The Global Economy Is Still Feeling the Lehman Fallout 10 Years Later

The collapse of Lehman Brothers and subsequent global financial crisis sent shockwaves through the world economy, many of which still reverberate a decade later.

The deepest international recession since the Great Depression prompted central banks to deliver massive and unorthodox monetary stimulus, while governments either eased fiscal policy or delivered austerity depending on the country.

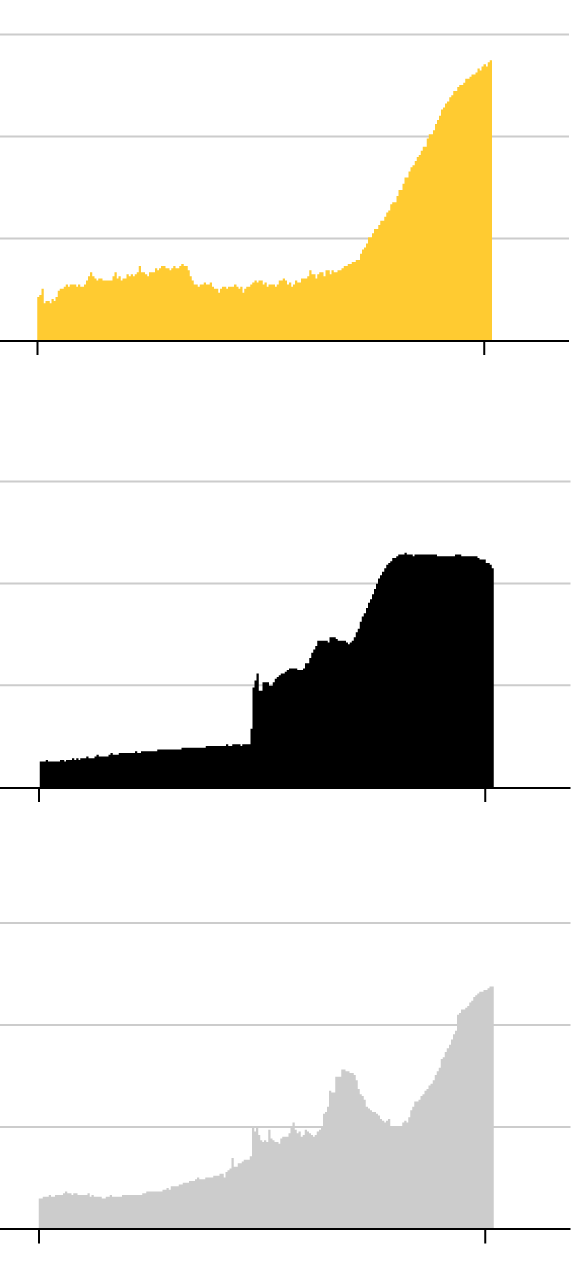

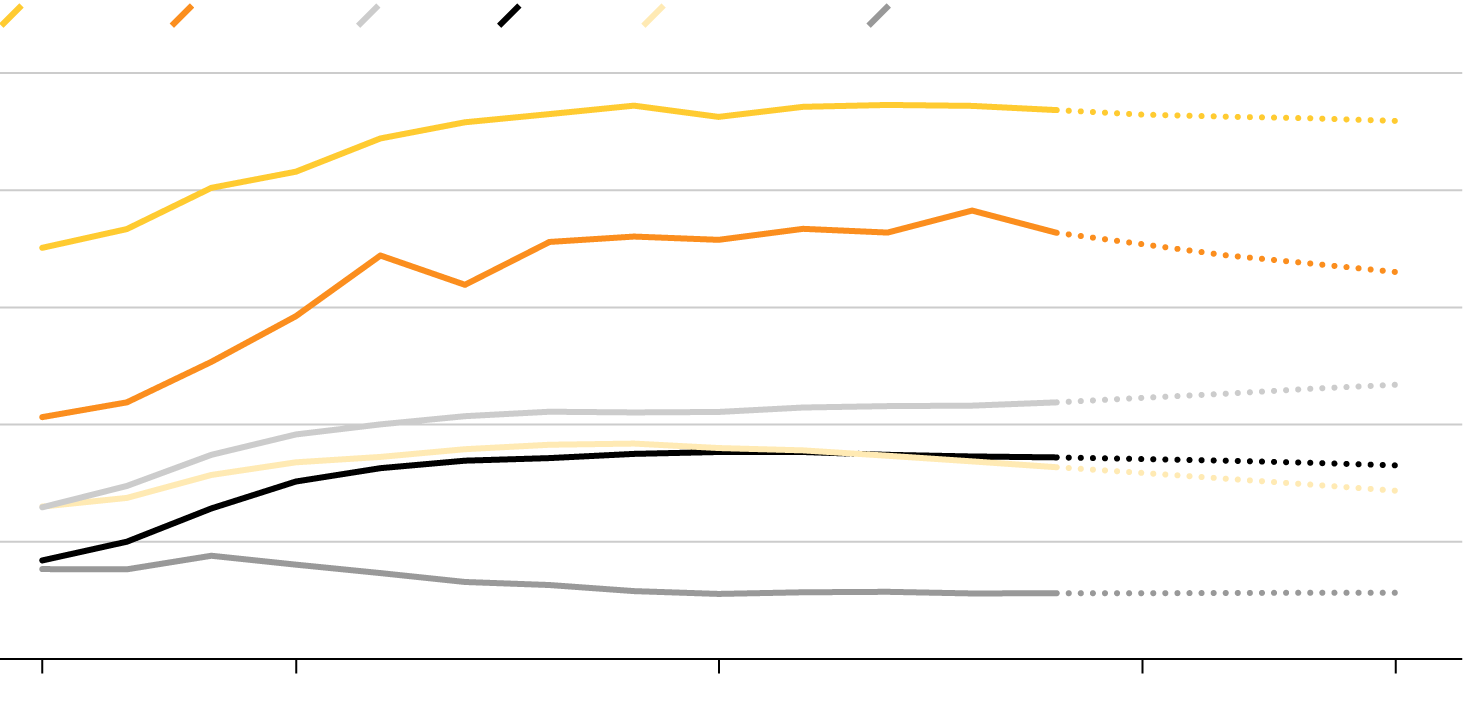

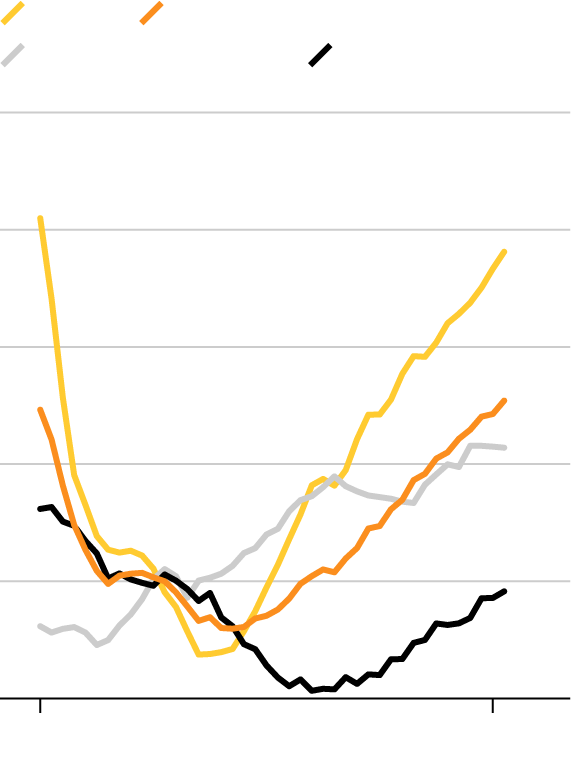

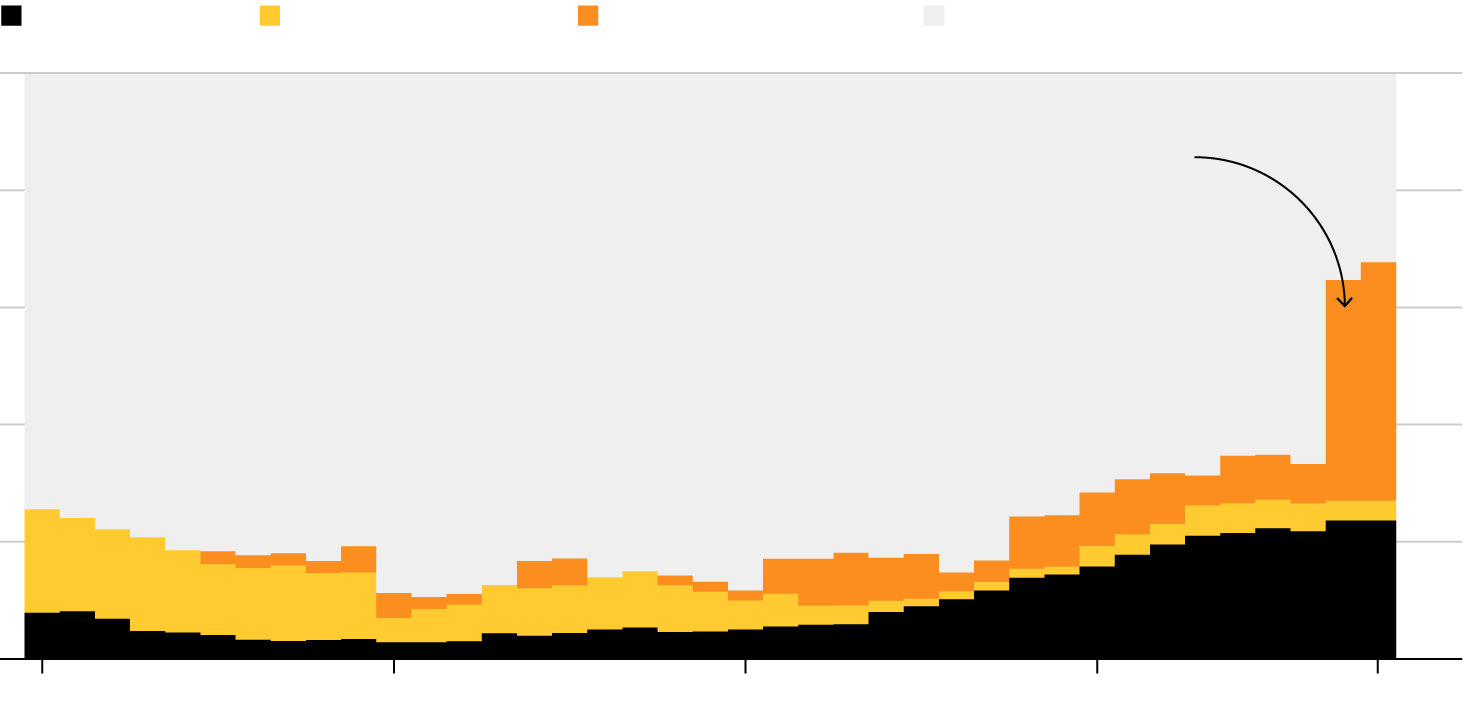

Central Bank Balance Sheets

¥600T

Bank of Japan

400

200

0

2018

2000

$6T

Federal Reserve

4

2

0

2000

2018

€6T

European Central Bank

4

2

0

2000

2018

Bank of Japan

Federal Reserve

European Central Bank

¥600T

$6T

€6T

4

400

4

200

2

2

0

0

0

2018

2018

2018

2000

2000

2000

Bank of Japan

Federal Reserve

European Central Bank

¥600T

$6T

€6T

4

400

4

200

2

2

0

0

0

2000

2018

2000

2018

2000

2018

Having cut interest rates to almost zero or even lower in some cases, central banks started buying bonds in a bid to reignite animal spirits among companies and consumers. The result? An unprecedented swelling of their balance sheets which while set to peak is unlikely to ever be reversed.

