The Fed’s Past Crises Hold Secrets to Tackling Future Recessions

The US central bank has made mistakes before and learned from the experience. Now it must do so again

Bad news: The Federal Reserve has lost control of inflation, and the cost of bringing it back on target may well be a recession. Worse news: Whenever the next really serious downturn hits, the Fed won’t have adequate tools to fight it.

That one-two punch risks blowing a giant hole in the Fed’s credibility. What, the American public might reasonably ask, is the point of a central bank that allows the inflation rate to reach 9%, and then also can’t protect jobs?

In the 1930s and 1970s, the Fed lost its way, and the economy went off the rails. Those experiences demonstrated that without an effective central bank, the US economy suffers, sometimes grievously.

Within that experience is a reason for hope: The Fed’s history since its creation more than a century ago reveals an institution that often gets it wrong—sometimes disastrously—but also learns from its mistakes and adapts to new paradigms. Now, before the next serious downturn, the Fed must do so again.

First, that means bringing inflation under control and trying to limit any associated downturn in the economy. Next, it requires working with Congress and the Treasury to put in place arrangements so that once the US economy is back in balance, a serious crisis will be less likely to occur—and less severe when it does.

Fighting inflation isn’t a team sport. Staving off the next major recession will be.

•••

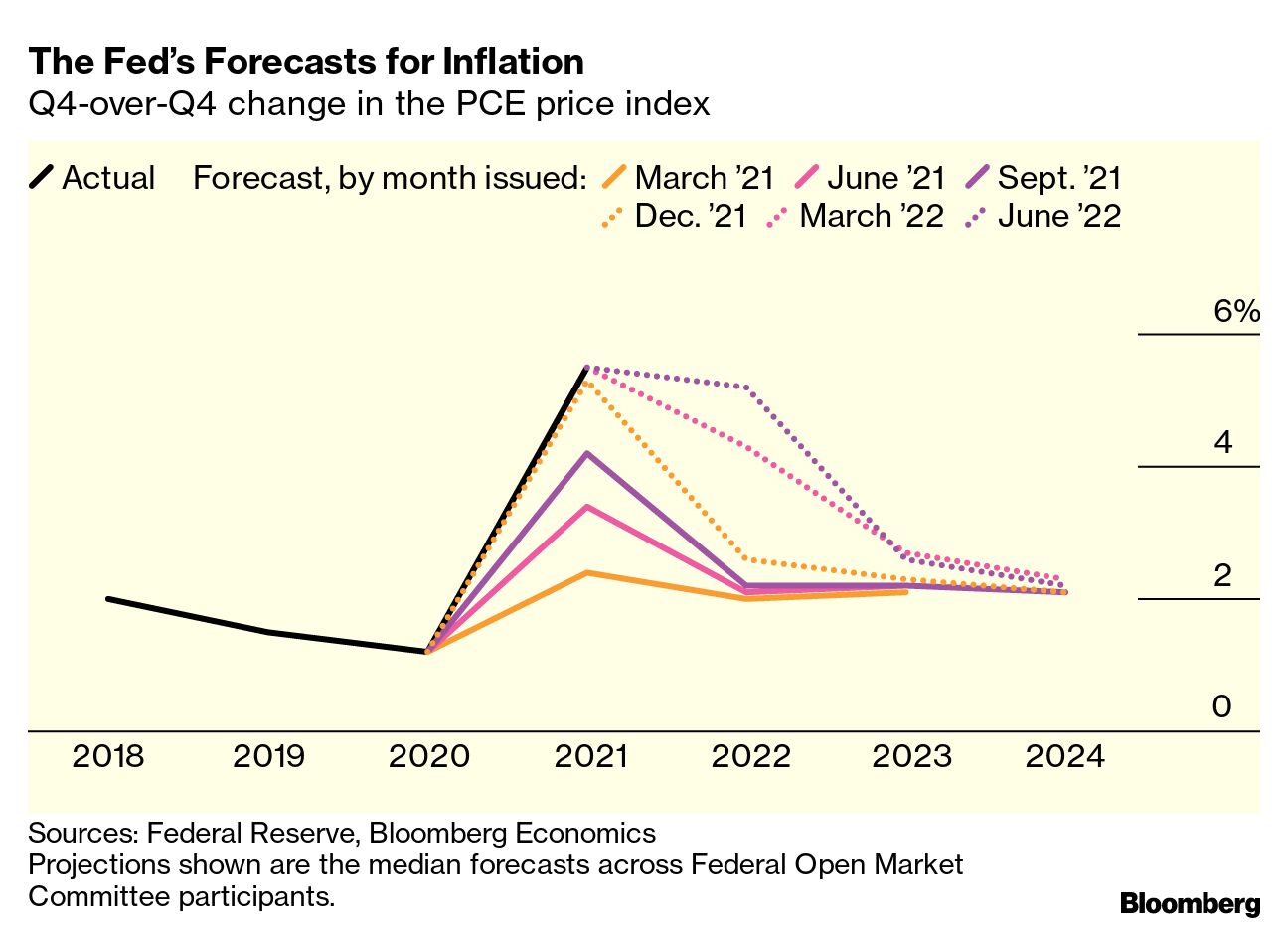

Inflation, measured by the Fed’s preferred gauge—the personal consumption expenditures price index, or PCE—was running close to 7% in June. That’s more than triple the central bank’s 2% target. With prices for everything from gasoline to groceries having risen at a torrid pace over the past 12 months, Bloomberg Economics calculates that the average US household faces an inflation tax for 2022 of more than $5,200.

