China Plots What’s Next as Influence on Global Markets Grows

China’s ascension as an economic superstar over the past three-plus decades is out of sync with its heft in global financial markets. But things are starting to change, and investors around the world will feel the difference.

China makes up more than one-seventh of the global economy, yet its footprint in international portfolios is ludicrously small, with overseas investors owning less than 2 percent of its domestic stocks and bonds. But its insulated markets are slowly becoming more integrated, as President Xi Jinping loosens rules on foreign participation. That push could get further backing at the Communist Party's twice-a-decade congress this month, where the leadership will set policy priorities for the coming five years.

Inflection Point

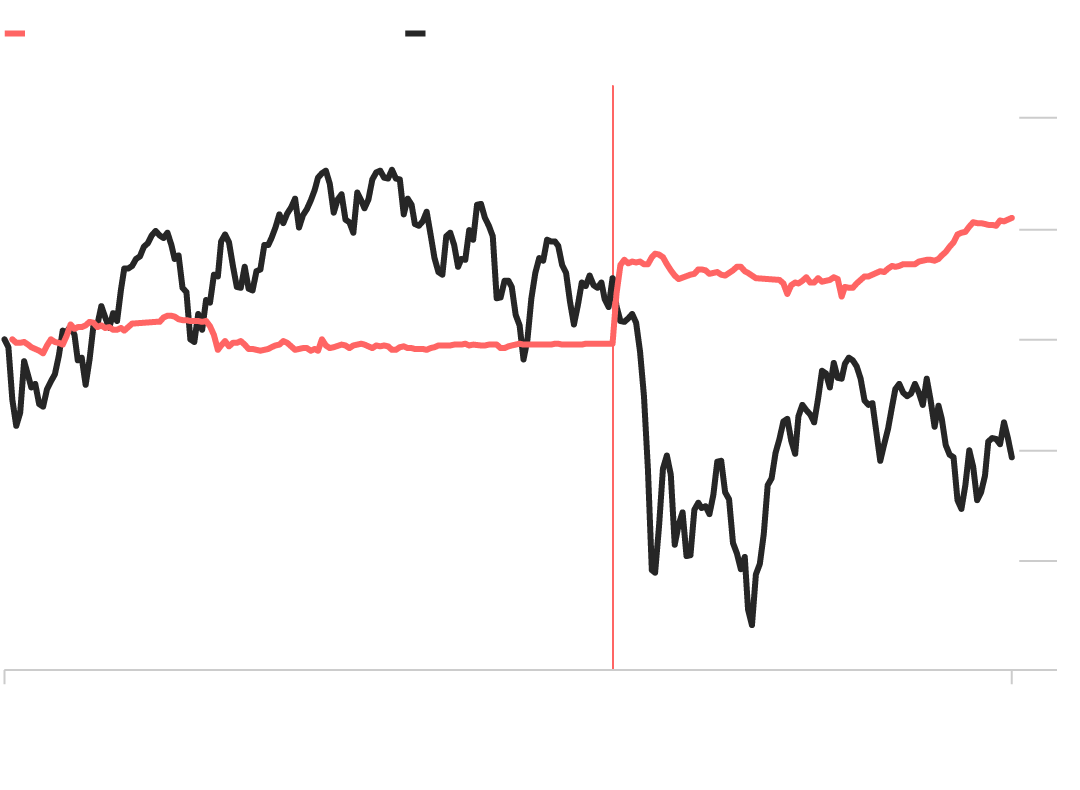

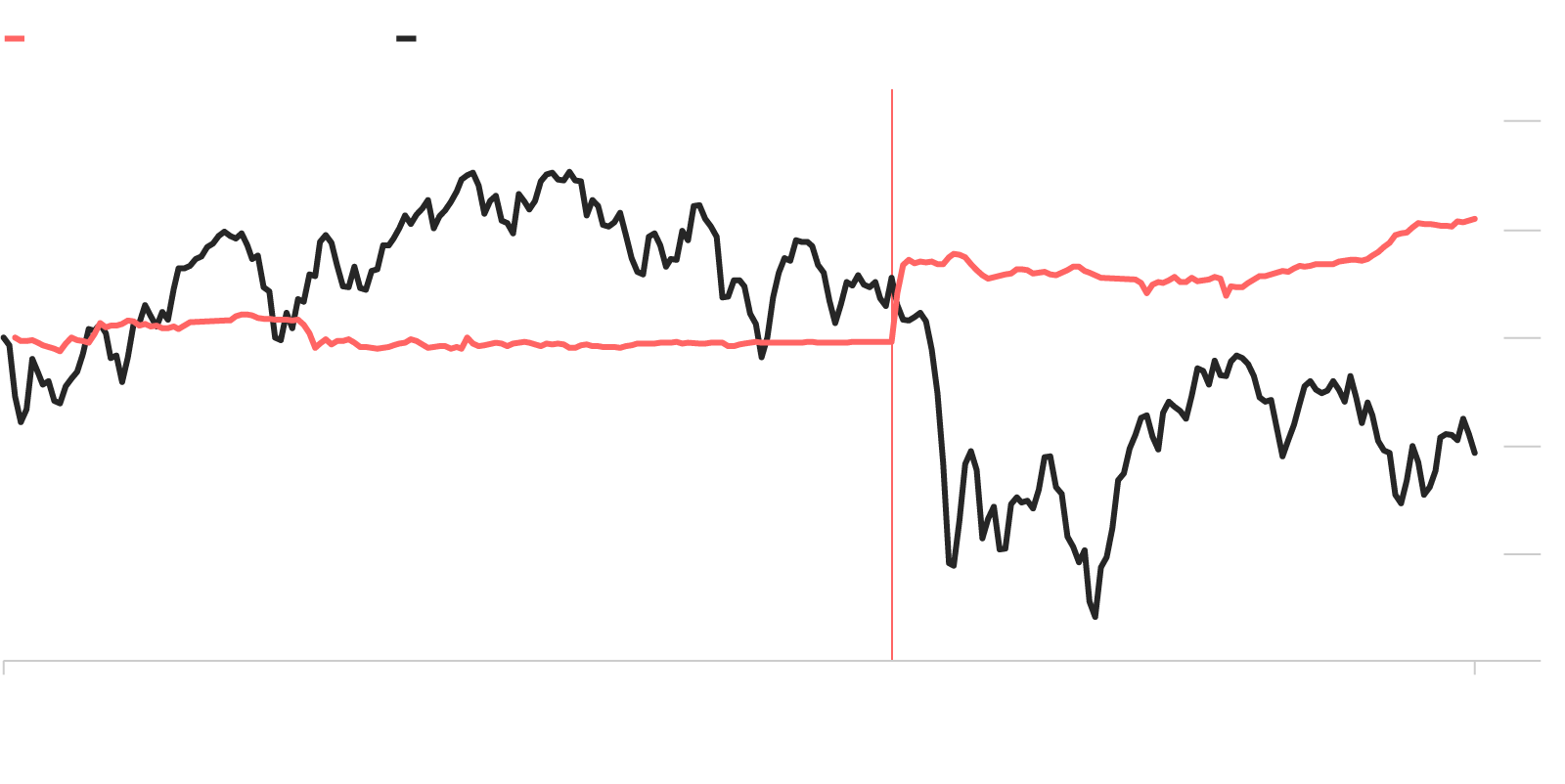

China’s capacity to influence global financial markets has been growing incrementally, but the pivotal moment came in 2015, when the yuan’s unexpected devaluation rocked assets worldwide, showing investors beyond Asia that China’s markets are a force to be reckoned with.

Yuan Devaluation

Dollar vs

Yuan (Onshore)

MSCI All-Country

World Index

China

devalues yuan

August 11, 2015

1/2015

12/2015

Note: Normalized as of 01/05/2015

Dollar vs Yuan (Onshore)

MSCI All-Country World Index

China devalues

yuan August 11, 2015

8%

4

0

–4

–8

–12

1/2015

12/2015

Note: Normalized as of 01/05/2015

Dollar vs Yuan (Onshore)

MSCI All-Country World Index

China devalues

yuan August 11, 2015

8%

4

0

–4

–8

–12

1/2015

12/2015

Note: Normalized as of 01/05/2015

The surprise move saw the yuan slide the most in two decades on Aug. 11, 2015, as Beijing sought to shore up economic growth and make China’s exports more competitive. Following on from a Chinese stock rout in mid-2015 that also had a ripple effect globally, the devaluation rattled risk assets for weeks as it was seen as an admission the economy was struggling.

