Rating:

BB

BBB

A

AA

AAA

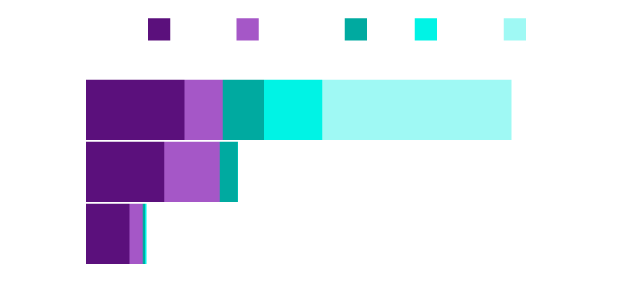

$933B

2007

$333B

2019

$132B

2021

A Hidden Bond-Market Problem

American savers could once count on bonds to provide meaningful returns with modest risk. Not anymore.

More than a decade of easy money has kept the U.S. economy afloat in times of crisis and fueled an unprecedented boom in financial markets.

But it’s also created a whole new series of risks, especially for savers.

Where there was once a vast pool of safe debt in which they could park their cash and count on annual payouts of 5% or more—comfortably above inflation—today there’s little more than a puddle, and a shrinking one at that. In fact, never has the amount of new government and corporate debt paying even modest yields been so minuscule.

$932.6B

580 parent issuers

Rating:

BB

BBB

A

AA

AAA

$84.0B

Federal National Mortgage Association

(Fannie Mae)

$179.4B

Federal Home Loan Banks

$85.2B

Federal Home Loan Mortgage Corp

(Freddie Mac)

$932.6B

580 parent issuers

Rating:

BB

BBB

A

AA

AAA

$84.0B

Federal National Mortgage

Association

(Fannie Mae)

$179.4B

Federal Home Loan Banks

$85.2B

Federal Home Loan Mortgage Corp

(Freddie Mac)

$932.6B

580 parent issuers

Rating:

BB

BBB

A

AA

AAA

$85.2B

Federal Home Loan Mortgage Corp

(Freddie Mac)

$84.0B

Federal National Mortgage

Association

(Fannie Mae)

$179.4B

Federal Home Loan Banks

$932.6B

580 parent issuers

Rating:

BB

BBB

A

AA

AAA

$84.0B

Federal National Mortgage Association

(Fannie Mae)

$179.4B

Federal Home Loan Banks

$85.2B

Federal Home Loan Mortgage Corp

(Freddie Mac)

$932.6B

580 parent issuers

Rating:

BB

BBB

A

AA

AAA

$84.0B

Federal National Mortgage Association

(Fannie Mae)

$179.4B

Federal Home Loan Banks

$85.2B

Federal Home Loan Mortgage Corp

(Freddie Mac)

$333.0B

301 parent issuers

$7.5B

Altice USA Inc

▼

$11.7B

◀ The Walt Disney Company

$333.0B

301 parent issuers

$7.5B

Altice USA Inc

▼

$11.7B

◀ The Walt Disney Company

$333.0B

301 parent issuers

▲

$7.5B

Altice USA Inc

▲

$11.7B

The Walt Disney Company

$333.0B

301 parent issuers

▲

$7.5B

Altice USA Inc

▲

$11.7B

The Walt

Disney Company

$333.0B

301 parent issuers

▲

$7.5B

Altice USA Inc

▲

$11.7B

The Walt

Disney Company

$131.7B

138 parent issuers

$23.9B

Petroleos Mexicanos

$131.7B

138 parent issuers

$23.9B

Petroleos Mexicanos

$131.7B

138 parent issuers

▲

$23.9B

Petroleos Mexicanos

$131.7B

138 parent issuers

$23.9B

Petroleos Mexicanos

$131.7B

138 parent issuers

▲

$23.9B

Petroleos Mexicanos

The repercussions—for pension managers, endowments, insurance companies and 70 million baby boomers starting their retirements—are vast. Sure, yields aren’t negative like in much of Europe, but many are nonetheless being forced to, as legendary investor Warren Buffett recently put it, “juice the pathetic returns now available by shifting their purchases to obligations backed by shaky borrowers.”

Others may choose to heed the advice of Ray Dalio, the founder of hedge fund giant Bridgewater Associates, who now recommends avoiding the U.S. bond market entirely and focusing on higher-returning, non-debt investments.

