Asia Can Power Through Another Financial Crisis

The Asian nations hit hardest 20 years ago by a crisis that sent currencies and stock markets tumbling, saw governments fall and pushed millions back into poverty, now have some of the strongest buffers in the world.

But that resilience faces a fresh test. The world’s biggest central banks are either removing monetary stimulus or mulling ways to do so—the same backdrop that helped unravel the Asian miracle a generation ago. That could suck liquidity out of emerging markets, pressure currencies and raise the cost of dollar debt repayments. The following charts assess the region’s changing fortunes:

Stronger Defenses

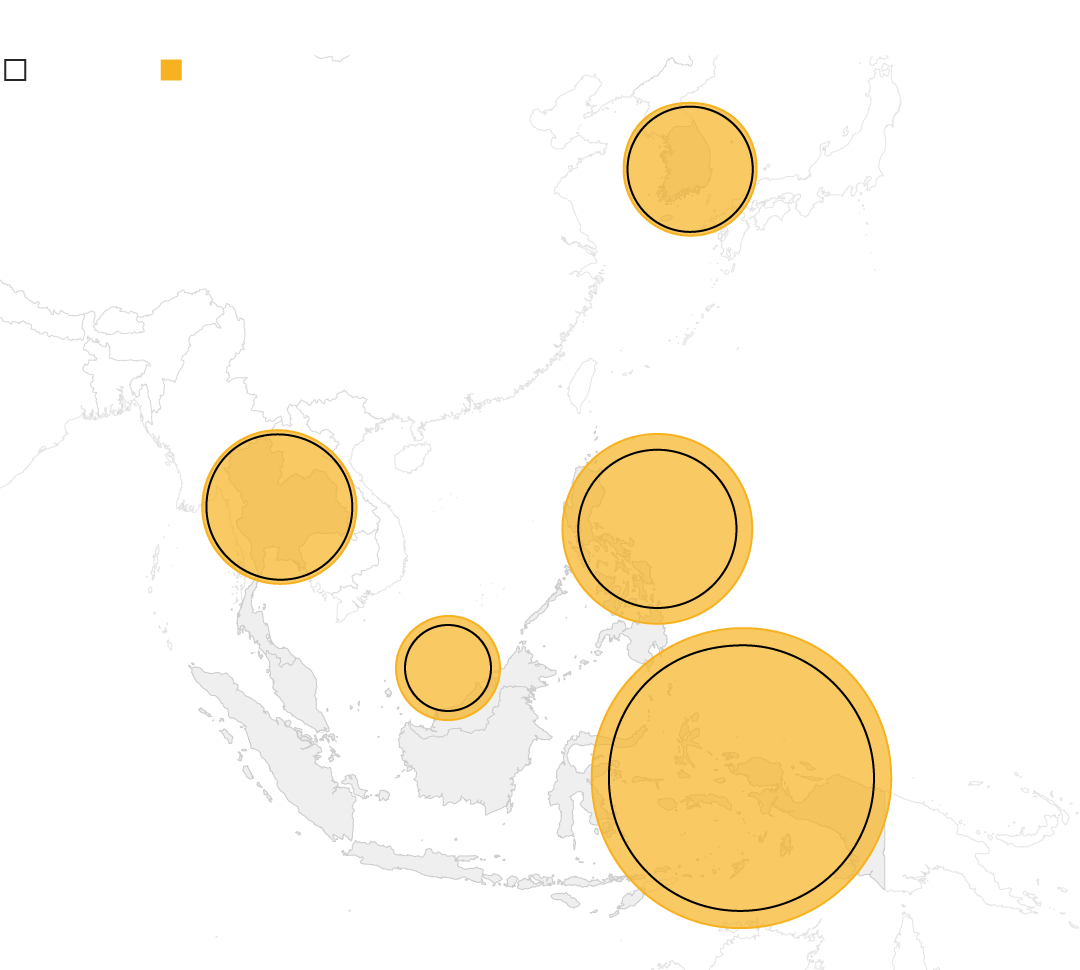

Asia’s currency reserves at well over $6 trillion make up more than half of the world’s holdings, led by China’s $3 trillion hoard. In 1996, Asia’s reserves were less than $1 trillion, leaving central banks short handed when their fixed and managed currencies came under speculative attack from investors including George Soros. Most of the countries now have floating exchange rate systems, reducing pressure on central banks to defend a particular level of the currency.

