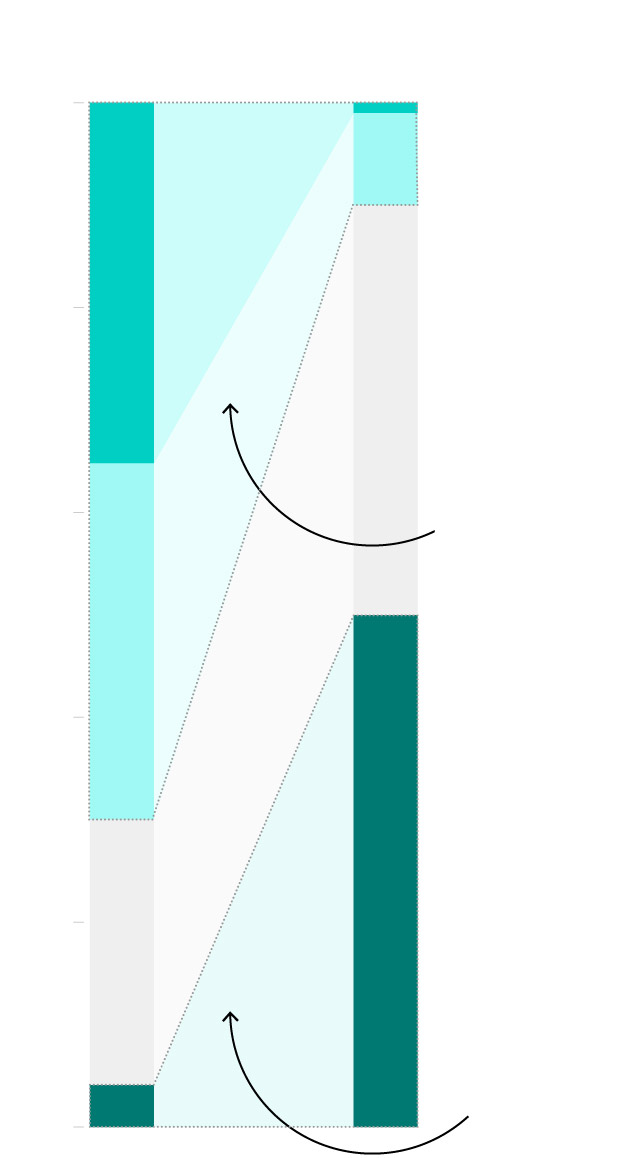

A $9 Trillion Binge Turns Central Banks Into the Market’s Biggest Whales

Central banks’ record spending blitz and what it means

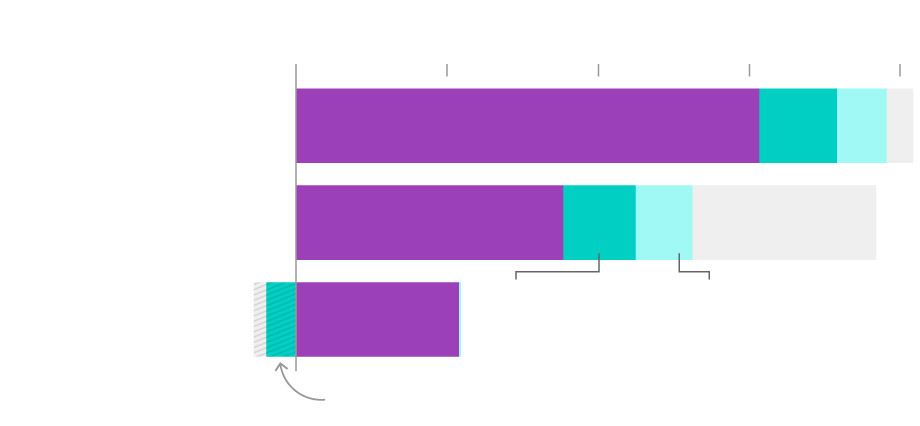

Since the start of the pandemic, central banks in the U.S., Europe and Japan have been on a $9 trillion spending spree.

That binge has turned the U.S. Federal Reserve, the European Central Bank and the Bank of Japan into the ultimate market whales, swelling their combined assets to $24 trillion. Now, talk is shifting to winding down the banks’ massive monetary stimulus and the challenge that presents for the economies they support.

Take a look at just how large that asset pool is:

Here’s how it compares to the market capitalization of some of the biggest companies.