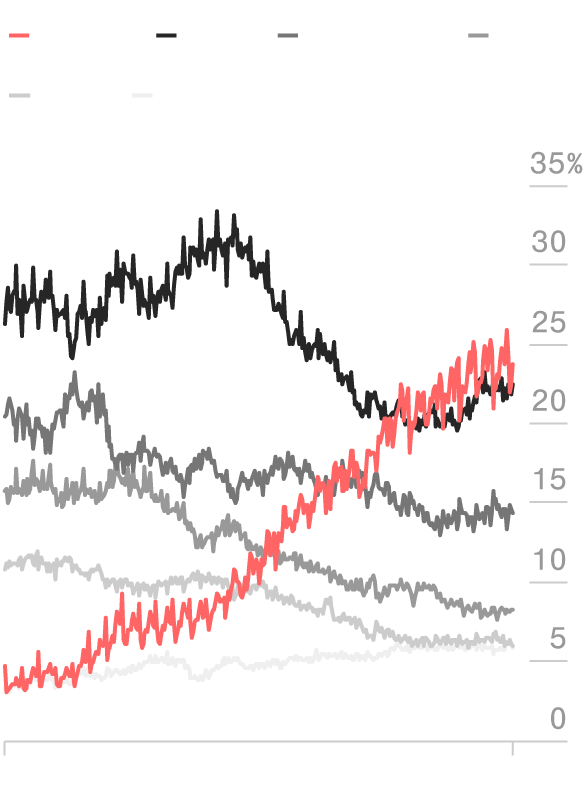

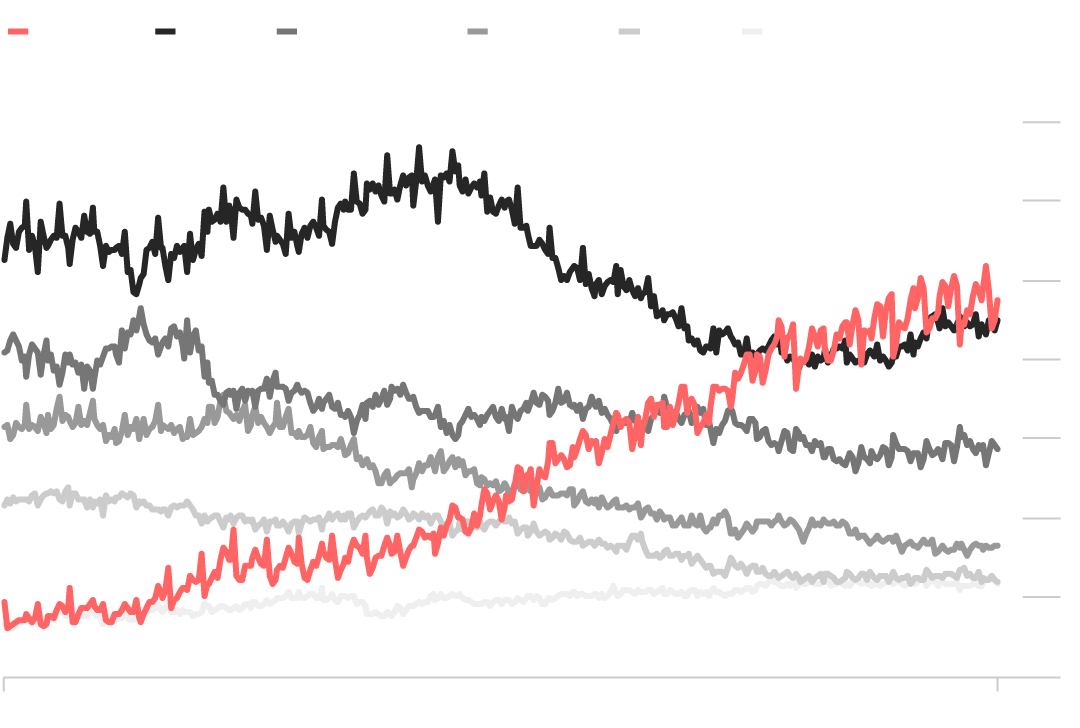

Global Clout

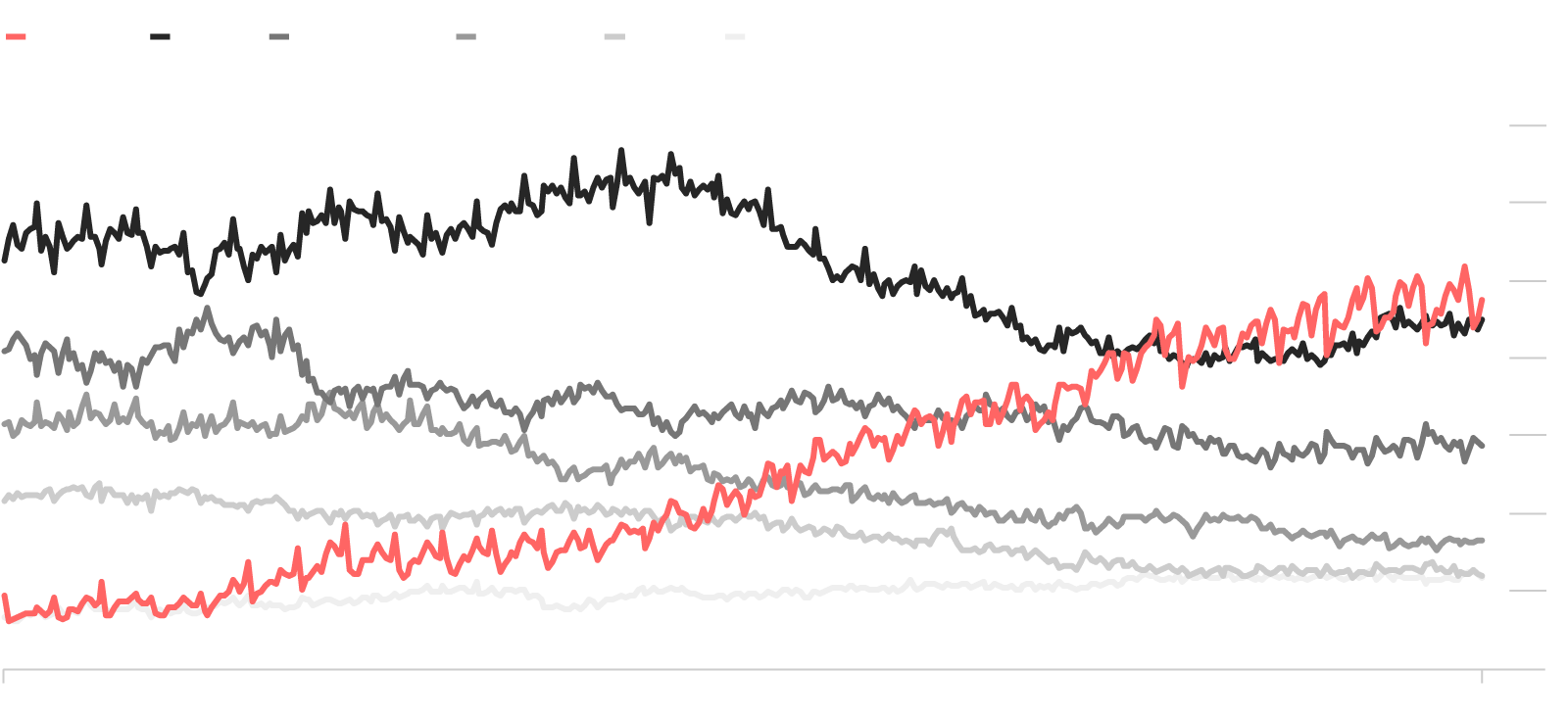

Fast forward to 2017, and China’s clout has only expanded, with its lion’s share of global trade making the managed yuan an anchor for currencies throughout Asia.

China’s Share of World Trade

U.S.

Germany

Japan

China

U.K.

South Korea

4/30/2017

12/31/1986

U.S.

Germany

Japan

U.K.

South Korea

China

35%

30

25

20

15

10

5

0

4/30/2017

12/31/1986

U.S.

Germany

Japan

U.K.

South Korea

China

35%

30

25

20

15

10

5

0

4/30/2017

12/31/1986

The nation’s status as both the world’s biggest exporter and the largest market of consumers means policy tweaks in Beijing can affect prices for everything from beef to bitcoin. Trading on Shanghai’s commodity futures market is taking on increasing influence beyond China’s borders.

The country’s pivot away from the smokestack industries that have been its growth engine for decades toward high-tech production is already shifting the global landscape for manufacturing and consumption. At the same time, China is looking to draw in more foreign capital by opening conduits to its equity and bond markets, among the largest in the world. That makes the 19th party congress, where Xi will unveil the party’s vision for China over the next five years, key for even the most peripheral of investors.

Tracking China

China has long been the world’s factory, but now that it's seeking to become the biggest shopping mall as well, the country’s sway over the global economy is becoming more obvious. Market barometers of world economic health are increasingly tracking China.