Reserves

USD billions

1996

May 2017

South Korea

Thailand

$33.2B

$38.7B

$378.5B

$184B

Malaysia

Philippines

Indonesia

$18.3B

$27B

$11.8B

$125B

$98B

$82.1B

1996

May 2017

South Korea

$33.2B

$378.5B

Thailand

$38.7B

Malaysia

$184B

$27B

Philippines

$98B

$11.8B

$82.1B

Indonesia

$18.3B

$125B

1996

May 2017

South Korea

$33.2B

$378.5B

Thailand

$38.7B

Malaysia

$184B

$27B

Philippines

$98B

$11.8B

$82.1B

Indonesia

$18.3B

$125B

Surplus Strength

Asia’s current-account positions are much stronger, with most in surplus for several years now. The current account, which measures trade and financial flows including interest and dividend payments, is used by investors to gauge a nation’s resilience to a crisis.

Current Account

1996

2016

Thailand

-8%

11.4%

South Korea

-4%

7%

Malaysia

-4.1%

2%

Philippines

-4.3%

0.2%

Indonesia

-1.8%

-2.7%

1996

2016

-8%

Thailand

11.4%

-4%

South Korea

7%

-4.1%

Malaysia

2%

-4.3%

Philippines

0.2%

-1.8%

Indonesia

-2.7%

1996

2016

-8%

Thailand

11.4%

-4%

South Korea

7%

-4.1%

Malaysia

2%

-4.3%

Philippines

0.2%

-1.8%

Indonesia

-2.7%

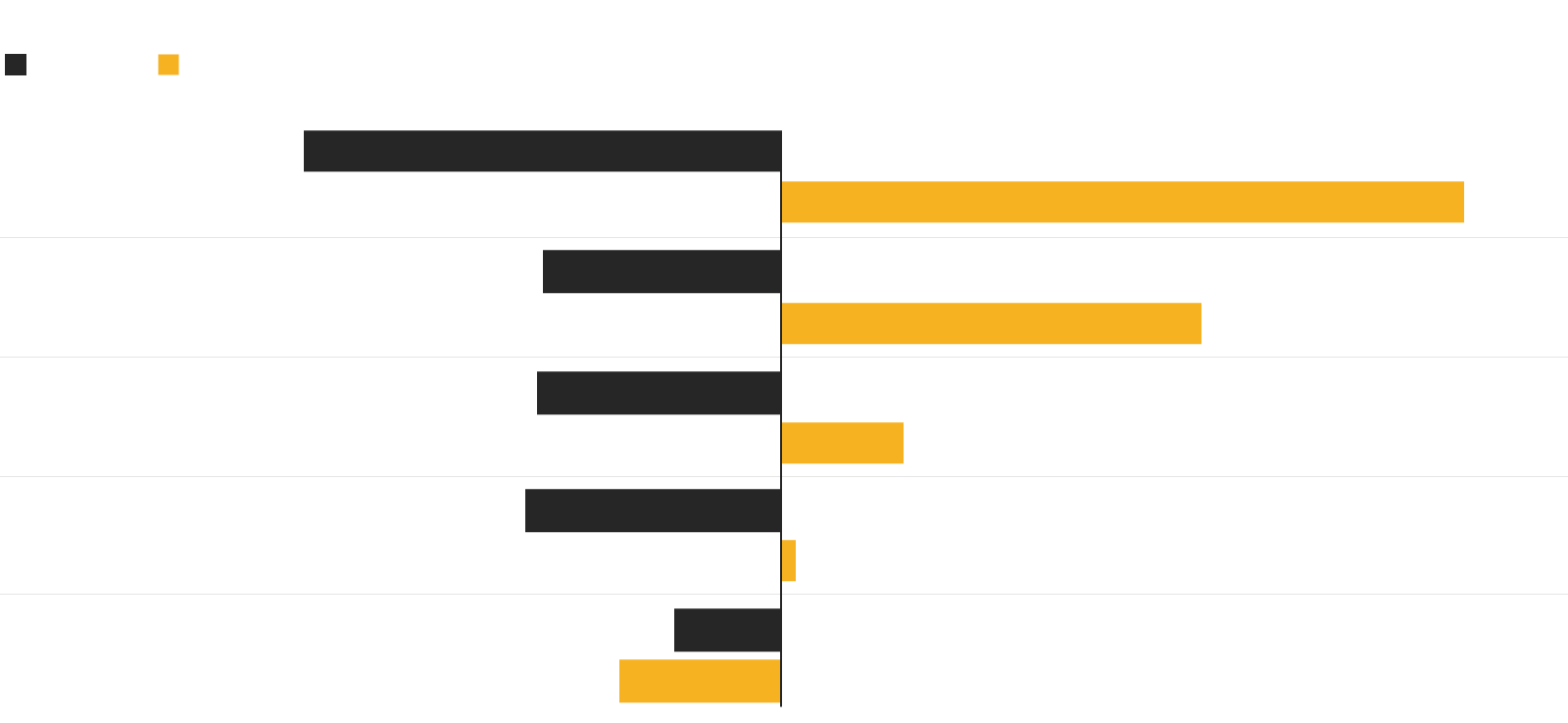

Sweet Spot

Asian economies are again among the fastest-growing in the world, with countries such as the Philippines, India and China expanding more than 6 percent annually.

GDP

USD billions

South Korea

Indonesia

$598B

$274.7B

$1,411B

$932.4B

Thailand

Philippines

Malaysia

$108.3B

$183B

$91.8B

$407B

$304.7B

$296.4B