That binge has turned the U.S. Federal Reserve, the European Central Bank and the Bank of Japan into the ultimate market whales, swelling their combined assets to $24 trillion.

Now, talk is shifting to winding down the banks’ massive monetary stimulus and the challenge that presents for the economies they support.

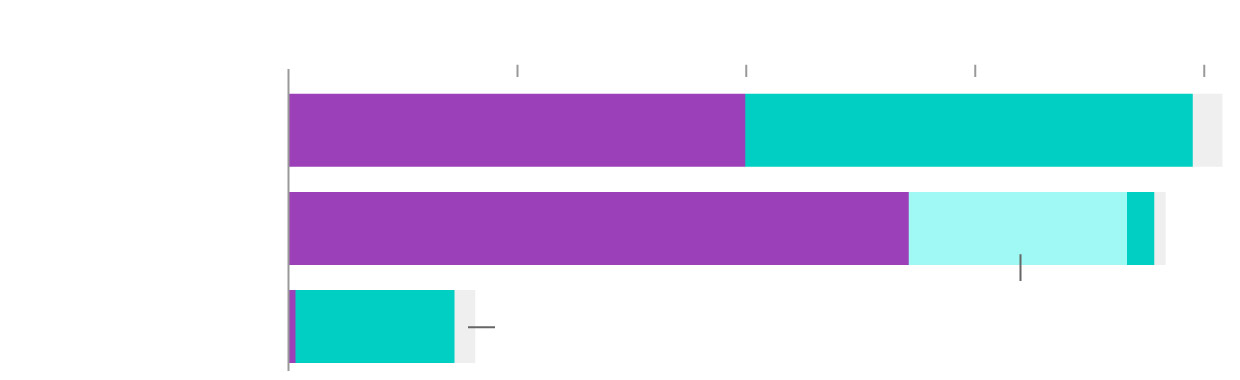

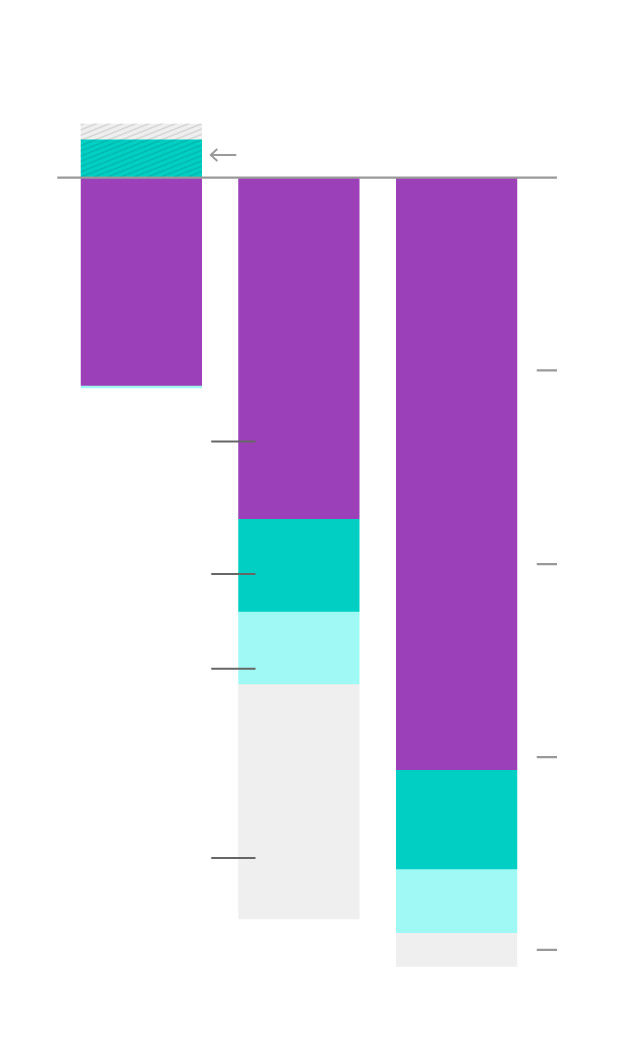

So where has all the central banks’ money gone?

They bought a lot of bonds, of course, helping their governments fund stimulus programs.