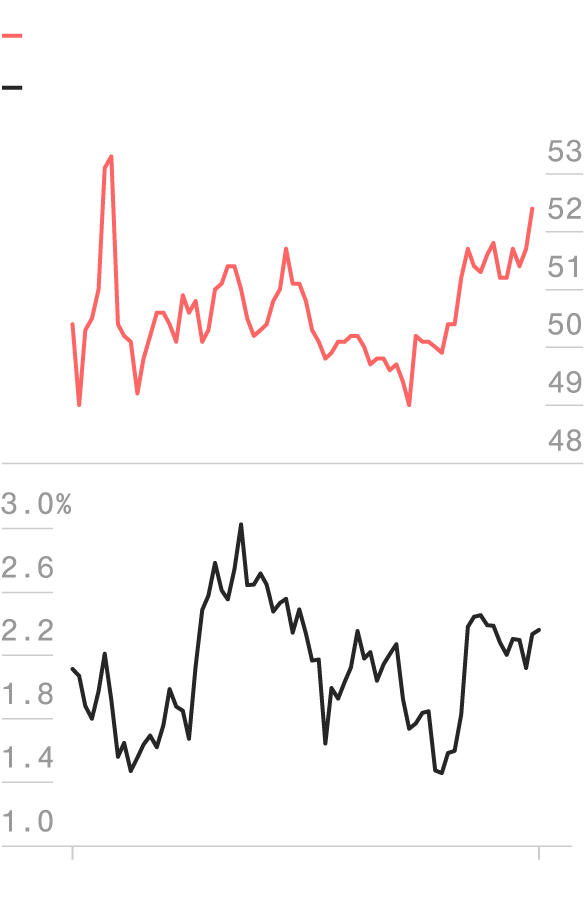

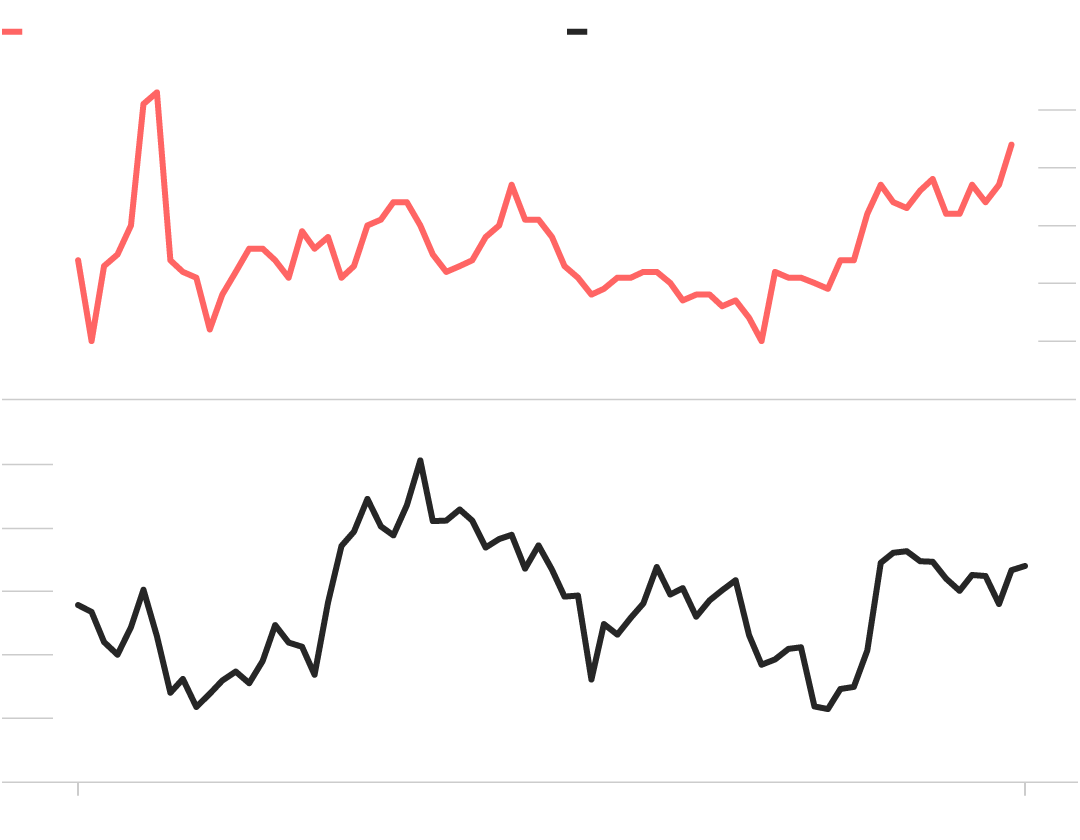

U.S. Treasuries, the go-to asset for strategists looking to assess the outlook for global growth, have been moving in line with China’s PMI (Purchasing Managers’ Index)—a gauge of sentiment in the manufacturing sector—for some time.

Treasuries Track China Manufacturing

China Manufacturing PMI (index level)

10-year Treasury yields (%)

10/10/2017

01/31/2012

10-year Treasury yields (%)

China Manufacturing PMI (index level)

53

52

51

50

49

48

3.0%

2.6

2.2

1.8

1.4

1.0

10/10/2017

01/31/2012

10-year Treasury yields (%)

China Manufacturing PMI (index level)

53

52

51

50

49

48

3.0%

2.6

2.2

1.8

1.4

1.0

10/10/2017

01/31/2012

And in an era where inflation globally has been stuck in a rut, moves in China’s factory-gate prices have become a major driver for world cost trends. That’s feeding into policy settings, risk appetite and investor animal spirits worldwide.

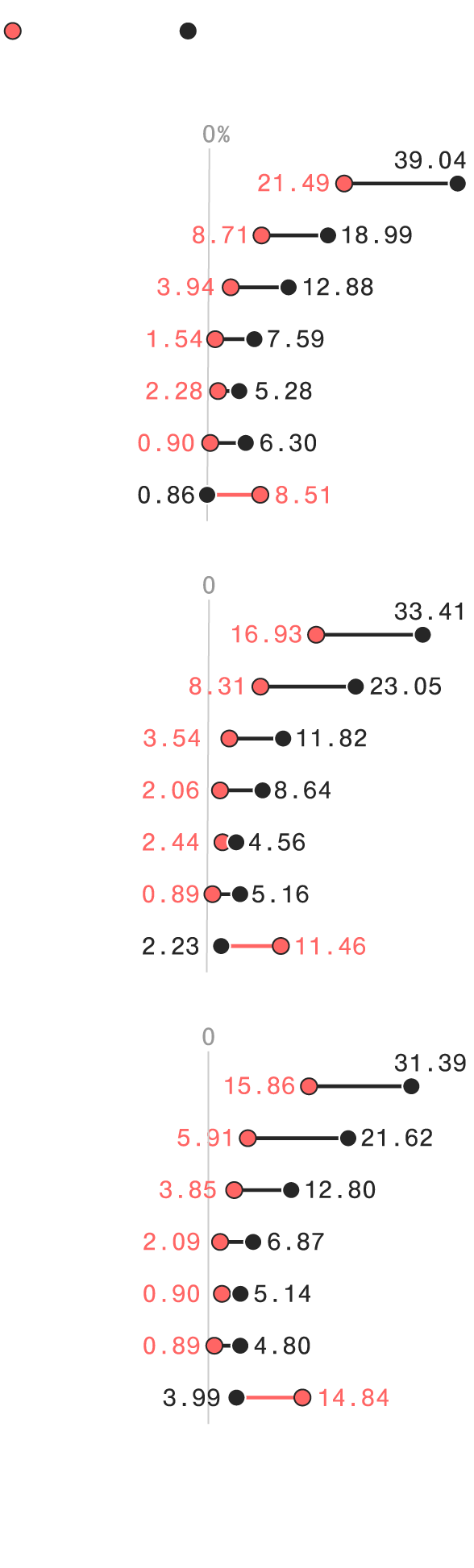

Mindful of the gap between China’s economic heft and the influence of its markets, authorities are targeting “increased convertibility” of the yuan by 2020 and have pursued its internationalization. The yuan’s share of global currency markets has almost doubled since 2010 as new trading centers opened and it is increasingly used in deals.