The Fed’s Forecasts for Inflation

Q4-over-Q4 change in the PCE price index

Adding to the stress, growth is stalling. The Fed’s goal is to engineer the fabled soft landing—bringing down inflation without crashing the economy. At all costs, though, it cannot allow an inflationary psychology to take hold, permitting outsize wage and price increases to become a self-fulfilling prophecy. That could provide the crucial ingredient for an even more toxic situation: stagflation.

In the 1970s, Fed Chair Arthur Burns allowed inflation to run too high for too long, leading to the classic case of stagflation. In 1979, the year after he stepped down, he gave a speech in Belgrade, “The Anguish of Central Banking,” claiming that society was unwilling to accept the pain necessary to stifle inflation—making it impossible for the Fed to do its job.

One person in the audience was determined to prove Burns wrong. Paul Volcker, less than two months in office as Fed chair, raced back to Washington. Six days later he unveiled a radical policy shift that would ultimately raise benchmark interest rates to almost 20%, wringing runaway inflation—and inflation expectations—out of the system.

The cost of the Volcker shock was a deep recession, with millions thrown into unemployment. The benefit was decades of steady growth and low inflation, a period that economists now call the Great Moderation. Volcker gave a valedictory speech, “The Triumph of Central Banking?,” in 1990.

Today, with the highest inflation since the early 1980s, Fed Chair Jerome Powell also faces painful trade-offs. So far, after initially failing to recognize the extent of the problem, his response is closer to Volcker’s vigor than Burns’s anguished inaction.