ASSETS ADDED SINCE MAR. 2020

0

1

2

3

$4 TRILLION

European

Central Bank

BONDS

LOANS

Federal Reserve

MORTGAGE-BACKED

SECURITIES

Bank of Japan

OTHERS

ASSETS ADDED SINCE MAR. 2020

0

1

2

3

$4T

European

Central Bank

BONDS

LOANS

Federal Reserve

MORTGAGE-BACKED

SECURITIES

Bank of Japan

OTHERS

European

Central

Bank

Bank of

Japan

Federal

Reserve

0

BONDS

1

OTHERS

2

LOANS

3

MORTGAGE-BACKED

SECURITIES

$4T

ASSETS ADDED

SINCE MAR. 2020

The Fed bought a higher proportion of mortgage-backed securities than its counterparts, desperate to shore up a sector that caused so much trouble during the global financial crisis of 2008. In fact, it spent enough on these assets to buy more than a million homes in New York. Some Fed officials think that mortgage-backed securities are where spending should slow first.

The ECB and BOJ did more with loans, keeping businesses afloat, workers in jobs and preventing bad debts from piling up at banks. Indeed, the Japanese central bank’s extra lending would cover the debts of every company that has gone out of business in the country since the autumn of 2003.

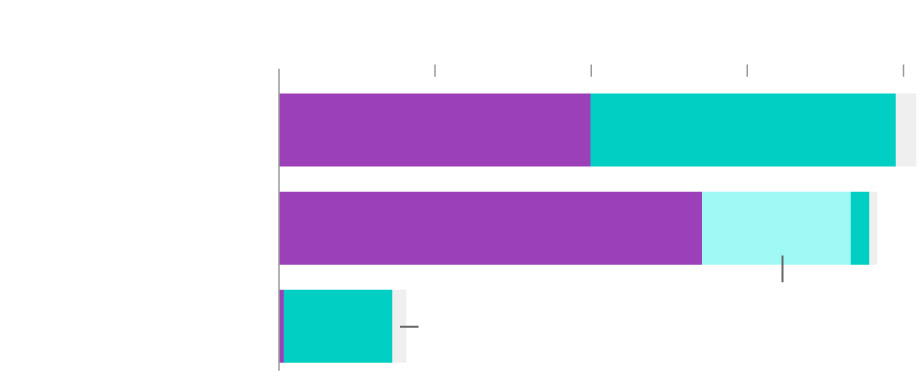

What do the central banks actually “owe?”

Central banks follow basic accounting rules, just like the rest of us, so all those trillions of dollars in assets have liabilities to match. During the pandemic, a lot of that has ended up as bank deposits, keeping lenders flush with liquidity. Getting that money pumping through the economy will be key to sustaining the recovery as central banks dial back stimulus. Government deposits and currency in circulation have also climbed in Europe and the U.S.

LIABILITIES ADDED SINCE MAR. 2020

0

1

2

3

$4 TRILLION

European

Central Bank

Banking sector deposits

Federal Reserve

Government

deposits

Currency in

circulation

OTHERS

Bank of Japan

Deposits reduced

LIABILITIES ADDED SINCE MAR. 2020

0

1

2

3

$4T

European

Central Bank

Banking sector deposits

Federal Reserve

OTHERS

Government

deposits

Currency in

circulation

Bank of Japan

Deposits reduced

European

Central

Bank

Bank of

Japan

Federal

Reserve

Deposits reduced

0

1

Banking

sector

deposits

Government

deposits

2

Currency in

circulation

3

OTHERS

$4T

LIABILITIES ADDED

SINCE MAR. 2020

Has the binge really helped the economy, or just asset prices?

Clearly, the global economy would be in a worse position now if central banks hadn’t jumped in to help avert a financial crisis. And governments wouldn’t have been able to fund their health and welfare spending without the help of central banks.