The Yuan in Global Markets

GDP as

% of World

% of all

transactions

2010

Europe

Japan

U.K.

Australia

Canada

Switzerland

China

2013

Europe

Japan

U.K.

Australia

Canada

Switzerland

China

2016

Europe

Japan

U.K.

Australia

Canada

Switzerland

China

NOTE: The data above excludes the U.S. dollar because, as the world’s reserve

currency, it is used in the overwhelming majority of all transactions, at 88%.

GDP as % of World

% of all transactions

2010

2013

0%

0

Europe

21.49

39.04

16.93

33.41

Japan

8.71

18.99

8.31

23.05

U.K.

3.94

12.88

3.54

11.82

Australia

1.54

7.59

2.06

8.64

Canada

2.28

5.28

2.44

4.56

Switzerland

0.90

6.30

0.89

5.16

China

0.86

8.51

2.23

11.46

2016

0

Europe

15.86

31.39

Japan

5.91

21.62

U.K.

3.85

12.80

Australia

2.09

6.87

Canada

0.90

5.14

Switzerland

0.89

4.80

China

3.99

14.84

NOTE: The data above excludes the U.S. dollar because,

as the world’s reserve currency, it is used in the overwhelming majority

of all transactions, at 88%.

GDP as % of World

% of all transactions

2010

2013

2016

0%

0

0

Europe

21.49

39.04

16.93

33.41

15.86

31.39

Japan

8.71

18.99

8.31

23.05

5.91

21.62

U.K.

3.94

12.88

3.54

11.82

3.85

12.80

Australia

1.54

7.59

2.06

8.64

2.09

6.87

Canada

2.28

5.28

2.44

4.56

0.90

5.14

Switzerland

0.90

6.30

0.89

5.16

0.89

4.80

China

0.86

8.51

2.23

11.46

3.99

14.84

NOTE: The data above excludes the U.S. dollar because, as the world’s reserve currency,

it is used in the overwhelming majority of all transactions, at 88%.

Beijing has also started to facilitate more access to what is the world’s second-largest stock market, notably via trading links called connects between Shanghai, Shenzhen and Hong Kong. MSCI Inc.’s decision in June to start including mainland shares in its global benchmarks was a key development as it will expose a whole new universe of investors to China’s stocks. This isn’t the only avenue for foreigners to buy Chinese shares, as a lot of companies are also listed offshore. Chinese e-commerce behemoth Alibaba Group Holding Ltd., for instance, trades on the Nasdaq.

