, 10 bins based on price—and then computes average ratios for each bin. Lines sloping from the upper left to lower right indicate regressivity.

NYC Class 2 Condos - Binned sales ratios

Of note: Among rental properties, we found that valuations are also regressive. Because rental properties as a whole shoulder a larger property-tax burden than condos and co-ops, this finding suggests that lower-priced rental buildings receive a disproportionate share of that burden. The regressivity is illustrated in this binned scatter plot.

NYC Class 2 Rentals - Binned sales ratios

The study also calculates several other measures of central tendency, including means (or averages) and weighted means. All of these measures were calculated by year and by borough.

Effective tax rate

The analysis uses actual tax bill data to examine the end result for taxpayers: the effective tax rate. The ETR is simply the final tax bill divided by the market value of the property – in this case, the sale price. This part of our study reflects the impact of exemptions as well as abatements. Unlike exemptions, which lower properties’ assessed values, abatements directly reduce final tax bills. We produced the same statistics for the effective tax rate analysis as for those covering valuations and assessments.

The Manhattan effect. When effective tax rates are viewed from a citywide perspective, the effects of exemptions and abatements might appear to eliminate regressivity in the city’s valuations. In fact, closer examination reveals that this effect can be attributed in large part to distortions that result from the inclusion of Manhattan, which has significantly more valuable real estate than the other boroughs and does not benefit as much from abatement programs for new condo construction. Manhattan’s much higher market values, coupled with the fewer lucrative abatements, cause the effective tax rate in Manhattan to be higher than in most other boroughs.

This Manhattan effect skews citywide results in a way that masks deep disparities that emerge when viewed on a borough-by-borough basis – including within Manhattan itself – and even after the extensive assessment limits, exemptions and abatements are applied. The same pattern is seen in a citywide analysis when Manhattan is excluded.

Our analysis found deep inequities in effective tax rates among the boroughs. Among New York condo owners, those in Brooklyn benefit the most, paying the lowest effective tax rate.