1996

2016

South Korea

$598B

$1,411B

Philippines

$91.8B

$304.7B

Thailand

$183B

Malaysia

$407B

$108.3B

$296.4B

Indonesia

$274.7B

$932.4B

1996

2016

South Korea

$598B

$1,411B

Philippines

$91.8B

$304.7B

Thailand

$183B

Malaysia

$407B

$108.3B

$296.4B

Indonesia

$274.7B

$932.4B

Less Exposed

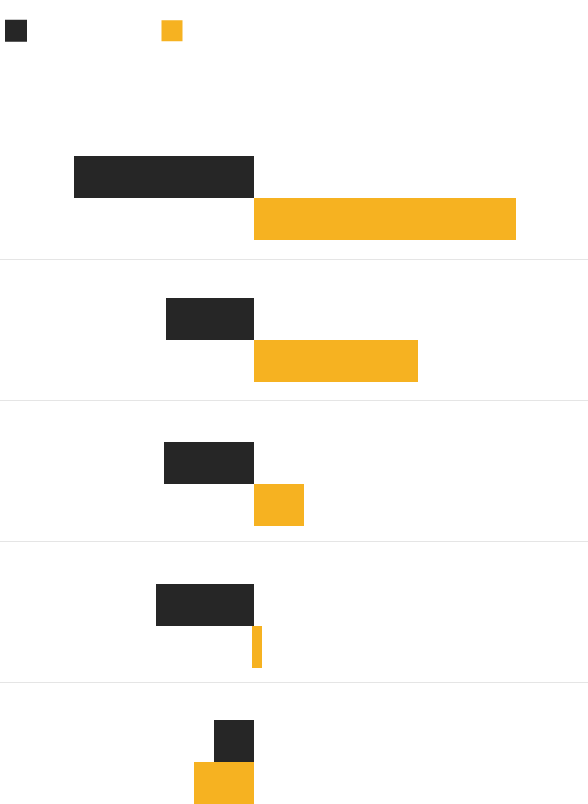

Most countries have taken steps to reduce foreign debt, making their economies less exposed should a sharp appreciation in the U.S. dollar inflate the cost of repaying loans. Twenty years ago, companies went bankrupt and governments from Thailand to South Korea were forced to seek bailouts from the International Monetary Fund when their tumbling currencies made servicing U.S. dollar loans impossible.

Foreign Debt/GNI

1996

2015

Malaysia

41.3%

66.3%

Thailand

63.3%

35.2%

Indonesia

58.3%

37%

South Korea

24%

26*%

Philippines

51.1%

22%

Note: South Korea data is from Bank of Korea

(1996, *2016); all other data are from the

World Bank (1996, 2015)

1996

2015

Malaysia

41.3%

66.3%

Thailand

63.3%

35.2%

Indonesia

58.3%

37%

South Korea

24%

26*%

Philippines

51.1%

22%

Note: South Korea data is from Bank of Korea (1996, *2016);

all other data are from the World Bank (1996, 2015)

1996

2015

41.3%

Malaysia

66.3%

63.3%

Thailand

35.2%

58.3%

Indonesia

37%

24%

South Korea

26*%

51.1%

Philippines

22%

Note: South Korea data is from Bank of Korea (1996, *2016); all other data are from the World Bank (1996, 2015)