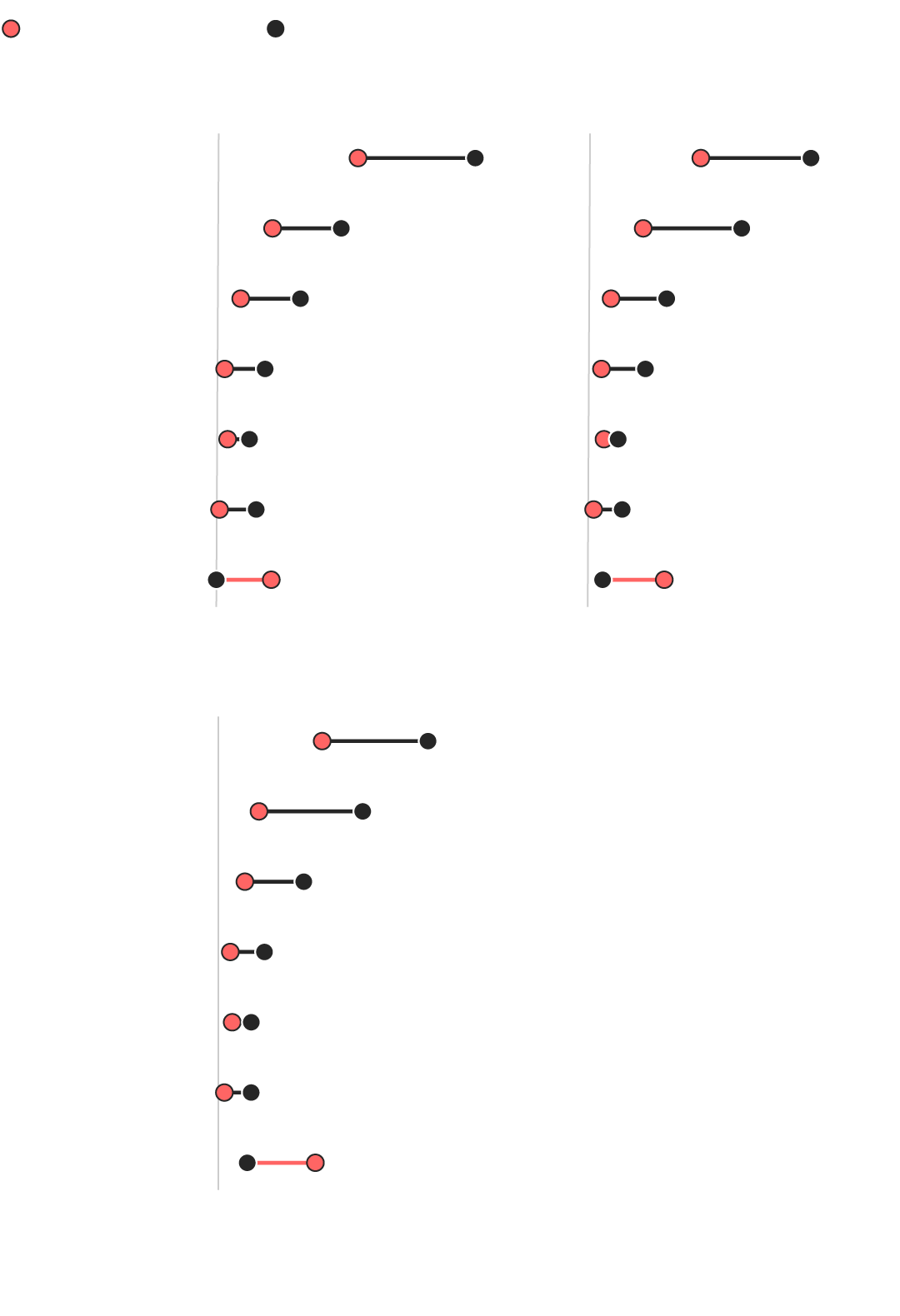

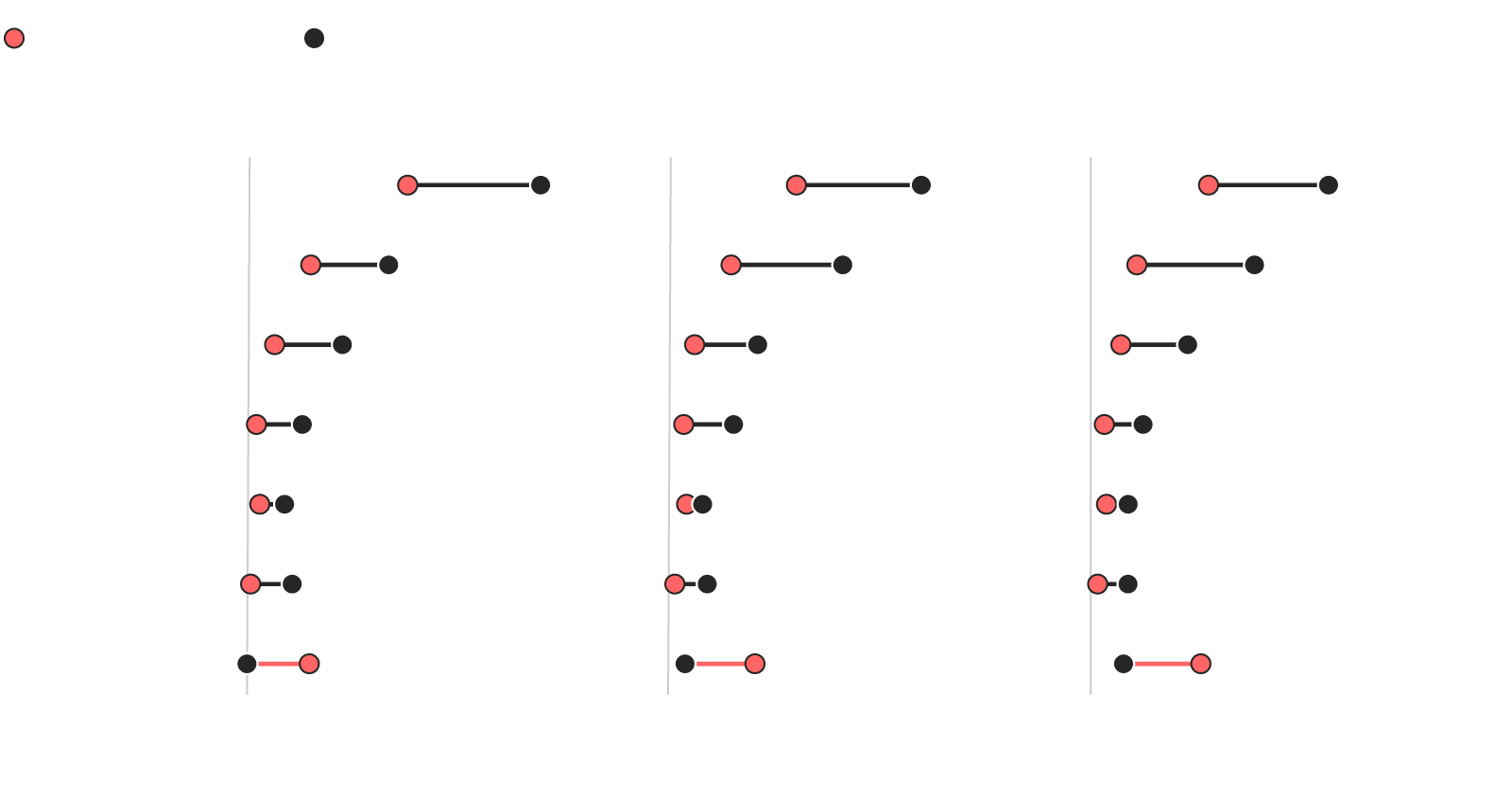

Stocks

222

222 mostly large-cap mainland Chinese stocks will be included in MSCI’s indexes starting next year, giving the mutual and pension funds that track the index compiler’s gauges access to onshore equities for the first time.

458

MSCI has said the scope of mainland

equities to be included in its indexes

may be expanded in the future to include more, mostly midcap stocks that were

overlooked in the June decision.

That could swell the universe accessible

to MSCI trackers by another 236 stocks.