Table: NYC Class 2 Condos - Effective tax rate stats

Weighted

mean

effective

tax rate

Median

effective

tax rate

Borough

Sales

COD

PRD

Manhattan

Brooklyn

Queens

Bronx

Staten Island

Citywide

13,667

6,123

3,436

959

540

24,725

0.7627%

0.0749%

0.2385%

0.2398%

0.6691%

0.5350%

0.602%

0.202%

0.300%

0.337%

0.580%

0.530%

41.23

267.90

123.05

84.50

34.75

68.50

1.24

1.15

1.26

0.92

1.18

1.04

Weighted

mean

effective

tax rate

Median

effective

tax rate

Borough

Sales

COD

PRD

Manhattan

Brooklyn

Queens

Bronx

Staten Island

Citywide

13,667

6,123

3,436

959

540

24,725

0.7627%

0.0749%

0.2385%

0.2398%

0.6691%

0.5350%

0.602%

0.202%

0.300%

0.337%

0.580%

0.530%

41.23

267.90

123.05

84.50

34.75

68.50

1.24

1.15

1.26

0.92

1.18

1.04

Weighted

mean

effective

tax rate

Median

effective

tax rate

Borough

Sales

COD

PRD

Manhattan

Brooklyn

Queens

Bronx

Staten Island

Citywide

13,667

6,123

3,436

959

540

24,725

0.7627%

0.0749%

0.2385%

0.2398%

0.6691%

0.5350%

0.602%

0.202%

0.300%

0.337%

0.580%

0.530%

41.23

267.90

123.05

84.50

34.75

68.50

1.24

1.15

1.26

0.92

1.18

1.04

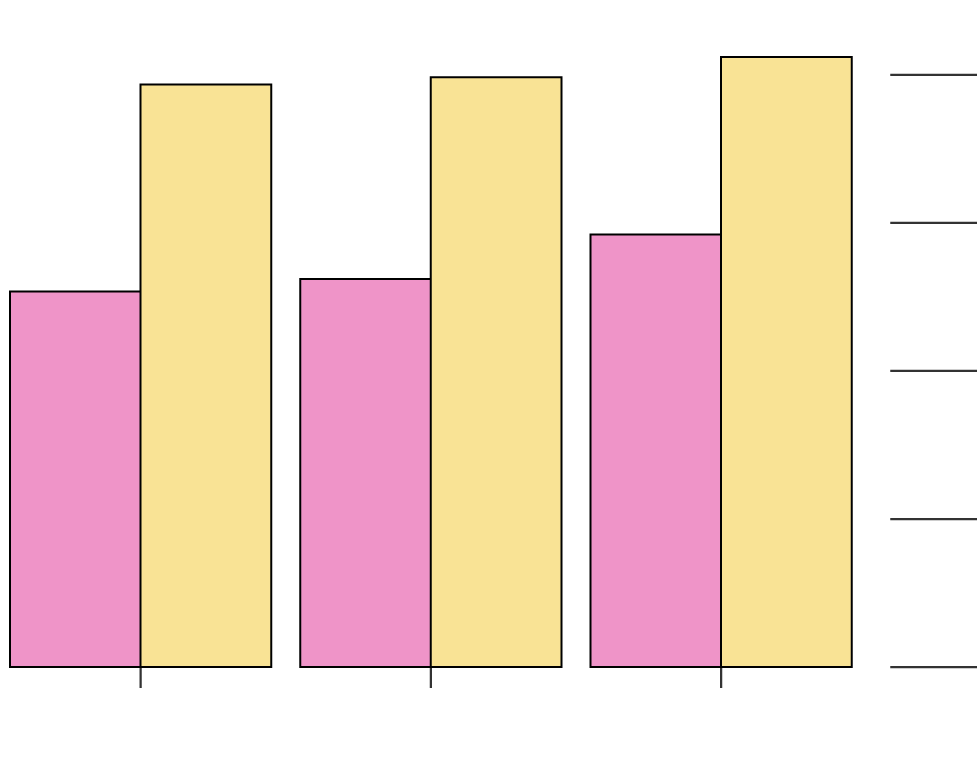

Rental properties pay a larger effective tax rate, especially in Brooklyn. Because the city captures more value for rental properties, they end up shouldering a disproportionate share of the tax burden allotted to Class 2 properties.

This pattern is especially pronounced in Brooklyn. Using tax bill data, we can calculate a rough estimate of the amount of taxes that are shifted from condos to rental properties in Brooklyn. By aggregating the total amount of taxes collected for each type of property (condo and rental), we can see the actual distribution of the tax burden.

We can then estimate the total value of each property type by dividing the taxes collected by the effective tax rates derived from our sales ratio studies—0.075% for condos and 0.627% for rentals in Brooklyn.

Once we have the total taxes collected and the total value of the properties, we arrive at an equalized effective tax rate by dividing the total taxes collected by the total value of the property. Applying the equalized effective tax rate to the total property value gives us an estimate of what the tax would have been if the property types were taxed at the same effective rate.

Taking the difference between the actual tax collected and the amount that would have come in under a flat effective rate shows a roughly $237 million shift in the tax burden from Brooklyn condos to Brooklyn rental properties in 2019 alone. Because co-ops are valued using the same methods as condos, it’s reasonable to assume there is a similar tax shift from co-ops to rentals. If so, approximately $422 million would have shifted from co-ops to rental properties in 2019.