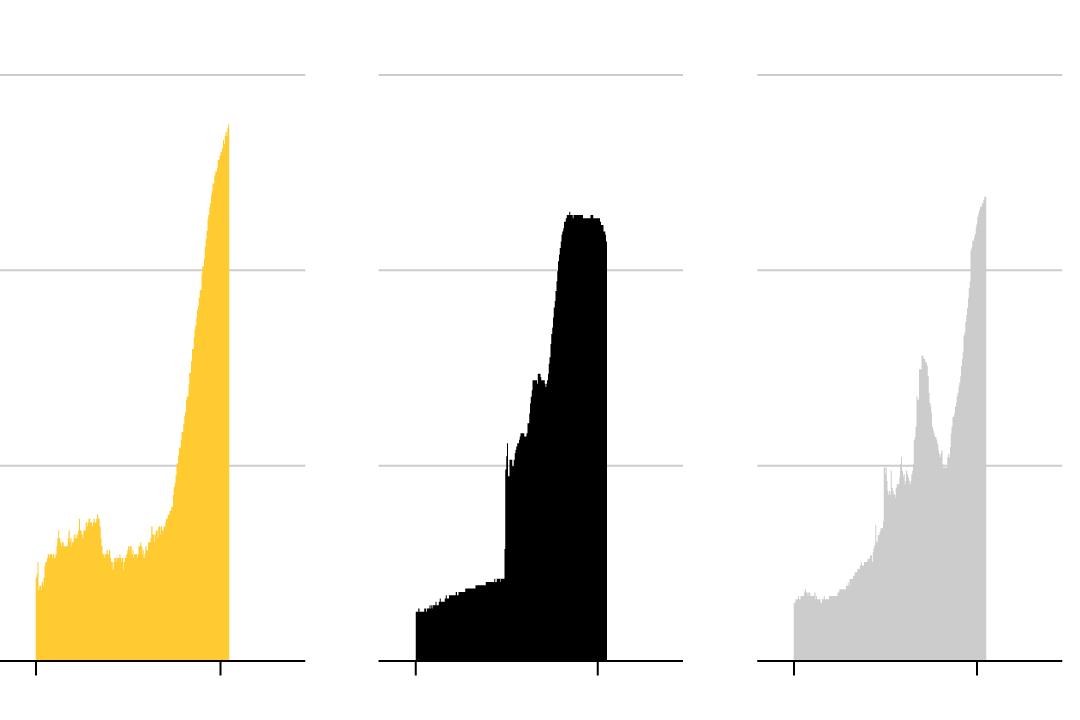

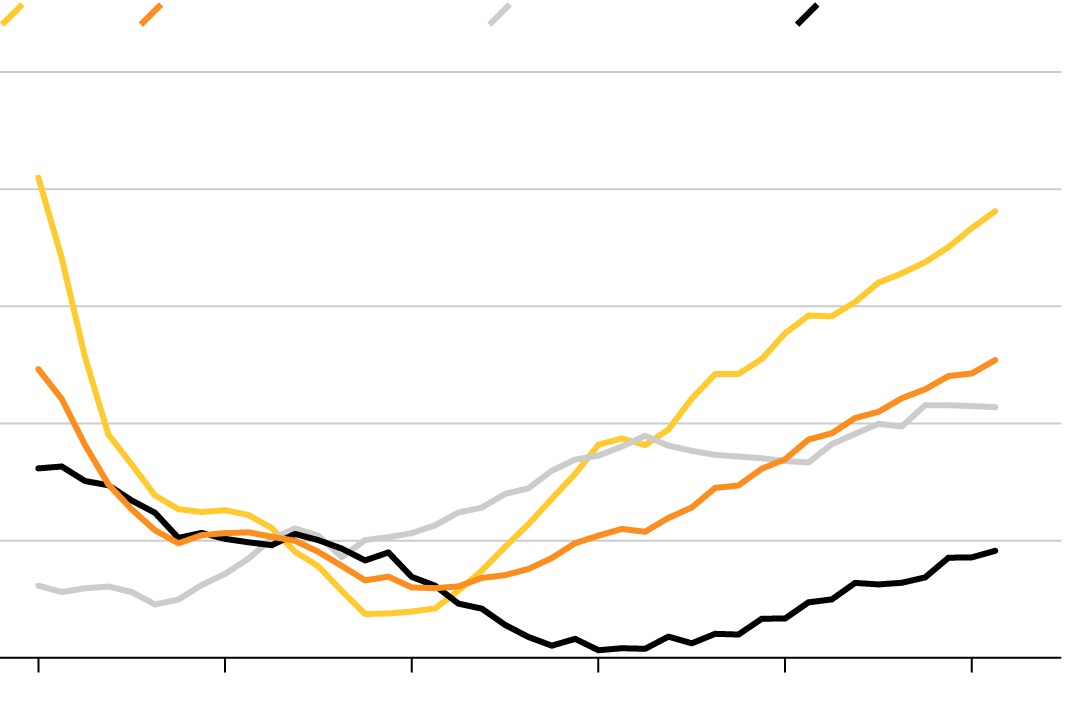

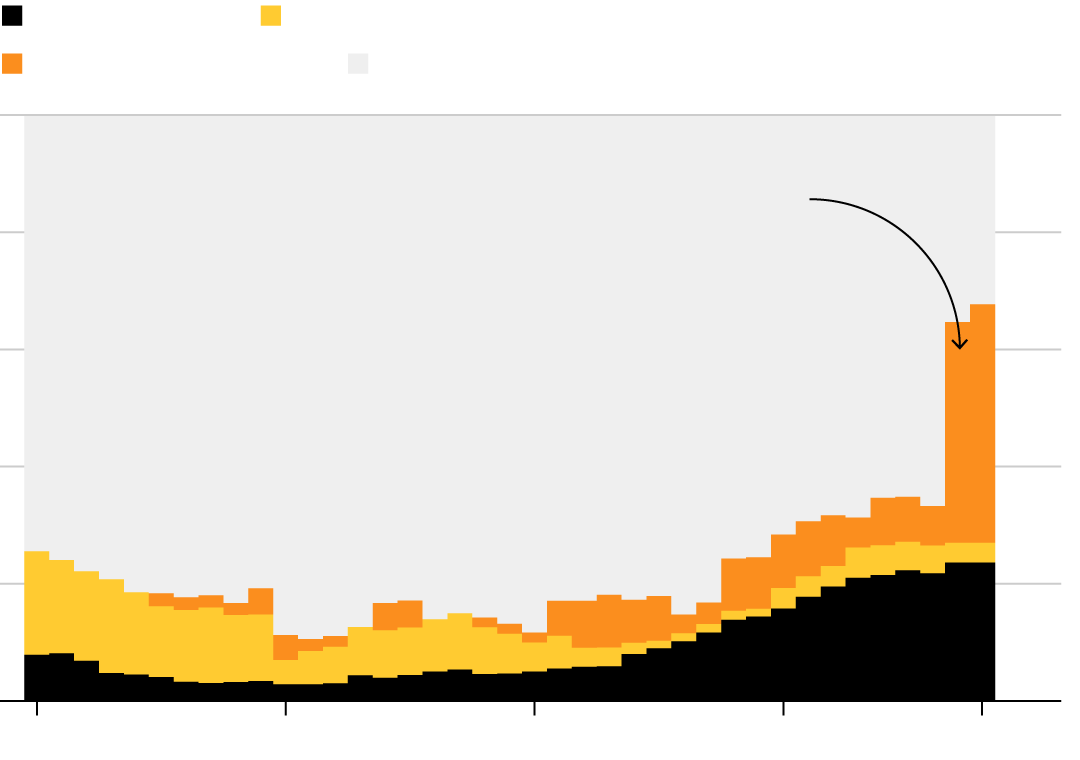

Government Debt

Japan

Greece

U.S.

U.K.

Euro area

Turkey

250% of GDP

200

150

100

50

0

2007

2023

Japan

Greece

U.S.

U.K.

Euro area

Turkey

250% of GDP

200

150

100

50

0

2007

2011

2015

2018

2023

Japan

Greece

U.S.

U.K.

Euro area

Turkey

250% of GDP

200

150

100

50

0

2007

2010

2015

2020

2023

For all the talk of austerity, government debts in most parts of the world are larger now than in 2007, potentially a risk for economies in the future as central bankers tighten monetary policy.