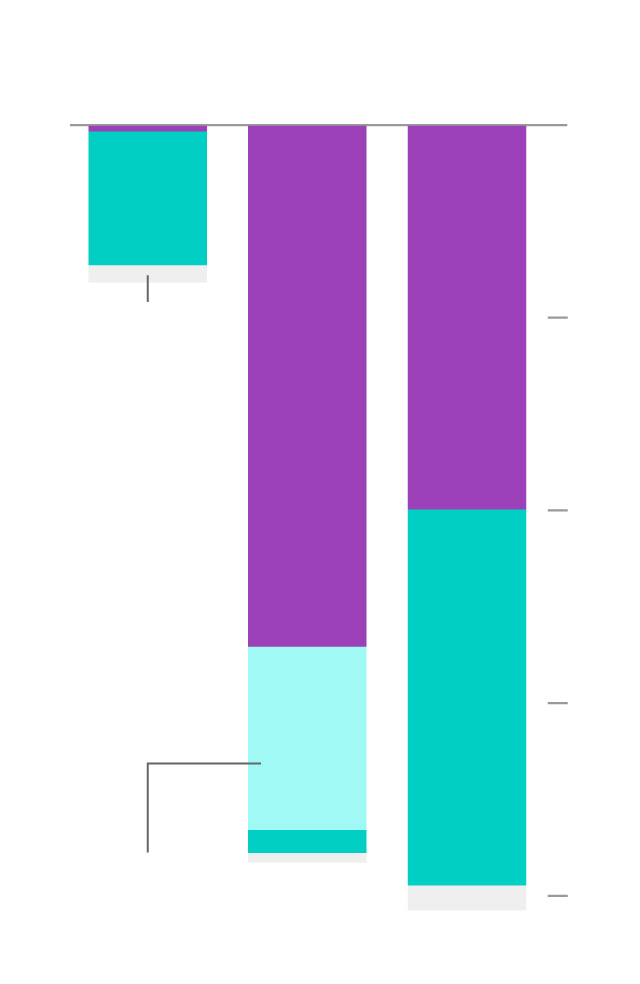

But it’s also clear that many asset classes such as technology stocks and real estate—and the people who own them—have fared better than the average worker over the past year or so. The Fed has the best data illustrating how the rich got richer and the poor slipped even further behind.

Total net worth

growth in 2020

0

20

40

60

80

100%

More than 60% of the wealth growth in 2020 went to the top 10% of the richest U.S. households...

... while only 4% went

to the bottom 50%

Next 9%

Next 40%

Bottom 50%

Top 1% of U.S. households

Total net worth

growth in 2020

0

20

40

60

80

100%

More than 60% of the wealth growth in 2020 went to the top 10% of the richest U.S. households...

... while only 4% went

to the bottom 50%

Next 9%

Next 40%

Bottom 50%

Top 1% of U.S. households

Total net worth

growth in 2020

Top 1% of U.S.

households

0

Next 9%

Next 40%

20

More than 60% of the wealth growth in 2020 went to the top 10% of the richest U.S. households...