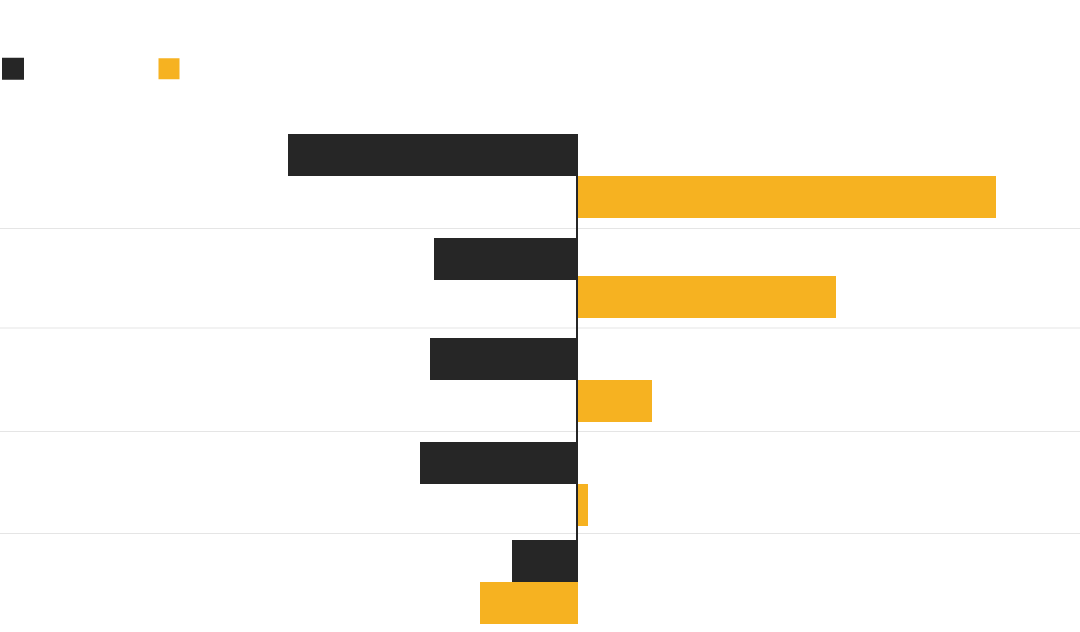

Demographic Dividend

Many of Asia’s economies have also gradually reduced their dependence on exports and become more reliant on rising consumption. Youthful populations in countries such as the Philippines and Indonesia are setting up what could be a demographic dividend if enough work can be found to swell the ranks of the middle classes there.

Population

Indonesia

Philippines

204.3M

71.7M

260.6M

104.3M

Thailand

South Korea

Malaysia

61.2M

45.3M

21.4M

68.4M

51.1M

31.4M

1996

2017

South Korea

45.3M

51.1M

Philippines

71.7M

104.3M

Thailand

61.2M

Malaysia

68.4M

21.4M

31.4M

Indonesia

204.3M

260.6M

1996

2017

South Korea

45.3M

51.1M

Philippines

71.7M

104.3M

Thailand

61.2M

68.4M

Malaysia

21.4M

31.4M

Indonesia

204.3M

260.6M

Fortunes Revived

So today, 20 years after the crisis that erupted on July 2, 1997, when Thailand abandoned its currency peg, the region is again a favorite among investors, with global funds pouring about $45 billion into stocks and bonds in Indonesia, Malaysia, the Philippines, South Korea and Thailand this year. Analysts predict that the Indonesian rupiah, Philippine peso, and Malaysian ringgit will be the top-performing currencies, including interest income, in Asia by the end of 2018.

Currencies

Forecasted total return through end of Q4 2018

Indonesian rupiah

10.04%

Philippine peso

8.64%

Malaysian ringgit

7.64%

South Korean won

0.56%

Thai baht

0.05%

Indonesian rupiah

10.04%

Philippine peso

8.64%

Malaysian ringgit

7.64%

South Korean won

0.56%

Thai baht

0.05%

Indonesian rupiah

10.04%

Philippine peso

8.64%

Malaysian ringgit

7.64%

South Korean won

0.56%

Thai baht

0.05%

“Asia has come a long way because of the lessons they learned,” said Tsutomu Soma, general manager of the fixed-income department in Tokyo at SBI Securities Co. “The region paid a huge price for those lessons but has moved on to improve drastically.”

Correction: A previous version of this graphic incorrectly indicated Thailand's GDP in 1996 as $138B; in fact it was $183B.