Rentals pay a larger effective tax rate

- Condos

- Rentals

Effective Tax Rate

0.8%

0.8241%

0.7968%

0.7872%

0.6%

0.5844%

0.5243%

0.5073%

0.4%

0.2%

0

2017

2018

2019

Fiscal Year

Effective Tax Rate

0.8%

0.8241%

0.7968%

0.7872%

0.6%

0.5844%

0.5243%

0.5073%

0.4%

0.2%

0

2017

2018

2019

Fiscal Year

Effective Tax Rate

0.8%

0.824%

0.797%

0.787%

0.6%

0.584%

0.524%

0.507%

0.4%

0.2%

0

2017

2018

2019

Fiscal Year

Net Operating Income Adjustments and Regressivity

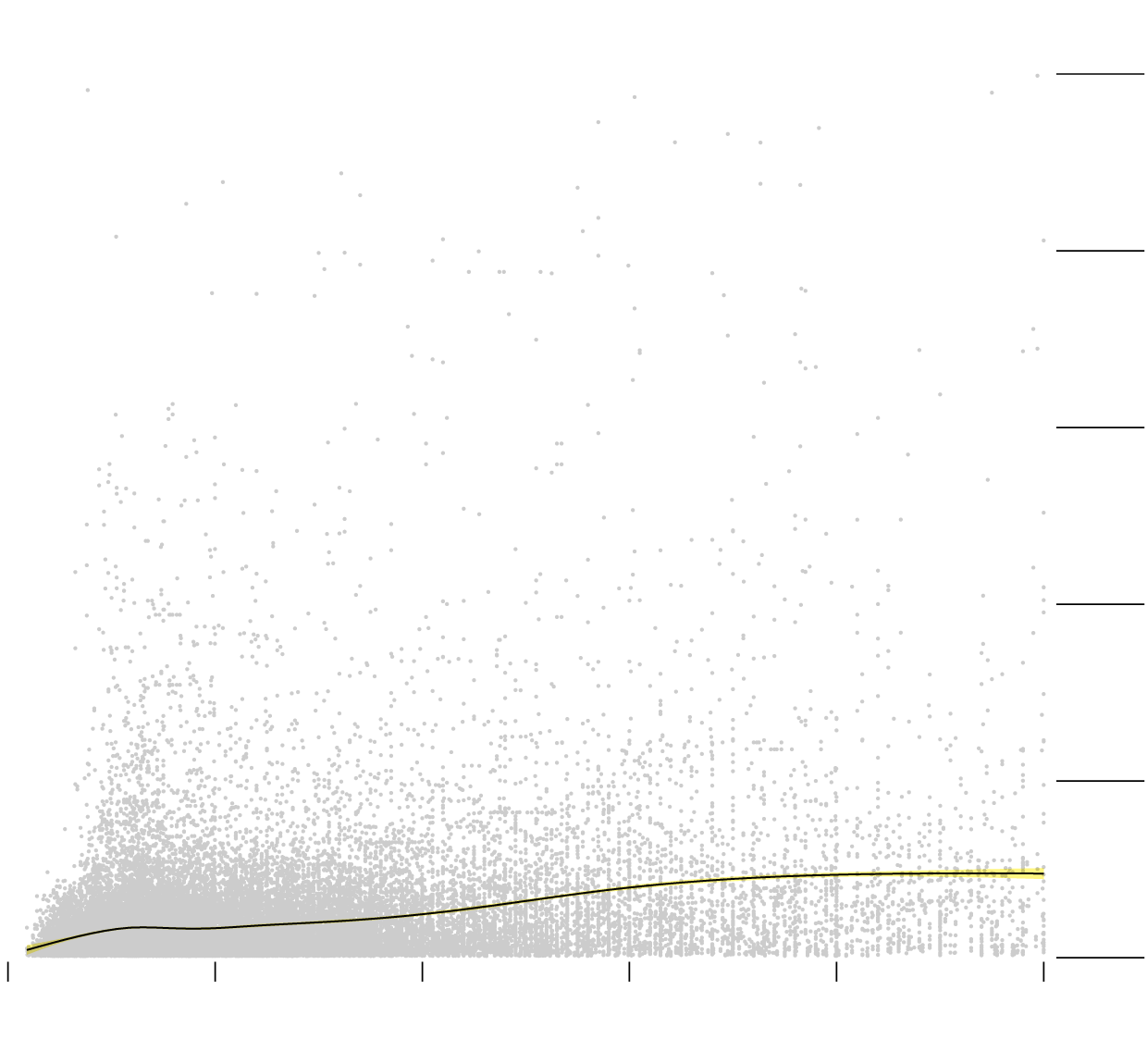

By comparing changes that city officials made to the net operating income of comparable rentals to actual condo sales, it’s possible to examine whether the department’s decisions and methods are driving regressivity in its condo valuations.