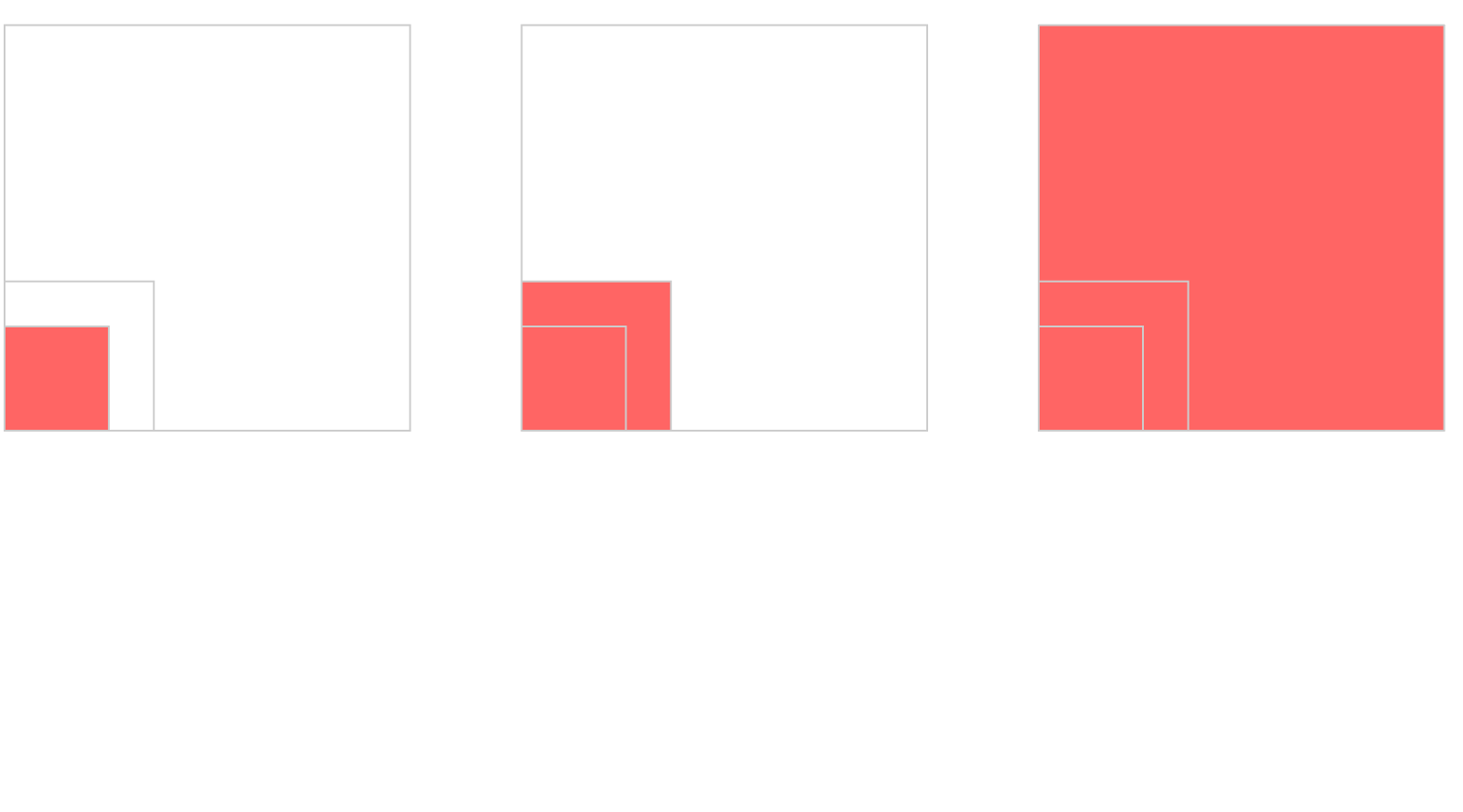

3,400+

MSCI cracking open the door to mainland equities is a key development, but China still has to address issues to do with accessibility, daily trading limits and trading suspensions if it wants more of

its mainland market, which numbers more than 3,400 stocks, to be admitted.

222

222 mostly large-cap mainland Chinese stocks will be included in MSCI’s indexes starting next year, giving the mutual and pension funds that track the index compiler’s gauges access to onshore equities for the first time.

458

MSCI has said the scope of mainland equities to be included in its indexes may be expanded in the future to include more, mostly midcap stocks that were overlooked in the June decision. That could swell the universe accessible to MSCI trackers by another 236 stocks.

3,400+

MSCI cracking open the door to mainland equities is a key development, but China still has to address issues to do with accessibility, daily trading limits and trading suspensions if it wants more of its mainland market, which numbers more than 3,400 stocks, to be admitted.

222

222 mostly large-cap mainland Chinese stocks will be included in MSCI’s indexes starting next year, giving the mutual and pension funds that track the index compiler’s gauges access to onshore equities for the first time.

3,400+

MSCI cracking open the door to mainland equities is a key development, but China still has to address issues to do with accessibility, daily trading limits and trading suspensions if it wants more of its mainland market, which numbers more than 3,400 stocks, to be admitted.

458

MSCI has said the scope of mainland equities to be included in its indexes may be expanded in the future to include more, mostly midcap stocks that were overlooked in the June decision. That could swell the universe accessible to MSCI trackers by another 236 stocks.

Likewise, China’s $11 trillion onshore bond market is being opened up, raising the potential for a big increase in overseas holdings of Chinese notes. A connect with Hong Kong was established in mid-2017 after the People’s Bank of China eased access to interbank bond trading for most investors last year.