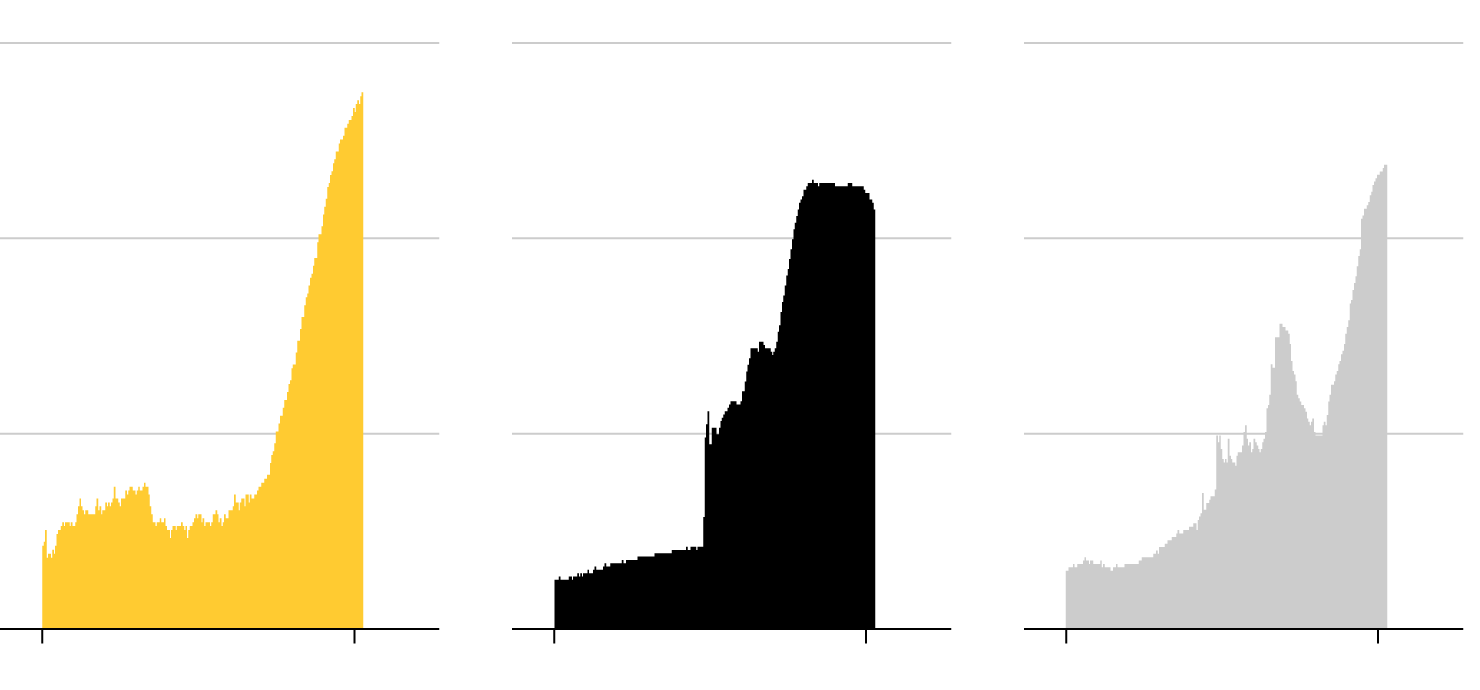

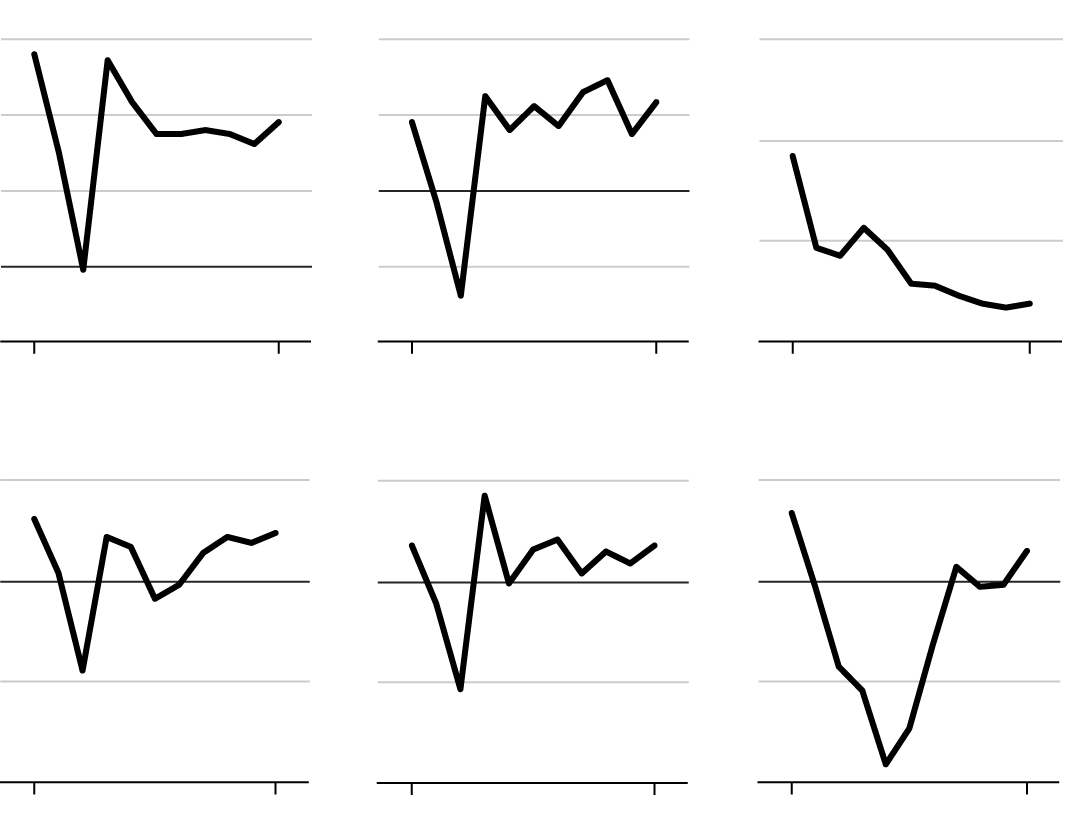

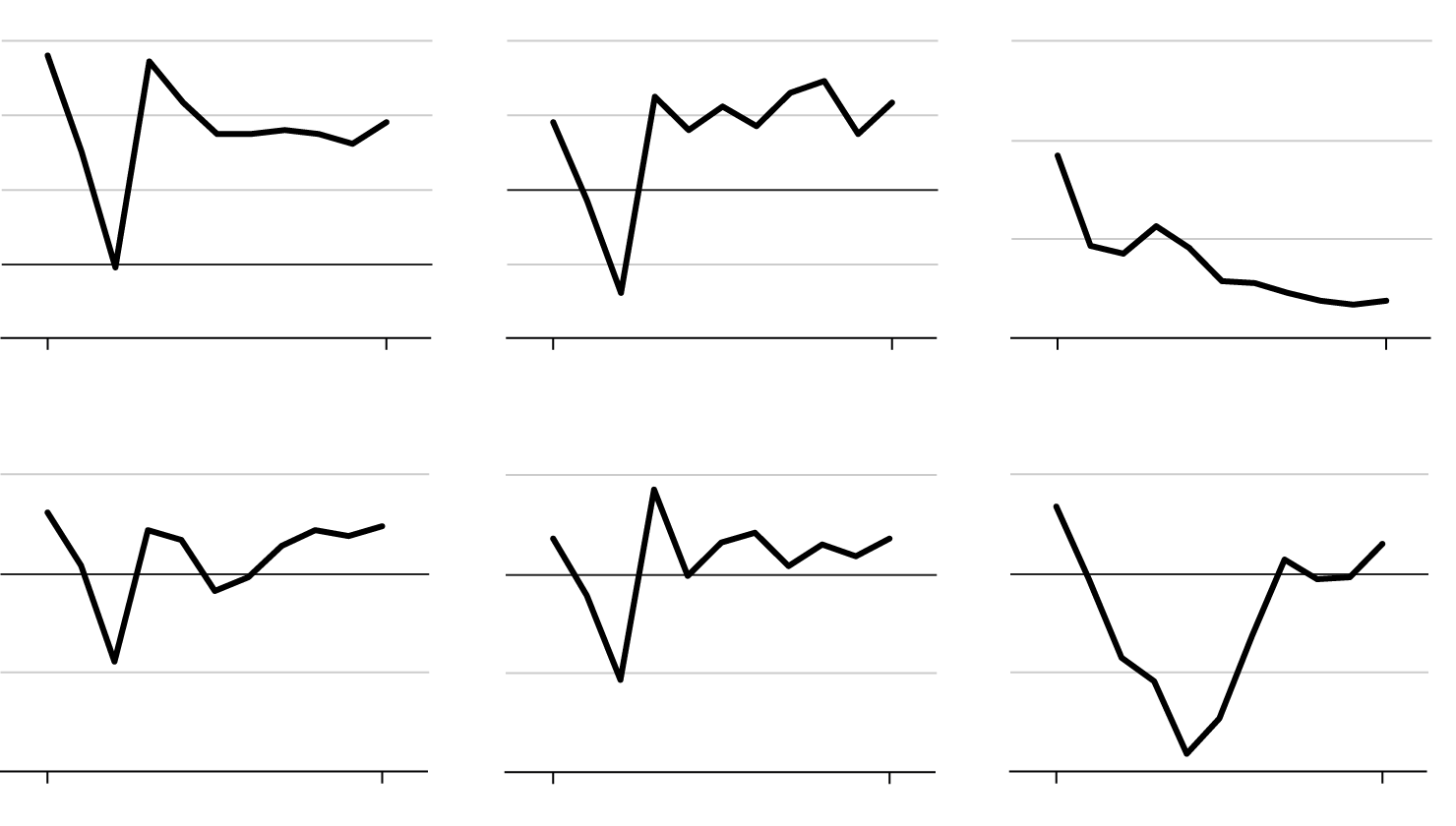

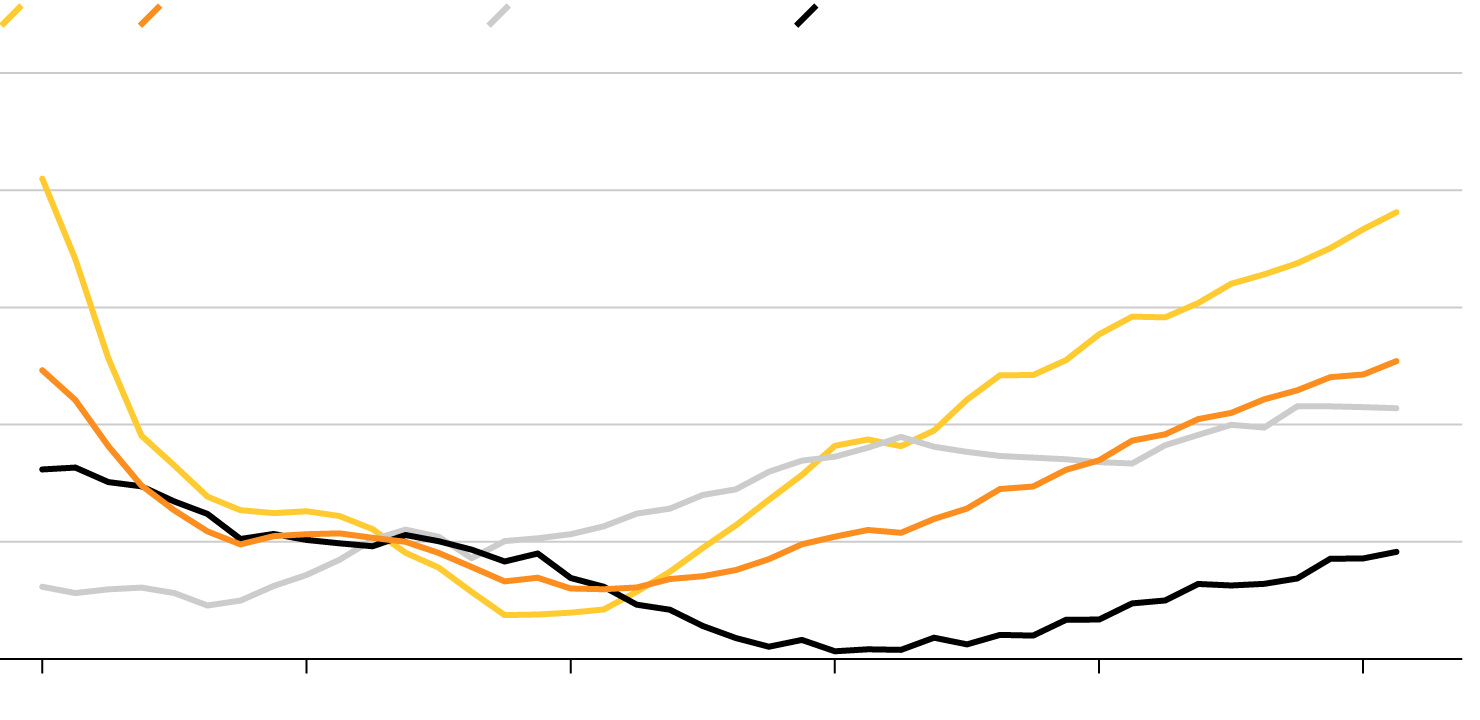

Economic Output

World

U.S.

6%

4%

4

2

2

0

0

-2

-2

-4

2007

2017

2007

2017

China

Euro area

5%

20%

15

0

10

-5

5

-10

2007

2017

2007

2017

Japan

Greece

5%

5%

0

0

-5

-5

-10

-10

2007

2017

2007

2017

World

U.S.

China

6%

4%

20%

4

2

15

2

0

10

0

-2

-2

-4

5

2007

2017

2007

2017

2007

2017

5%

5%

Euro area

Japan

Greece

5%

0

0

0

-5

-5

-5

-10

-10

-10

2007

2017

2007

2017

2007

2017

World

U.S.

China

6%

4%

20%

4

2

15

2

0

10

0

-2

-2

-4

5

2007

2017

2007

2017

2007

2017

Euro area

Japan

Greece

5%

5%

5%

0

0

0

-5

-5

-5

-10

-10

-10

2007

2017

2007

2017

2007

2017

The world economy collapsed into its deepest recession since World War II in the wake of the crisis, yet after initially bouncing, most economies showed only moderate growth for most of the past decade.

Unemployment

Africa

Americas

Arab states

Asia and the Pacific

Europe and central Asia

200M

150

100

50

0

2000

2005

2010

2015

2020

Africa

Americas

Arab states

Asia and the Pacific

Europe and central Asia

200M

150

100

50

0

2000

2005

2010

2015

2020

Africa

Americas

Arab states

Asia and the Pacific

Europe and central Asia

200M

150

100

50

0

2000

2005

2010

2015

2020

Some 25 million more people are now unemployed than back in 2007 even as the U.S. jobless rate falls. Particularly eye-catching is the youth unemployment rate in countries such as Greece, where—while down from over 60 percent in 2013—it’s still hovering at 40 percent.

G-7 Wages

Canada

France

3%

4%

2

2

1

0

0

-1

-2

2008

2017

2008

2017

Germany

Italy

3%

2%

0

2

1

-2

0

-4

2008

2017

2008

2017

4%

2%

Japan

U.K.