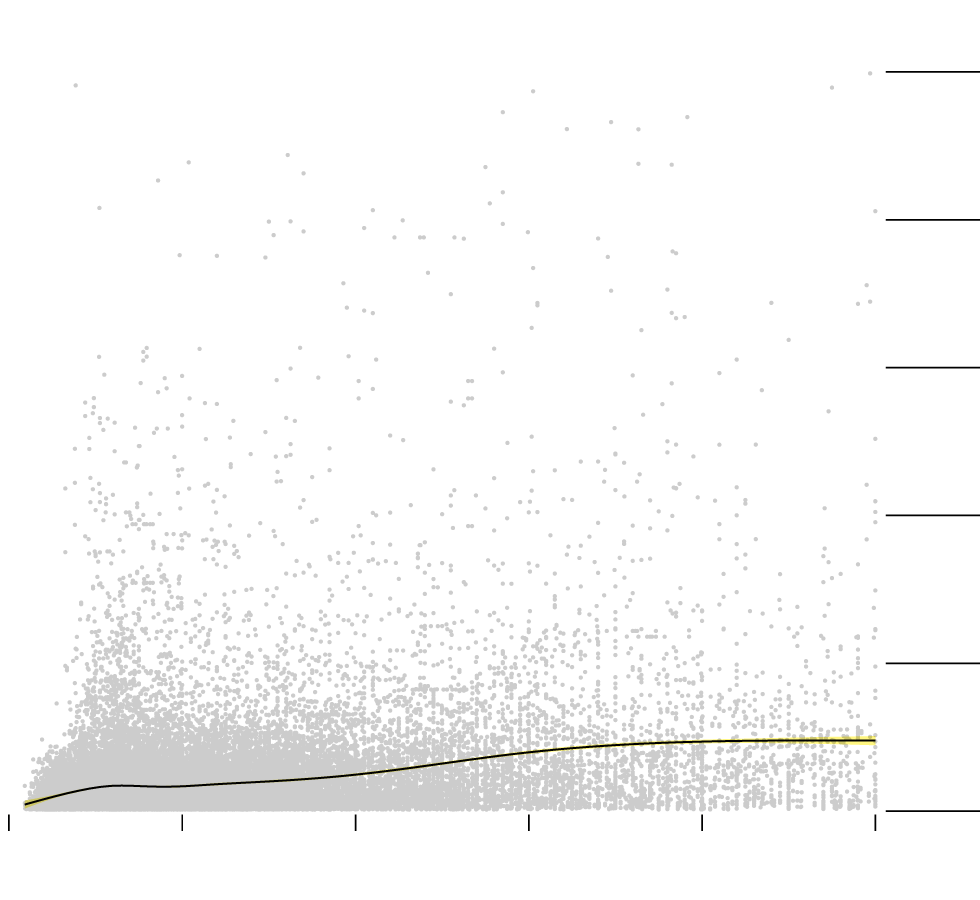

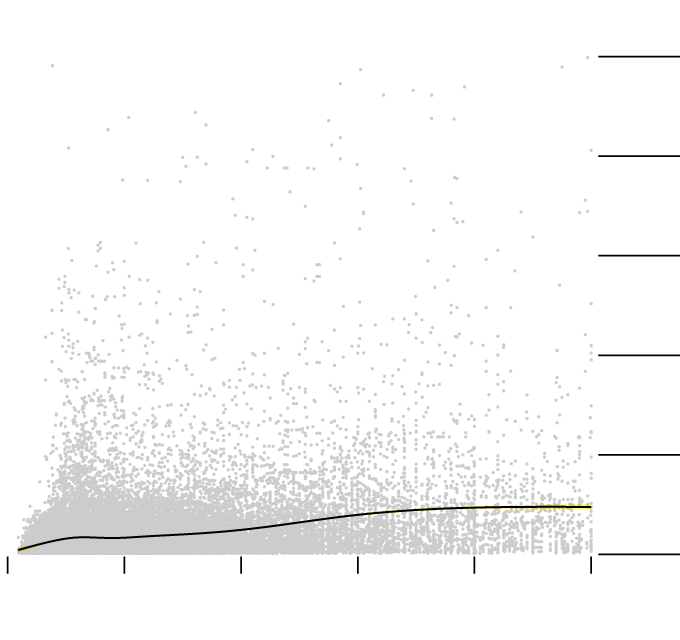

Bloomberg joined valid, arms-length condo unit sales to assessment records as well as data on the comparable rental properties used to impute the net operating income for the buildings in which the condo units are located. Because condo apartments sell as individual units while the net operating income of the comparable rental properties was computed for entire buildings, we used each condo unit’s common interest percentage in its building to apportion the total net operating income among individual units. (The common interest percentage is included in the city’s assessment roll data for condo units.) In all, our data set for this analysis includes about 15,000 condo unit sales and roughly 43,000 comparable rental properties.

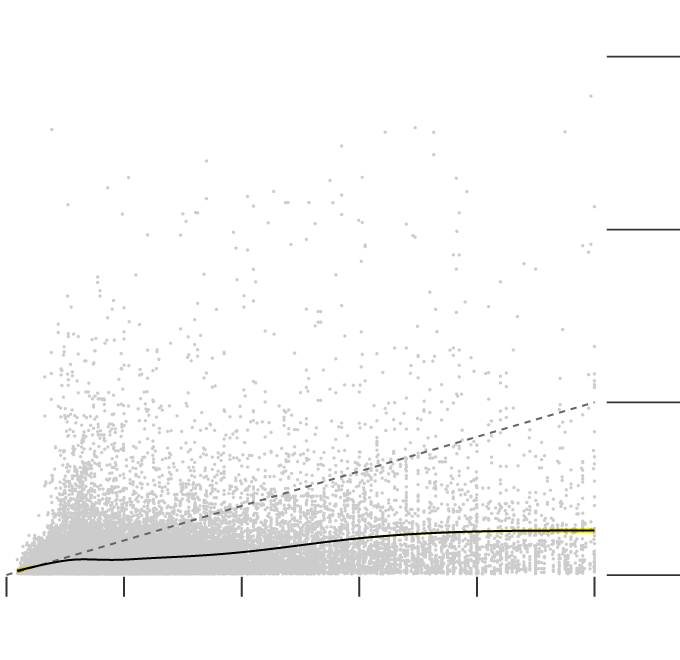

Once we have a sale price and a net operating income figure for each unit, we plot them on a graph with each dot representing a sale and a comparable for that sale. The x-axis reflects the unit’s sale price. The y-axis shows the net operating income of the comparables used to value the condo unit, as apportioned according to the unit’s common interest percentage.

If the department’s estimates for net operating income were accurate, the graph would reflect a linear relationship between them and the sale prices. That is, as the sale prices increase, so should the net operating income estimates.

Our results, depicted below, show that the relation is not linear. Instead, as sale prices increase, there is little change in the average net operating income used to value the condos. This is reflected in the blue trend line.

