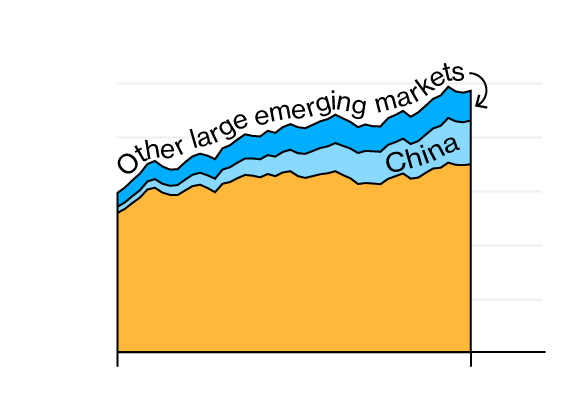

World debt

$250T

Mature markets

0

2018

2007

World debt

$250T

Mature markets

0

2018

2007

As China’s Debt Balloons, Other Emerging Markets Fail to Take Off

In 2008, as the Lehman Brothers bankruptcy triggered an epic credit crisis across the developed world, everyone braced for the inevitable crisis in the emerging markets that would follow. It didn’t happen.

That year’s financial chaos created problems for these economies, whose stock and bond markets dipped far more than those of the U.S. or Europe; but they avoided wholesale defaults or devaluations. There was no repeat of the cycle of emerging market crises that had roiled the world in past decades. By showing great resilience, these markets demonstrated that they had at last begun to emerge. What has happened since has been more concerning.

Where there is debt there is risk. In 2007, on the eve of the crisis, the bigger emerging markets tended to have far less total debt as a percentage of GDP than developed economies. That remains true.

However, there is an important exception. Once very lightly leveraged, China’s debt to GDP is now approaching the levels typically seen in developed markets. Its total debt has increased sevenfold since the crisis, to account on its own for more than half the outstanding debt of all the emerging market countries tracked by the Institute of International Finance.

This has transformed the world of debt into a bipolar one, with the U.S. and China by far the biggest debtors. With this much debt, any problems for the Chinese economy are now potentially far more dangerous for the rest of the world. Small wonder that global markets now react to every new signal about growth in China.

- 2007 total debt

- 2018 total debt

Canada

Russia

U.K.

Germany

South Korea

Luxembourg

France

Japan

China

U.S.

Italy

Spain

India

Mexico

Brazil

Australia

South Africa

Argentina

Canada

Russia

U.K.

Germany

South Korea

Luxembourg

France

Japan

U.S.

China

Italy

Spain

India

Mexico

Brazil

Australia

South Africa

Argentina

Canada

Russia

U.K.

Germany

South Korea

France

Japan

China

U.S.

Italy

Spain

India

Mexico

Brazil

Australia

South Africa

Argentina

Russia

Canada

U.K.

Germany

South Korea

France

Japan

U.S.

Italy

Spain

China

India

Mexico

Brazil

South Africa

Australia

Argentina

Within China, all forms of debt have risen, reflecting a shift in the dynamics of its economy. Before the crisis, China had largely managed to finance its growth without recourse to much debt. The inflows from exports had done the job. The population, fast reaching middle-class living standards, still tended to fund itself conservatively. But household debt has almost tripled from 18.8% of China’s GDP before the crisis to 51.2%. All this debt has successively less impact in stimulating economic growth.

Corporates leading the way in China

There are reasons why China’s debt is not creating greater fears. If countries want to avoid crisis, issuing a greater share of debt in their own currency is key. This avoids the risk that a devaluation can force them into default, and it leaves them with the option—not necessarily a good one—of printing money to escape difficulties.

China does more than 90% of its borrowing in local currency, which limits the risks somewhat. Meanwhile, almost all large emerging markets now do more than half of their borrowing in their own currency. But not all emerging markets have made uniform progress in converting to local market debt. The two biggest exceptions are Argentina and Turkey—and it is no coincidence that these two countries both slipped into crisis during 2018 as a strong dollar put pressure on their currencies.

But the result across the emerging world has been very healthy returns on debt for investors. The main Bloomberg Barclays debt index for the emerging world, including both government and high-grade corporate debt, has comfortably beaten the equivalent U.S. index since the year before the crisis. And anyone buying at the worst of the panic in 2008 would have been rewarded with a nice uptick in returns. Local currency debt has been much weaker, but has avoided a major crisis.

All of this is very different from the results for emerging market equity investors, who have suffered through a long and grinding bear market. Any luckless investor who bought MSCI’s emerging markets stock index when it peaked around Halloween 2007 would still be sitting on losses today, even after reinvestment of dividends.

That reflects a sad paradox of the last decade. The emerging markets have demonstrated “emergence” when it came to making themselves more resilient to shocks and crises. But they have failed to fulfill hopes that they could continue being a motor of growth for the world–and this was exactly the quality that attracted many western investors in the first place.