2

0

0

-2

-2

-4

2008

2017

2008

2017

U.S.

3%

2

1

0

-1

2008

2017

Canada

France

Germany

Italy

3%

4%

3%

2%

2

0

2

2

1

0

1

-2

0

-1

-2

0

-4

2008

2017

2008

2017

2008

2017

2008

2017

4%

2%

Japan

U.K.

U.S.

3%

2

2

0

1

0

-2

0

-2

-4

-1

2008

2017

2008

2017

2008

2017

Canada

France

Germany

Italy

3%

4%

3%

2%

2

0

2

2

1

0

1

-2

0

-1

-2

0

-4

2008

2017

2008

2017

2008

2017

2008

2017

4%

2%

Japan

U.K.

U.S.

3%

2

2

0

1

0

-2

0

-2

-4

-1

2008

2017

2008

2017

2008

2017

Source: OECD

The lackluster recovery is best evidenced by the lack of wage pressures across most of the world even as hiring strengthens.

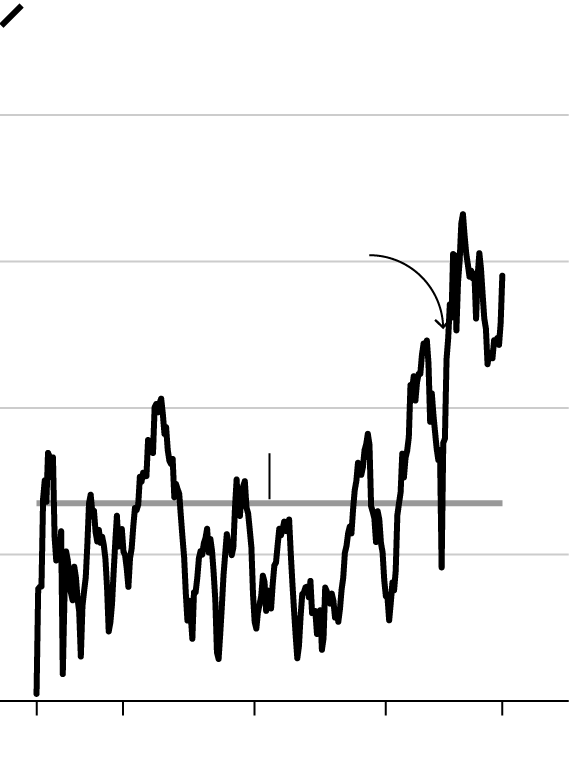

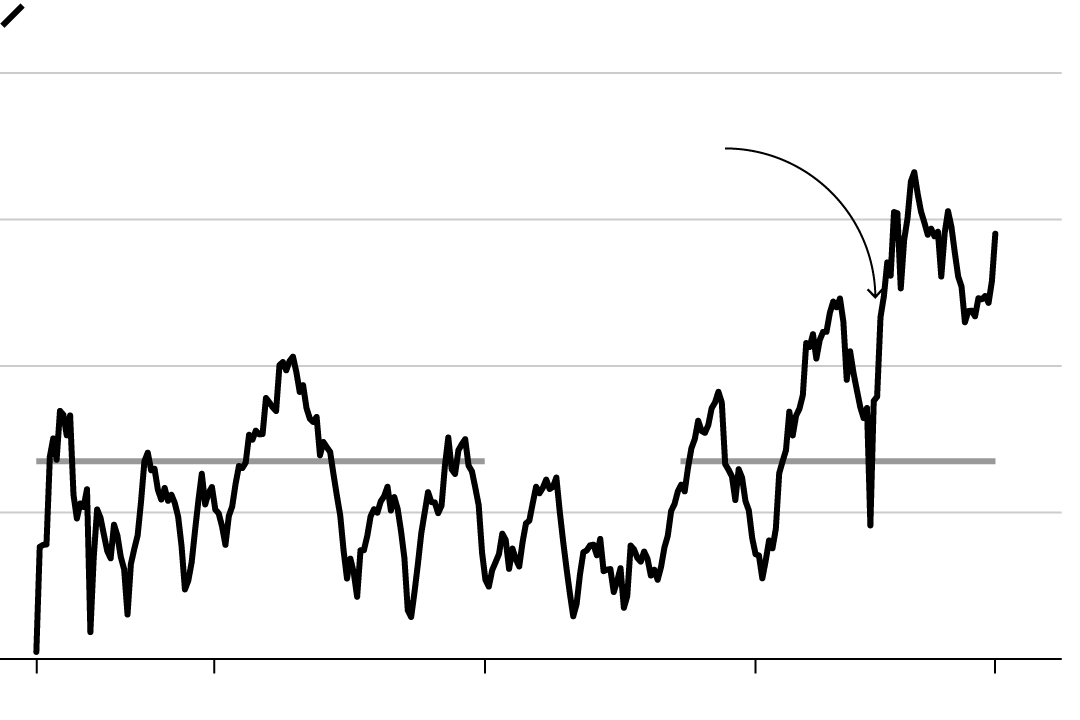

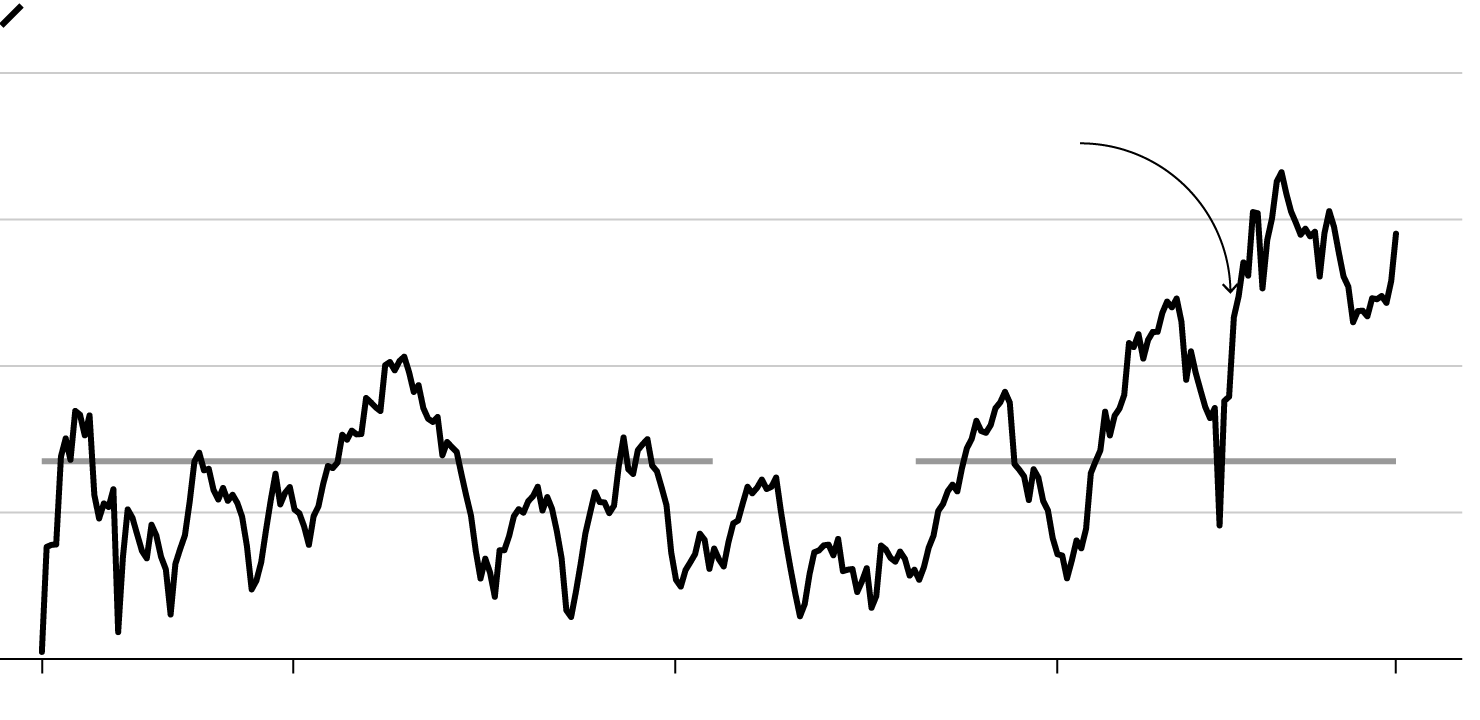

Robust U.S. Corporate Profits Have Coincided With a Strong Stock Market

Quarterly after-tax profits (with IVA, CCA)

share of nominal GDP

12%

10

Expansion

starts

8

Average 6.7%

6

4

1947

1960

1980

2000

2018

Quarterly after-tax profits (with IVA, CCA) share of nominal GDP

12%

Expansion

starts

10

8

Average 6.7%

6

4

1947

1960

1980

2000

2018

Quarterly after-tax profits (with IVA, CCA) share of nominal GDP

12%

Expansion

starts

10

8

Average 6.7%

6

4

1947

1960

1980

2000

2018

If there has been a winner of the past 10 years it’s the corporate sector, which in an age of easy money has seen its stock prices soar and profits start to rise.

House Prices

U.S.

Advanced economies

Emerging markets

Euro area

140

130

120

110

100

90

2008

2018

U.S.

Advanced economies

Emerging markets

Euro area

140

130

120

110

100

90

2008

2010

2012

2014

2016

2018

U.S.

Advanced economies

Emerging markets

Euro area

140

130

120

110

100

90

2008

2010

2012

2014

2016

2018

At the heart of the crisis, house prices have now recovered in most corners of the world, exacerbating the gap between those with assets and those without.