Pooled comparable analysis

DOF imputed NOI for unit

$500k

400

300

200

100

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

DOF imputed NOI for unit

$500k

400

300

200

100

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

DOF imputed NOI for unit

$500k

400

300

200

100

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

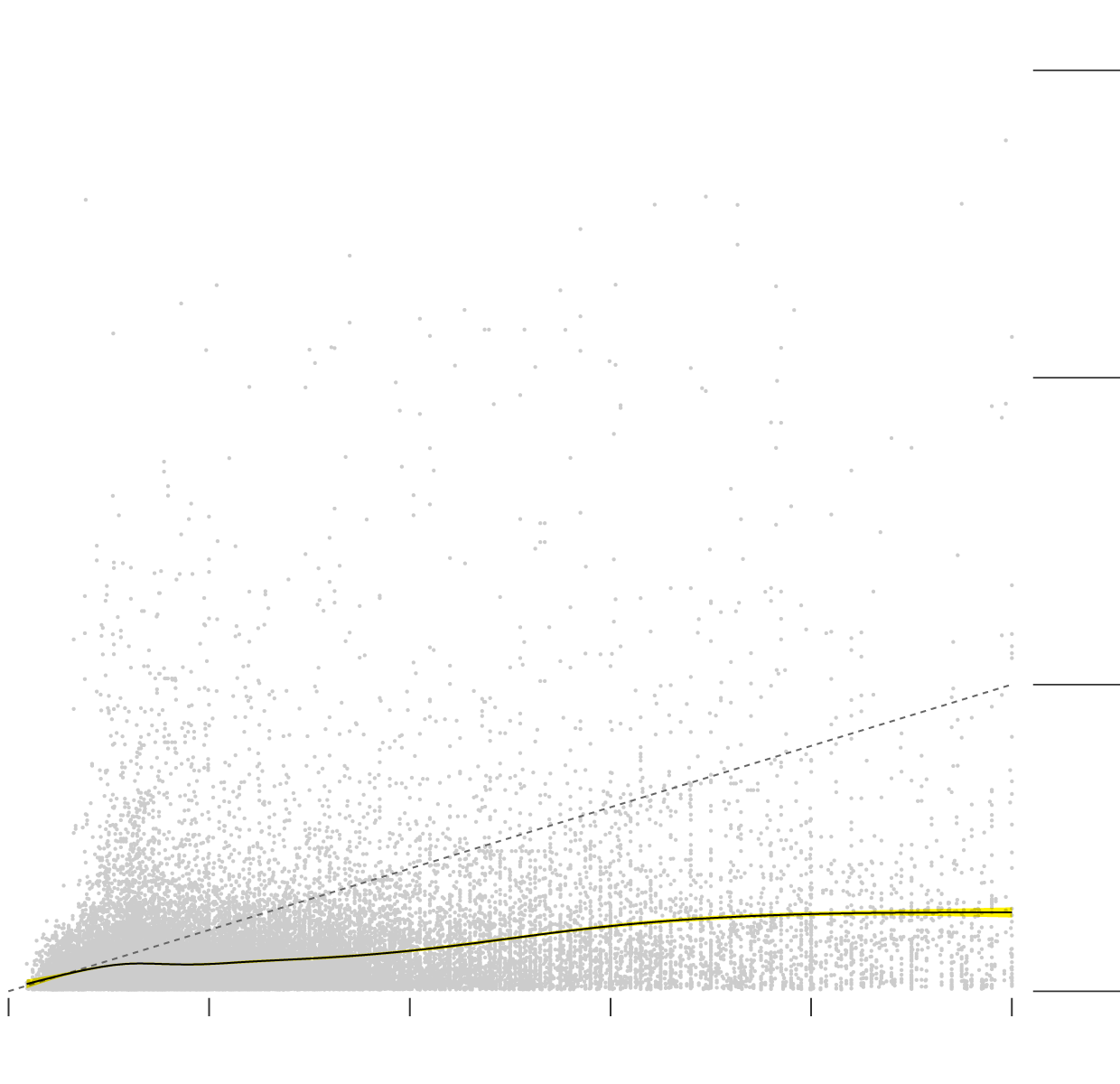

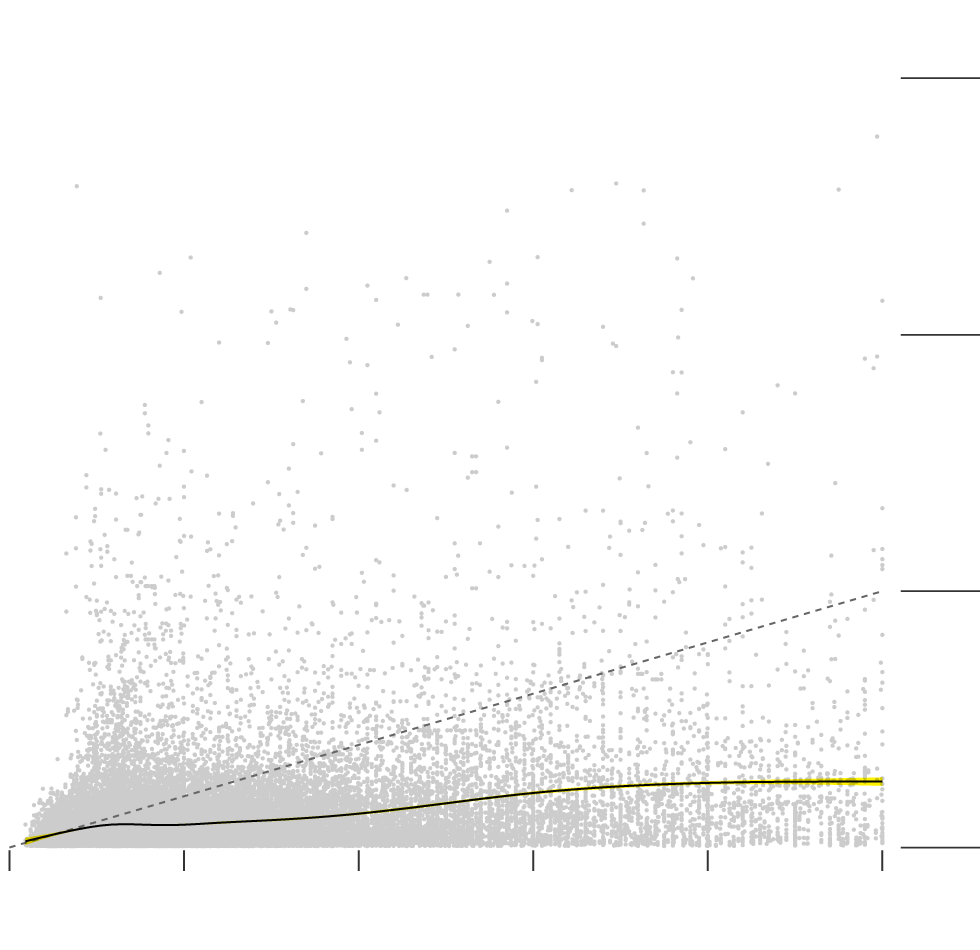

We then applied market capitalization rates published by Real Capital Analytics to the department’s estimated NOI values to determine the units’ implied market values. This step was designed to focus on the estimated NOI’s effect on the department’s valuations. By dividing the net operating income by the cap rate, we get the market value implied by the department’s net operating income figures. We can then add a trend line that shows how well those values match actual sale prices. Any point below the black, 45-degree trend line would be undervalued while those above it would be overvalued using the department’s net operating income figures.

Implied value based on DOF NOI, market cap rates

DOF implied sale price

$15m

10

5

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

DOF implied sale price

$15m

10

5

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

DOF implied sale price

$15m

10

5

0

0

$1m

$2m

$3m

$4m

$5m

Sale price

Here we see that as the sale price increases, more dots fall below the black line, indicating that the department’s estimates of net operating incomes contribute to the system’s high degree of regressivity.

Conclusion

The state law that requires the department to value condos and co-ops as if they generated income presents a difficult challenge for the department and diverges from international assessment standards for residential properties. Nonetheless, our analysis shows that city officials’ own methods and decisions—including opting to develop their own estimates of capitalization rates and hypothetical net operating incomes—contribute to inaccuracies and regressivity in their assessments. Moreover, our analysis suggests that the city’s practices result in low-value rental properties bearing an outsize share of the city’s property tax burden.