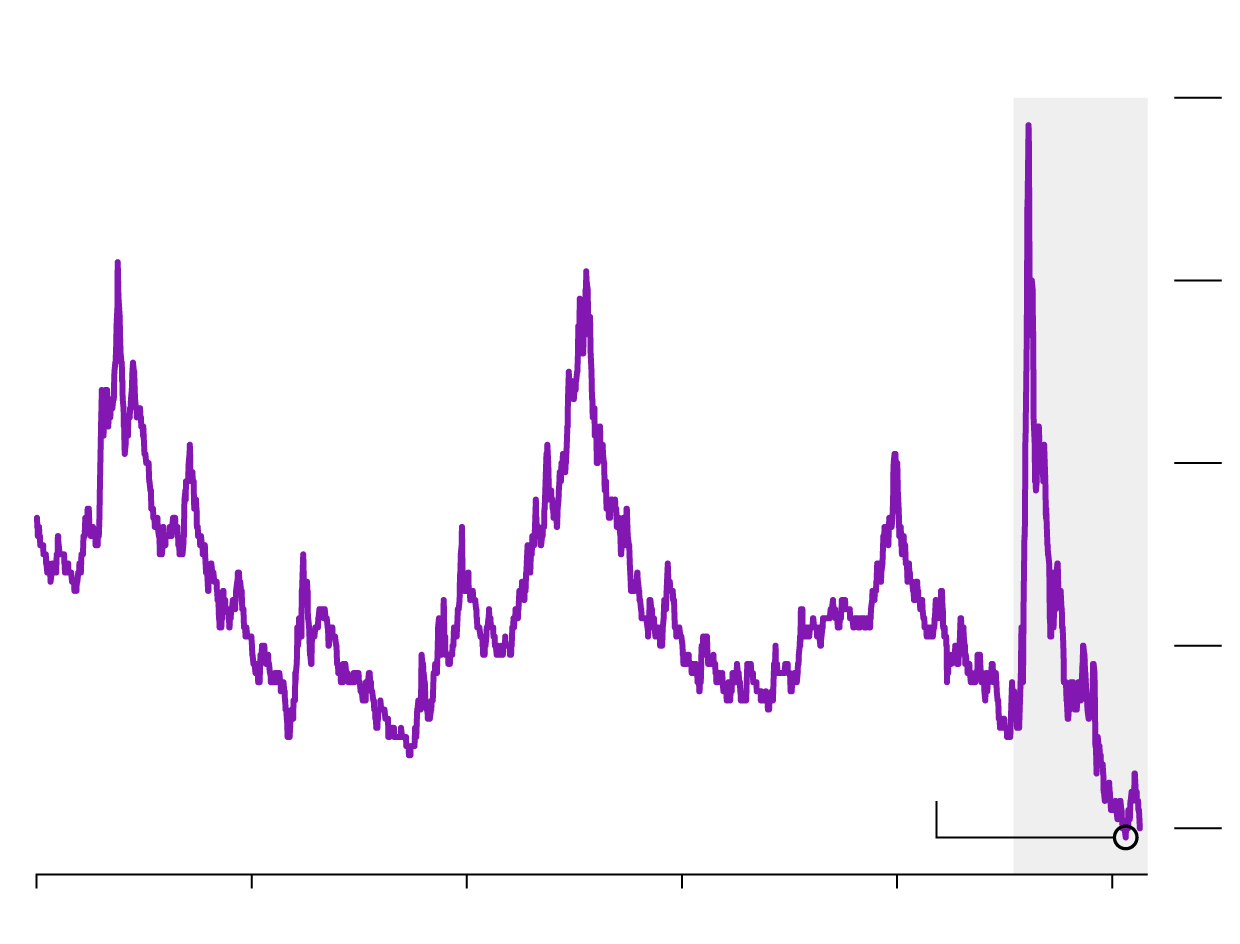

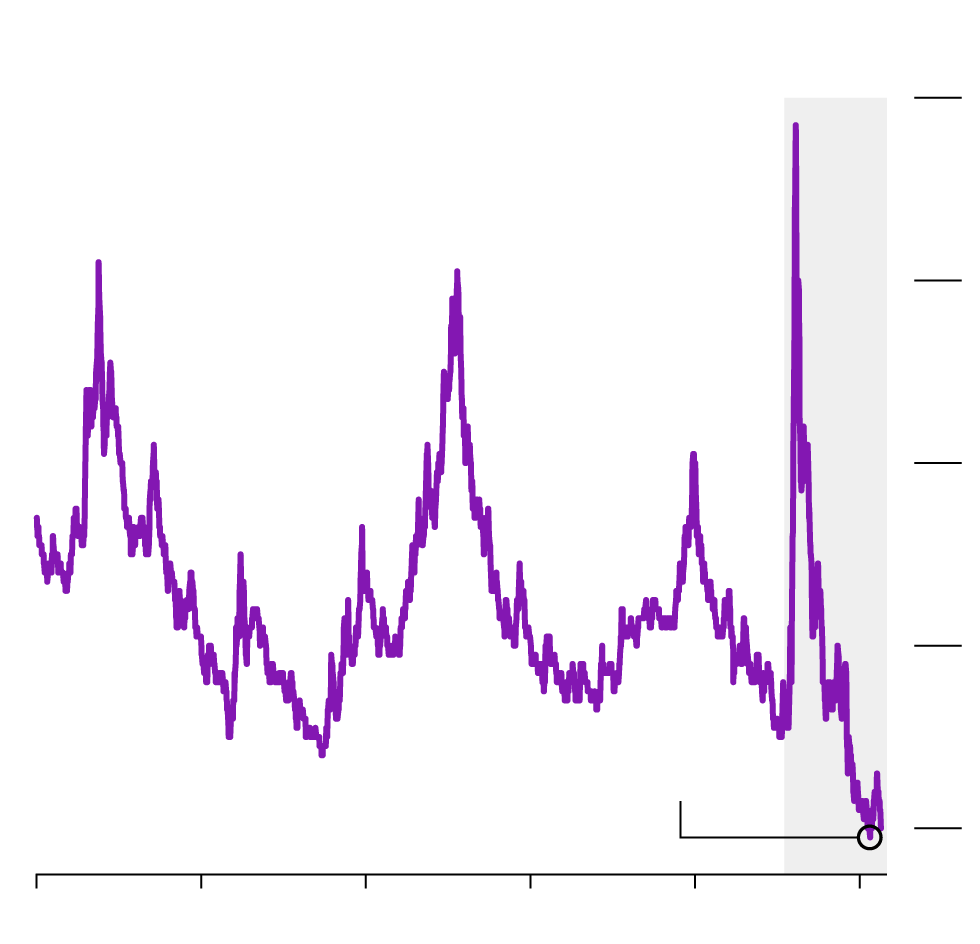

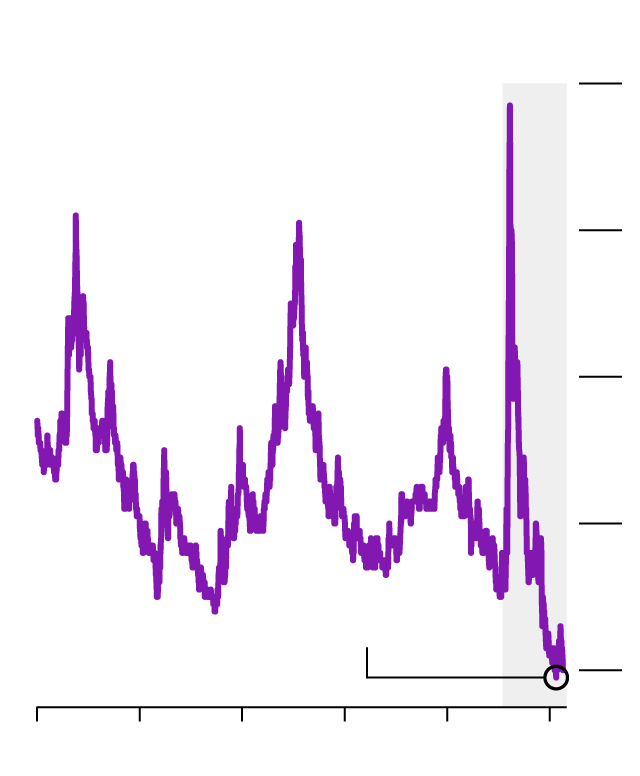

Junk’s Rock-Bottom Rates

Average yield

12%

Covid-19

Recession

▶

10

8

6

3.89%

4

2011

2013

2015

2017

2019

2021

Average yield

12%

Covid-19

Recession

▶

10

8

6

3.89%

4

2011

2013

2015

2017

2019

2021

Average yield

12%

Covid-19

Recession

▶

10

8

6

3.89%

4

2011

2013

2015

2017

2019

2021

While the potential payout is greater, such moves also carry significant risk, especially for groups previously accustomed to holding only the safest assets.

It’s possible that as savers push deeper into lower-rated debt, equities and more esoteric markets, the reckoning never comes.

But most know that’s ultimately unlikely.

“It’s a struggle that all of the public pension plans have been facing for a number of years—there are some solutions, and there are some hope and pray trades,” said Steve Willer, who helps manage $21 billion as deputy chief investment officer at the Kentucky Public Pensions Authority, which has lowered certain return targets amid the changing investment environment. “People are having to be more creative in looking at different segments of the debt market. That comes with different risks.”