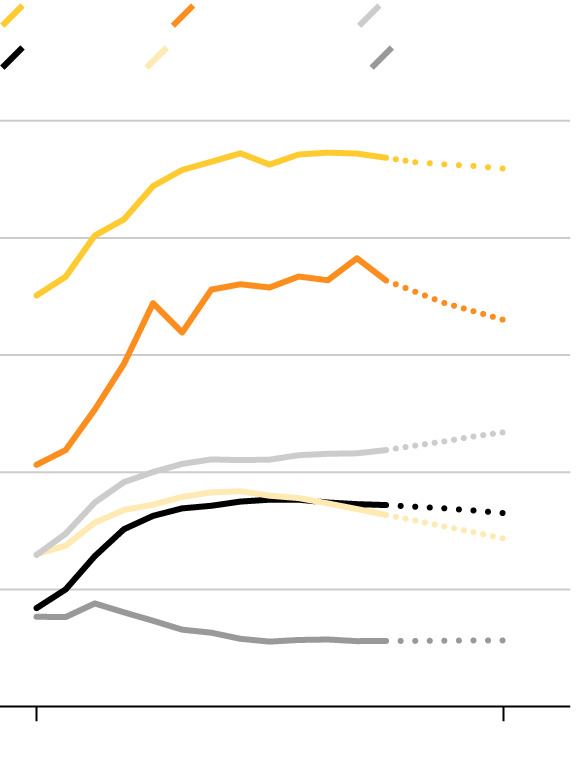

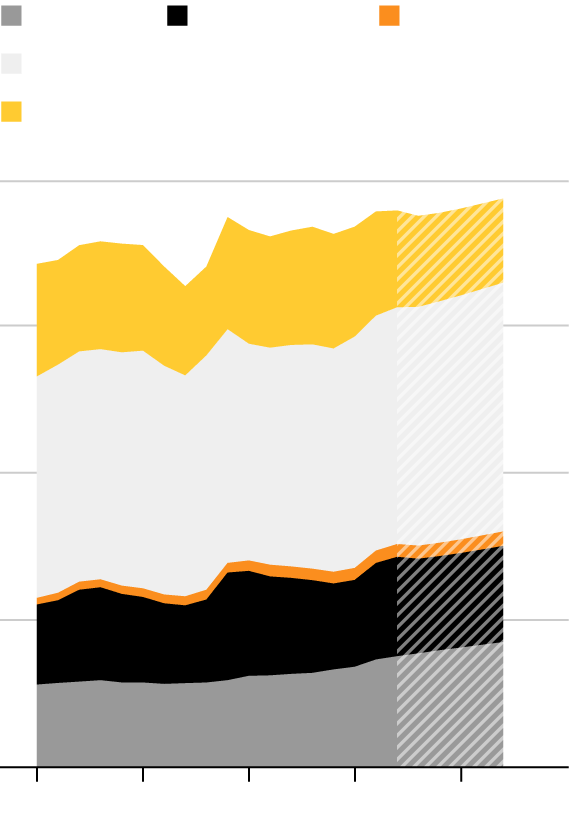

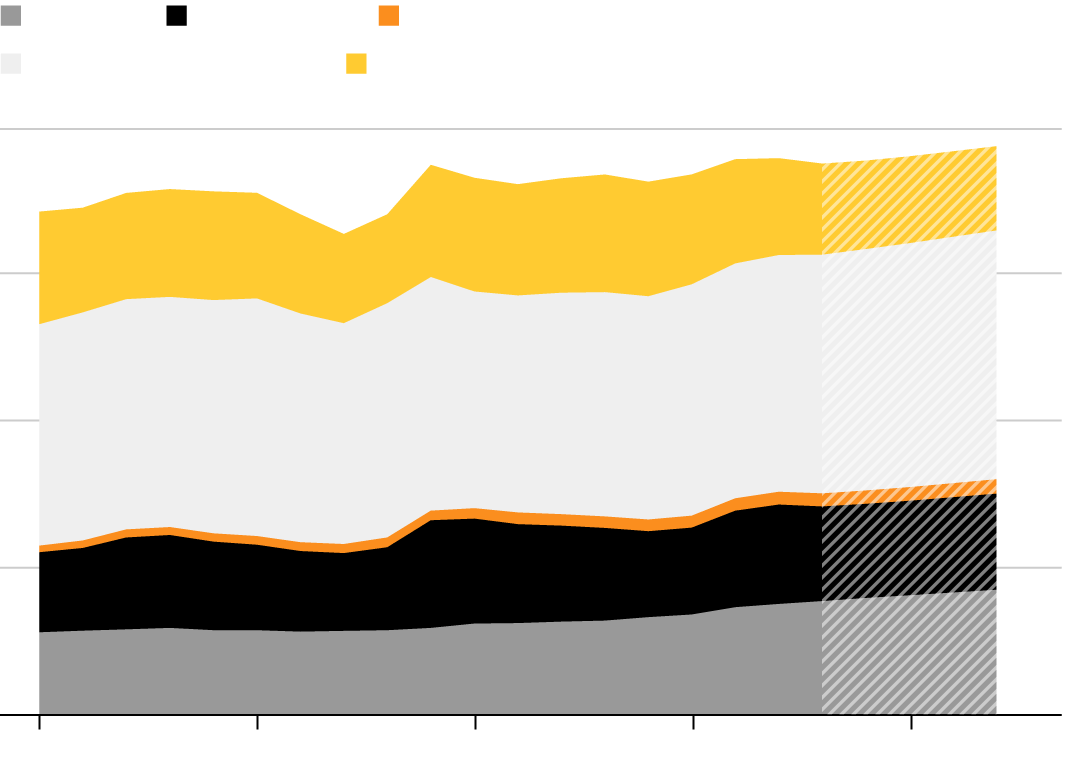

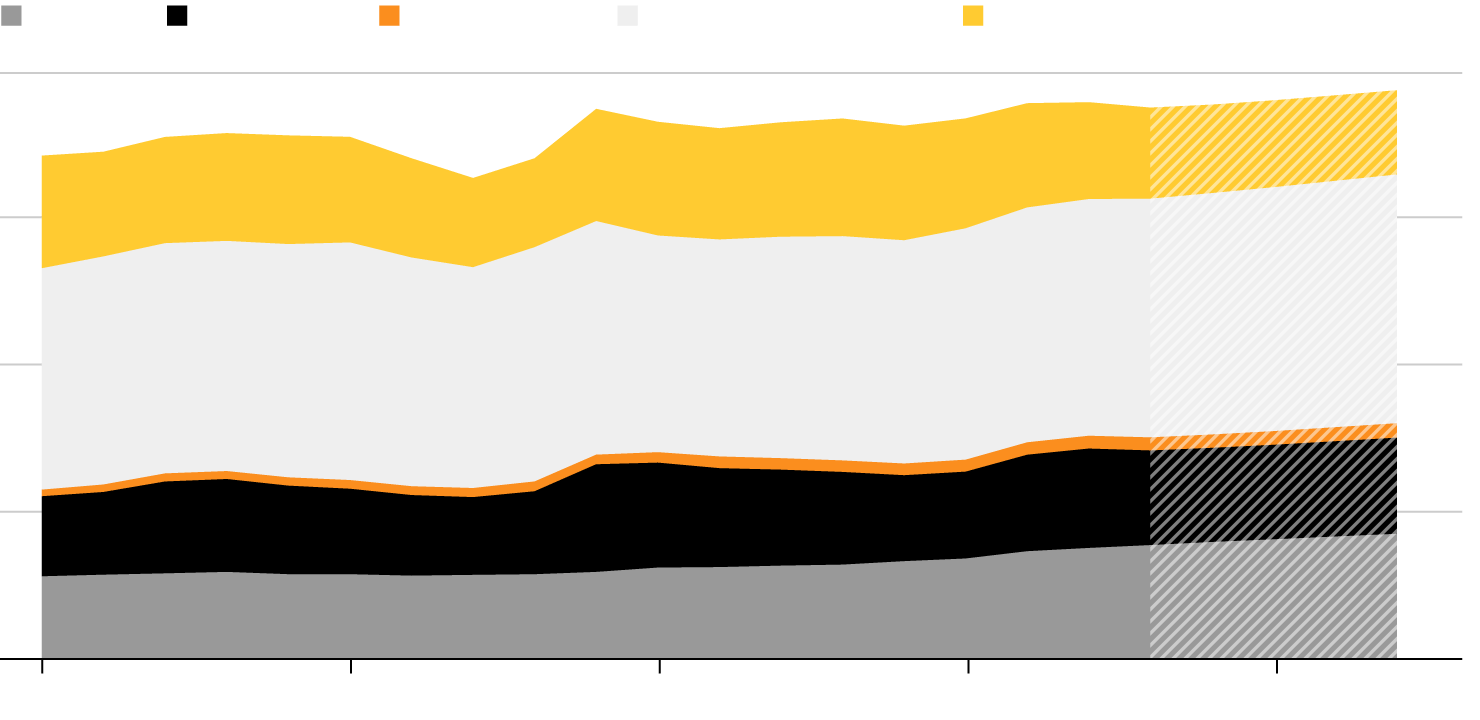

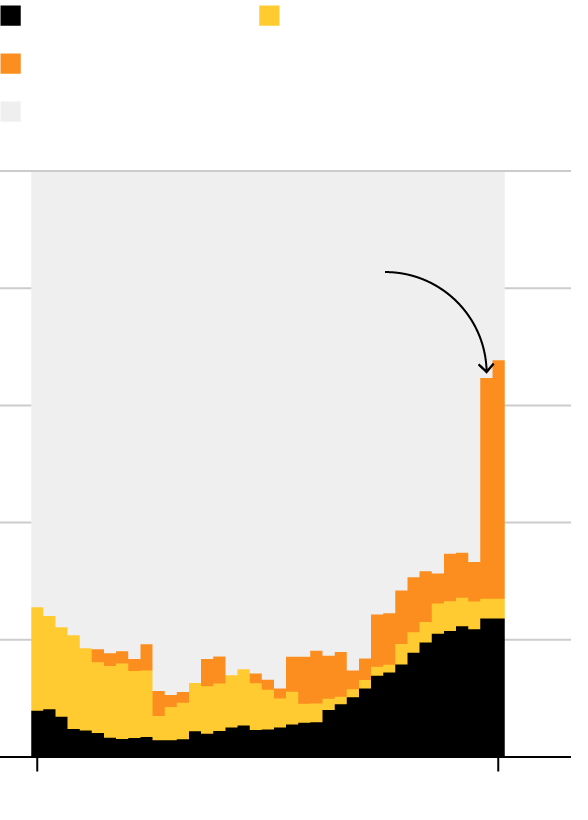

Populists and Authoritarians Now Oversee the Biggest Chunk of G-20 Output

Authoritarian

Weak democracy

Populist democracy

Establishment democracy

100%

80

Trump win flips U.S.

into populist

category

60

40

20

0

1980

2018

Authoritarian

Weak democracy

Populist democracy

Establishment democracy

100%

Trump win flips U.S.

into populist

category

80

60

40

20

0

1980

1990

2000

2010

2018

Authoritarian

Weak democracy

Populist democracy

Establishment democracy

100%

Trump win flips U.S.

into populist

category

80

60

40

20

0

1980

1990

2000

2010

2018

Sources: Bloomberg Economics, Freedom House, IMF

Voters are hitting back at inequality, frustrated by the lack of jobs or low pay for those who have work. As big business bounces back, there has been a backlash at the ballot box with populist wins, such as Donald Trump’s Presidential election victory in the U.S. elections and the U.K.’s vote to leave the European Union.