40

60

Bottom 50%

80

... while only 4% went

to the bottom 50%

100%

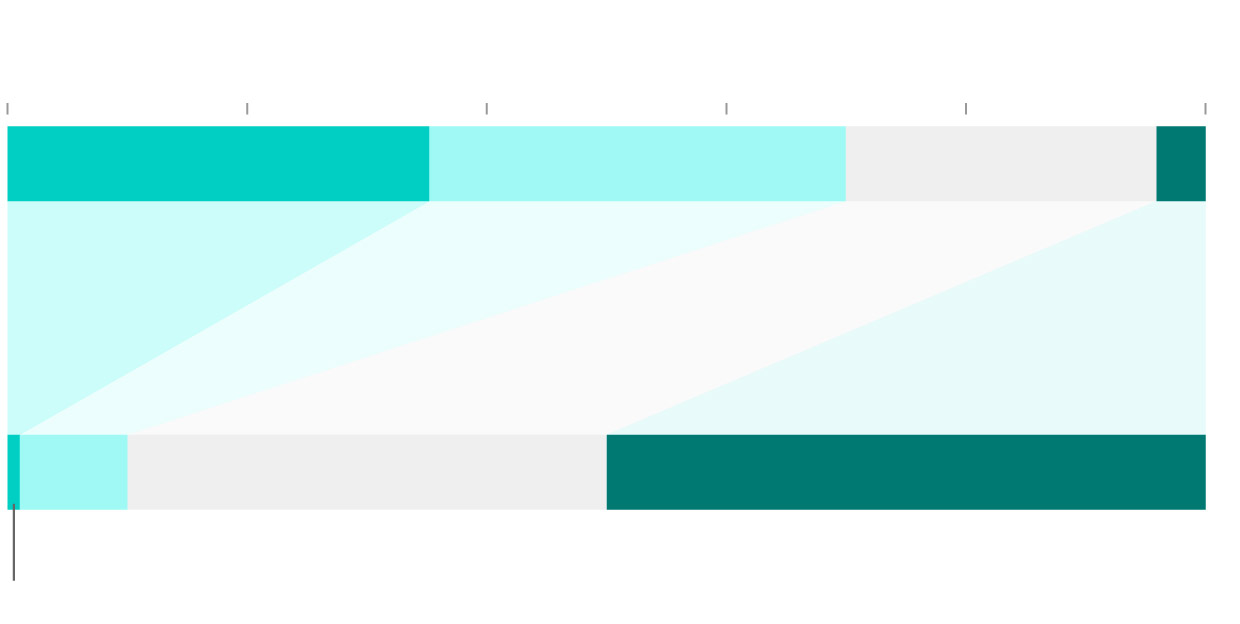

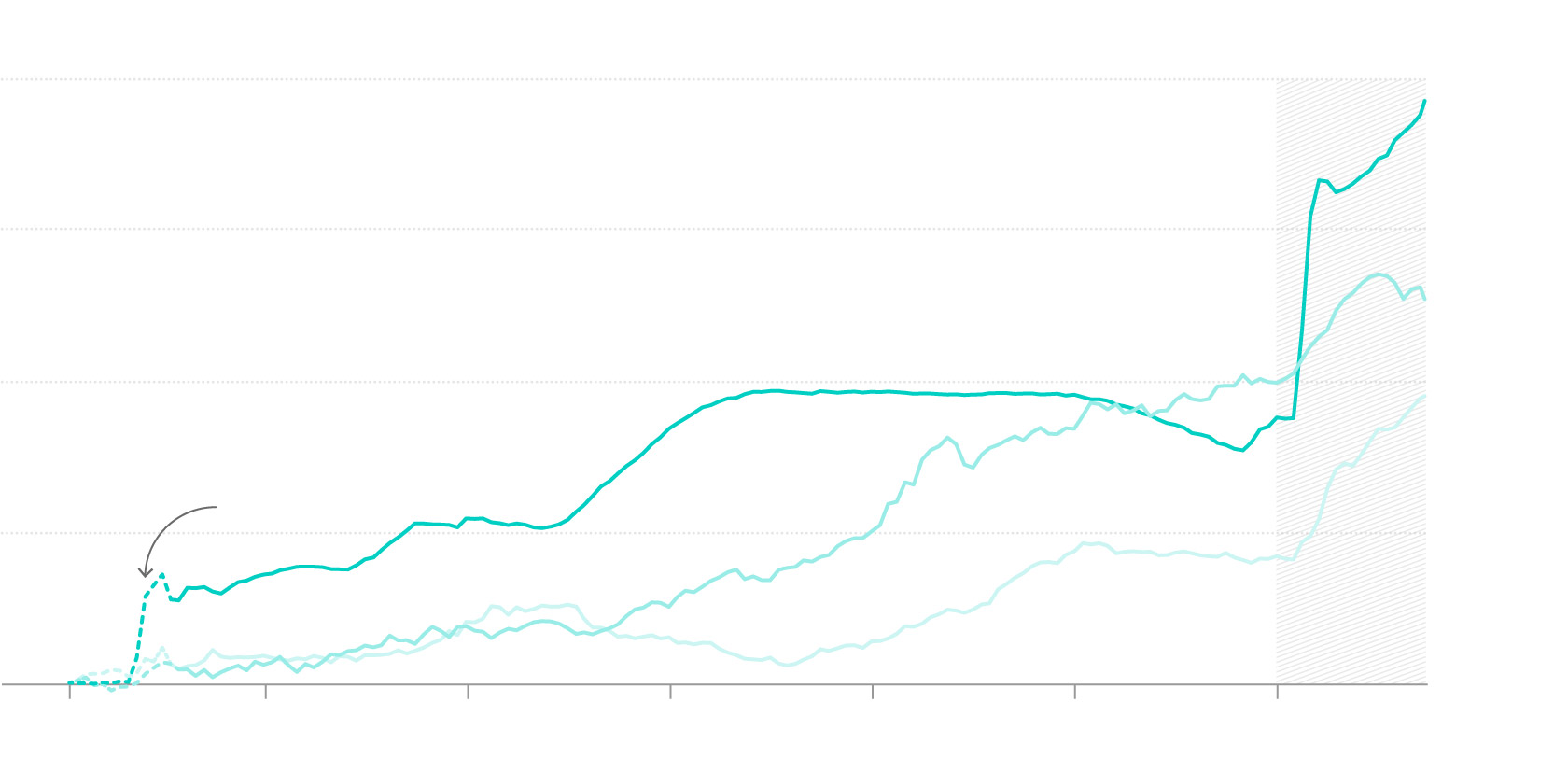

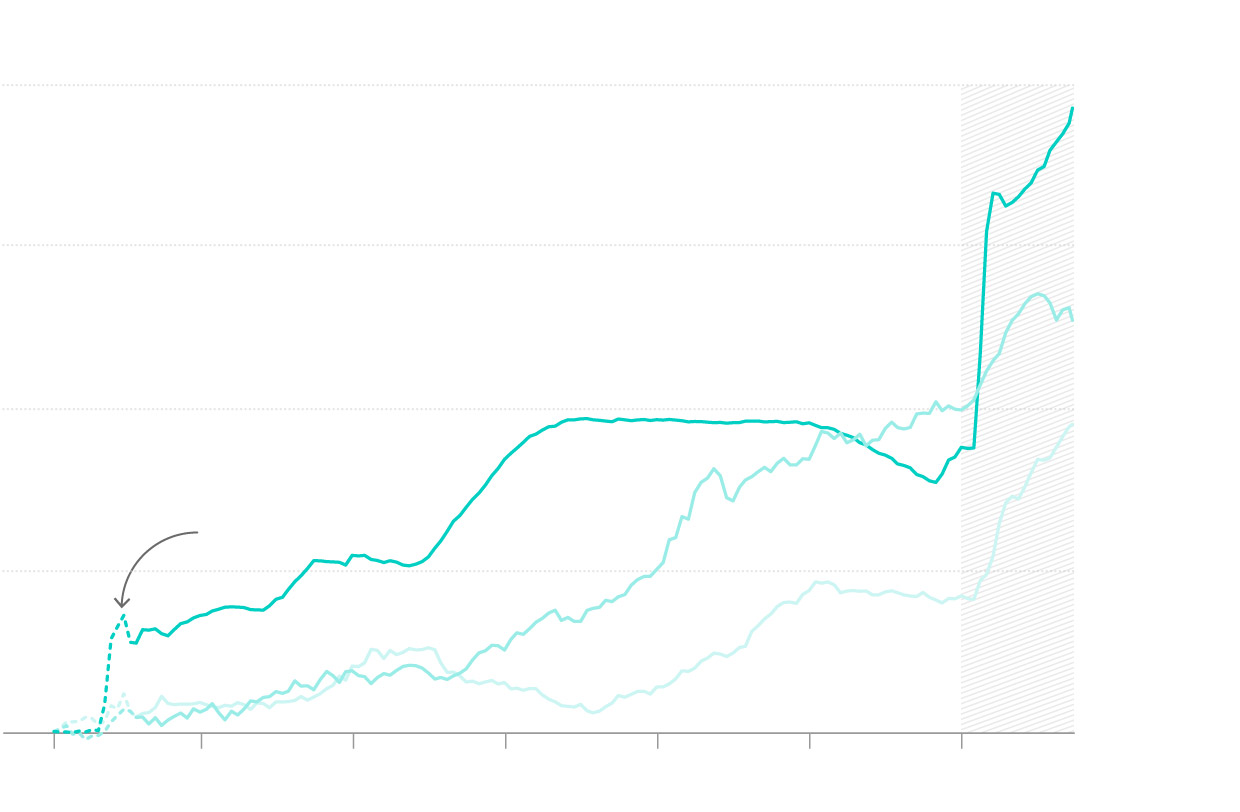

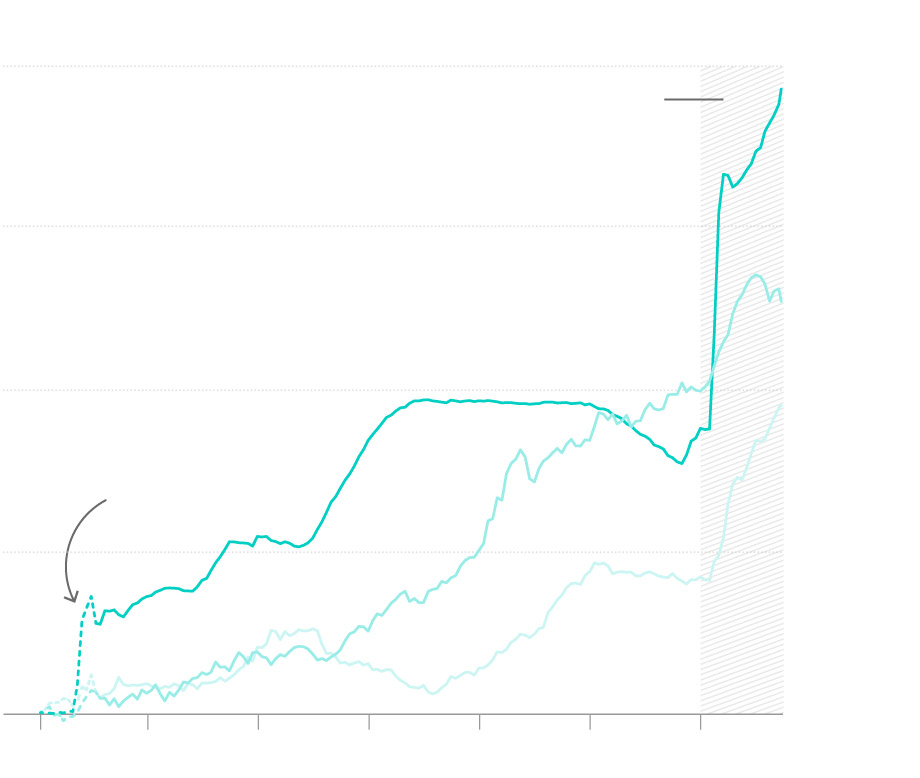

Is there a limit to how long this binge can continue?

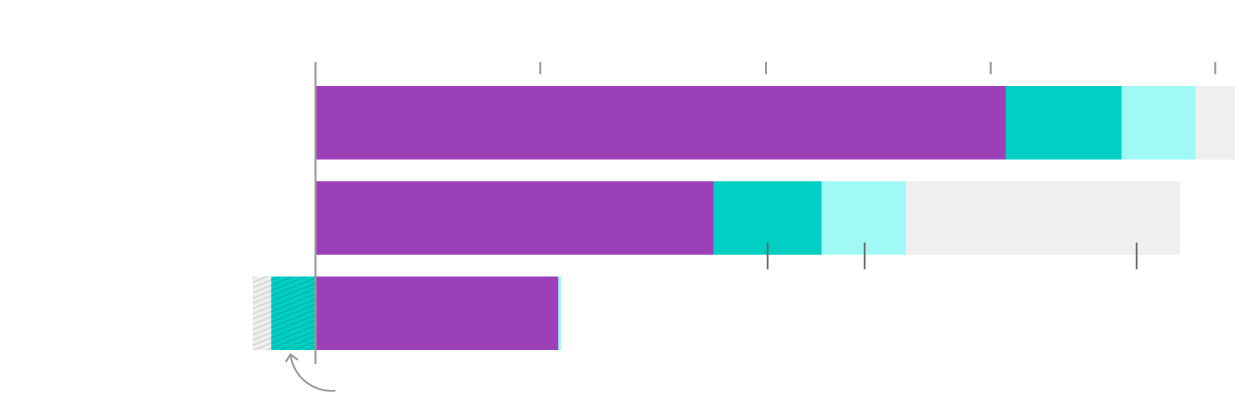

No one really knows. Some worry inflation will spike because of all the cash injected into the economy. Others are concerned about the outsized influence of central banks in free markets—the BOJ for instance owns almost half of all the outstanding Japanese government bonds.

Japan has been buying bonds for decades and its balance sheet is now larger than the economy. The Fed and ECB would need to keep buying at their current clip for years to approach that level, suggesting they may not be out of policy room yet.

U.S.

Eurozone

Japan

$25T

$15T

$8T

GDP

20

6

10

15

4

10

5

2

5

Central bank balance sheet

0

0

0

2017

2018

2019

2017

2018

2019

2017

2018

2019

2020

2021

2020

2021

2020

2021

U.S.

Eurozone

Japan

$25T

$15T

$8T

GDP

20

6

10

15

4

10

5

2

5

Central bank

balance sheet

0

0

0

2017

2019

2017

2019

2017

2019

2021

2021

2021

U.S.

Eurozone

Japan

$25T

$15T

$8T

GDP

20

6

10

15

4

10

5

2

5

Central bank

balance sheet

0

0

0

2017

2019

2017

2019

2017

2019

2021

2021

2021

U.S.