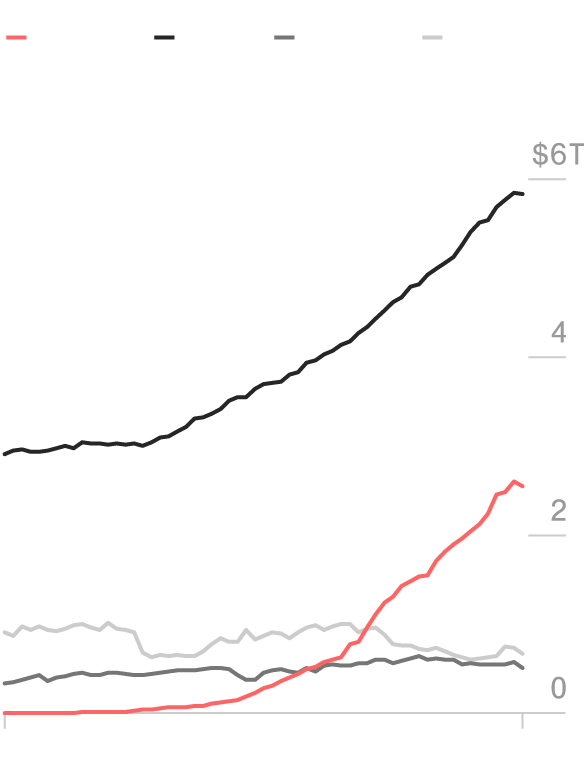

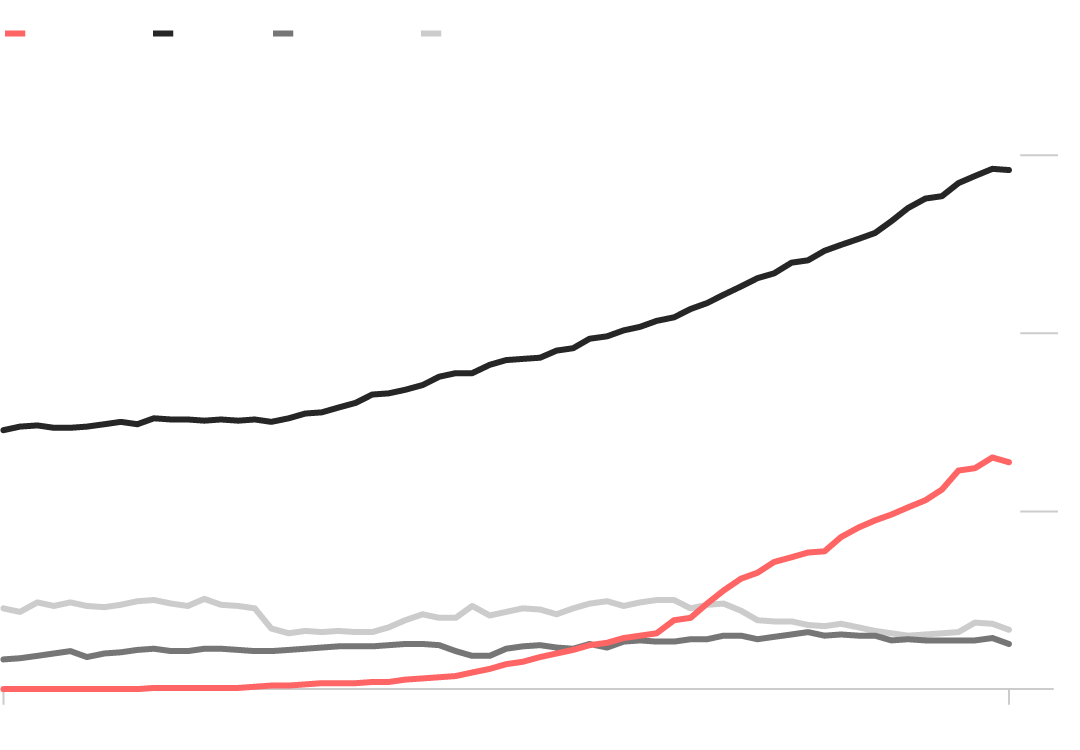

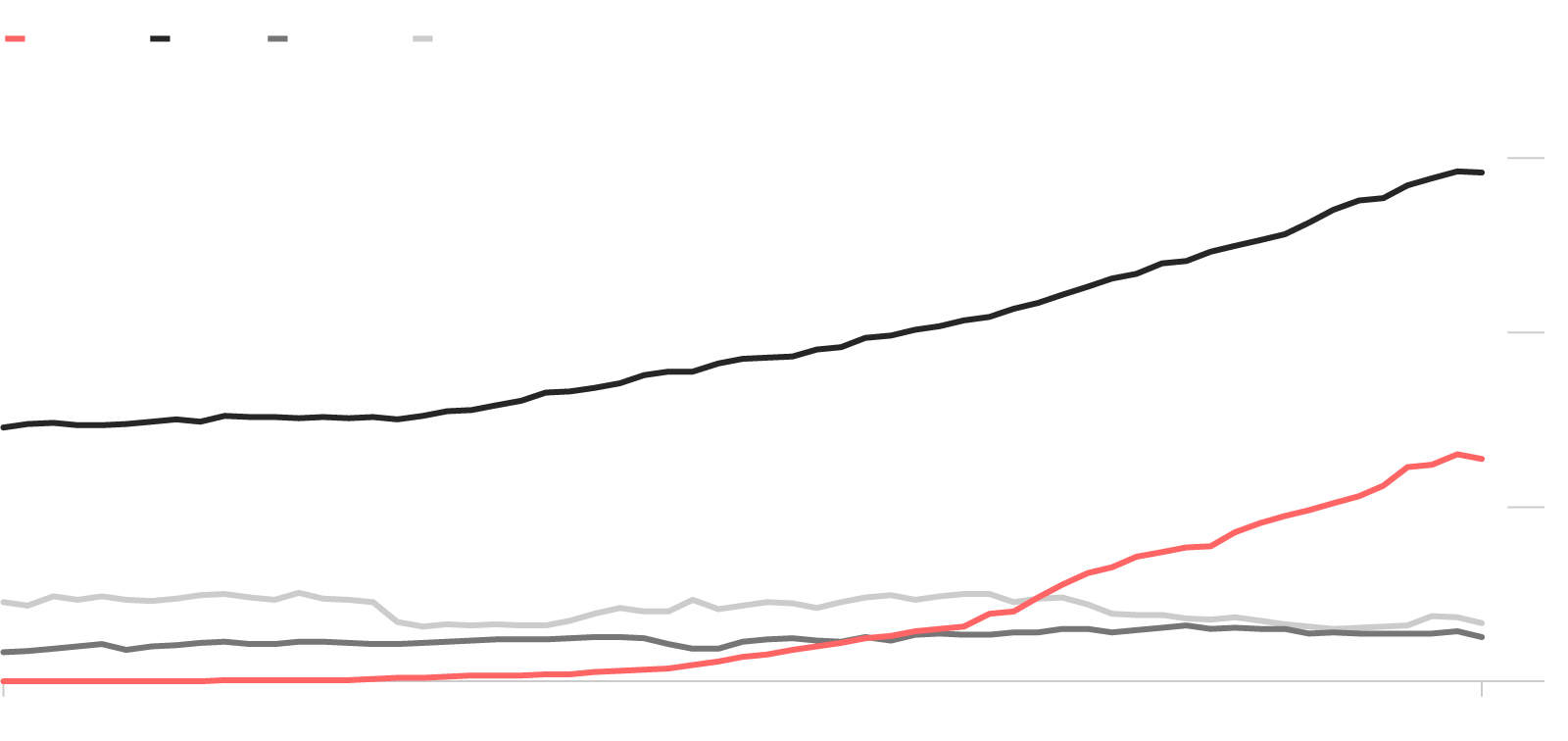

Issuance has exploded in China since the global financial crisis, when the country leveraged its way to a stable growth rate amid tumbling demand for its exports. Chinese issuers—and buyers—now dominate Asian dollar bond trading, while the market onshore is the third-biggest for debt in the world.

Non-Financial Corporate Bonds Outstanding

U.S.

Japan

U.K.

China

12/2001

12/2016

U.S.

Japan

U.K.

China

$6T

4

2

0

12/2001

12/2016

U.S.

Japan

U.K.

China

$6T

4

2

0

12/2001

12/2016

Admission to global bond benchmarks is also on the horizon—all the more reason investors may want to pay close attention to the all-important congress, due to start on Oct. 18. It’s only a matter of time before China’s mammoth local markets become global leaders in their own right.