$25T

GDP

20

15

10

5

Central bank balance sheet

0

2017

2018

2019

2020

2021

Eurozone

$15T

10

5

0

2017

2018

2019

2020

2021

Japan

$8T

6

4

2

0

2017

2018

2019

2020

2021

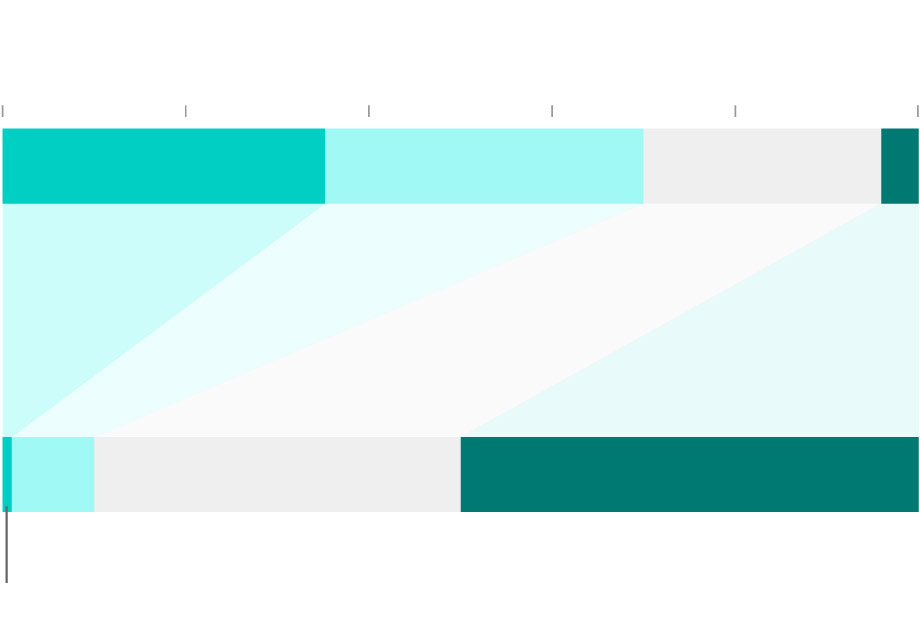

So what comes next?

The Fed last month said it will begin a discussion about reducing the scale of its purchases — a process known as “tapering.” Since then, a flurry of Fed officials have spoken publicly about when and how purchases may slow, perhaps in the hope that financial markets will become accustomed to the idea.

The BOJ is spending less on exchange-traded funds. But it has pledged to keep buying bonds for as long as needed to revive inflation, which remains a long way below target. The ECB has promised to keep splashing the cash too, wary of criticism it pulled back too early after the last crisis.

COVID-19

PANDEMIC

Balance sheet increased

800% since Jan. 2008

Federal

Reserve

600

Bank of

Japan

400

European

Central

Bank

GLOBAL

FINANCIAL

CRISIS

200

0

2008

2010

2012

2014

2016

2018

2020

COVID-19

PANDEMIC

Balance sheet increased

800% since Jan. 2008

Federal

Reserve

600

Bank of

Japan

400

European

Central

Bank

GLOBAL

FINANCIAL

CRISIS

200

0

2008

2010

2012

2014

2016

2018

2020

Balance sheet increased

800% since Jan. 2008

Federal

Reserve

COVID-19

PANDEMIC

600

Bank of

Japan

400

European

Central

Bank

GLOBAL

FINANCIAL

CRISIS

200

0

2008

2010

2012

2014

2016

2018

2020

Federal Reserve

Bank of Japan

European Central Bank

Balance sheet increased

800% since Jan. 2008

COVID-19

PANDEMIC

600

400

GLOBAL

FINANCIAL

CRISIS

200

0

2008

2010

2012

2014

2016

2018

2020

For now, the trio are still spending hundreds of billions of dollars each month to support the post-pandemic recovery. And while slowing the rate of purchases may be on the horizon, especially for the U.S., reversing course and actually selling securities remains a distant proposition. Weaning the world off such huge doses of stimulus will shape the economic and market landscape for years to come.

Notes: China’s central bank hasn’t undertaken a large-scale asset-purchase program over the past year, so we have excluded it from this story. The People’s Bank of China’s total assets are around $6 trillion. Company valuations in the lead graphic are based on their stock market capitalization as of June 23, 2021. The Fed and BOJ numbers are as of June 30, 2021, and the ECB’s as of June 25, 2021.