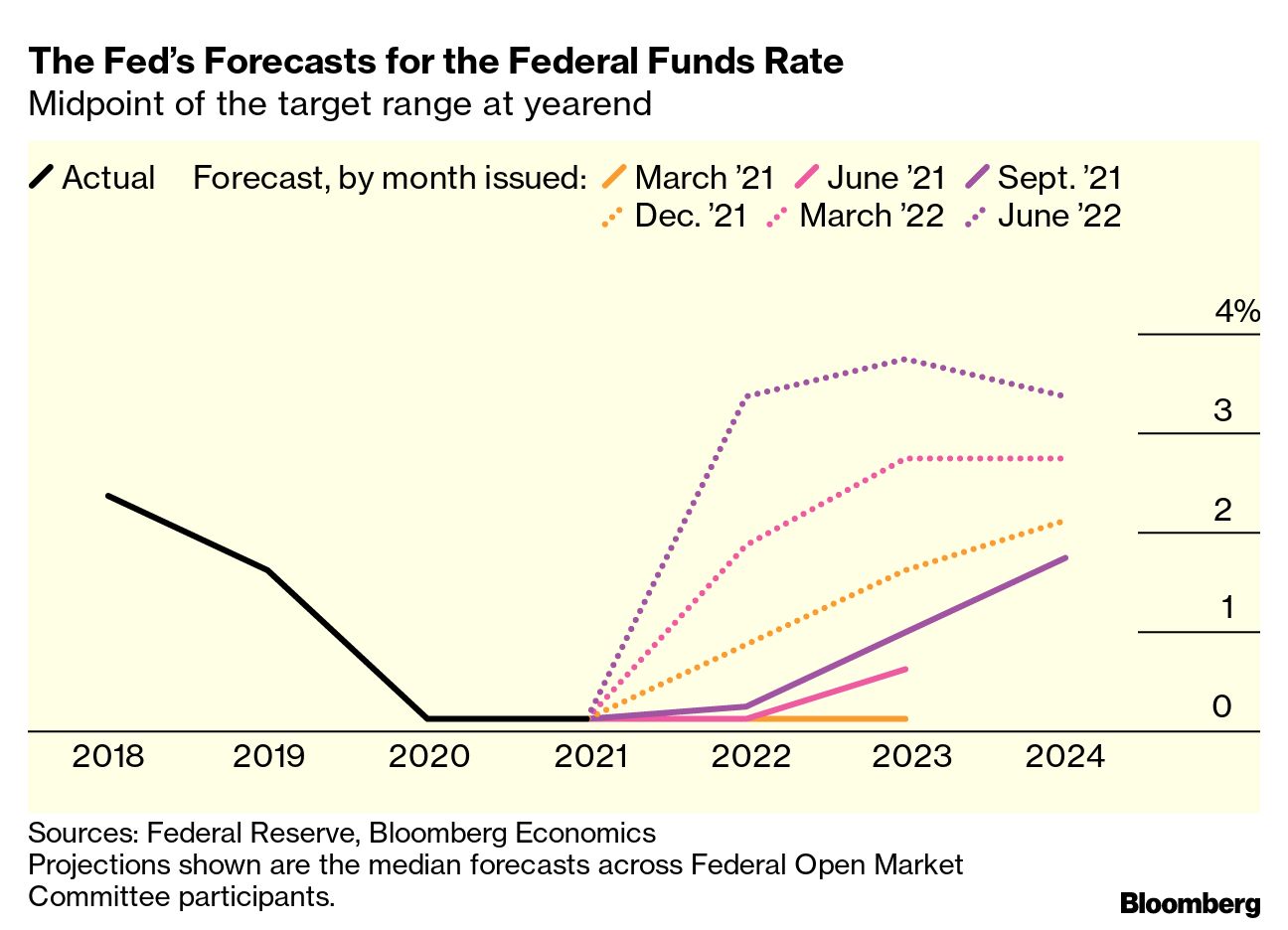

Under Powell’s leadership, the Federal Open Market Committee has lifted the federal funds rate from 0.25% at the start of the year to 2.5% in July. With rapid wage gains threatening to propel prices higher, there is substantially more to do. Neel Kashkari, one of the FOMC’s most dovish members, says he expects the funds rate to reach 4.4% by the end of 2023. Bloomberg Economics sees it hitting 5%.

The markets don’t really believe it yet. Indeed, investors’ confidence that rates won’t go that high sparked a rally in the S&P 500 from a trough in mid-June. Buoyant markets—by boosting confidence and wealth—actually make it harder for the Fed to bring inflation under control. The annual monetary policy symposium in Jackson Hole, Wyoming, later this month will be an opportunity for Powell to reset expectations.

The Fed’s Forecasts for the Federal Funds Rate

Midpoint of the target range at yearend

Even a mini-dose of Volcker’s medicine will be tough for the economy and markets to swallow. The higher interest rates required to cool demand and bring inflation back to target will certainly result in job losses and weaker growth and could well trigger a downturn. Bloomberg Economics’ model puts the chances of a recession starting before the end of 2023 at close to 100%.

Watch: Policymakers Then & Now on the Fed’s History

Bernanke on the Great Recession

Ferguson on Sept. 11

Boone on the Covid-19 Pandemic

Kohn on the 1987 Market Crash

Lowenstein on the Founding of the Bank

Rajan on the Great Recession

Ahamed on the Great Depression

Orphanides on Volcker Shock

Wong on the Pandemic Crisis

•••

Eventually, inflation will be back on target, and any immediate recession will end. At that point, once the labor market is back in balance, the federal funds rate will probably settle at about 2.5%—or at least that’s what Fed policymakers expect. That presents a significant problem.

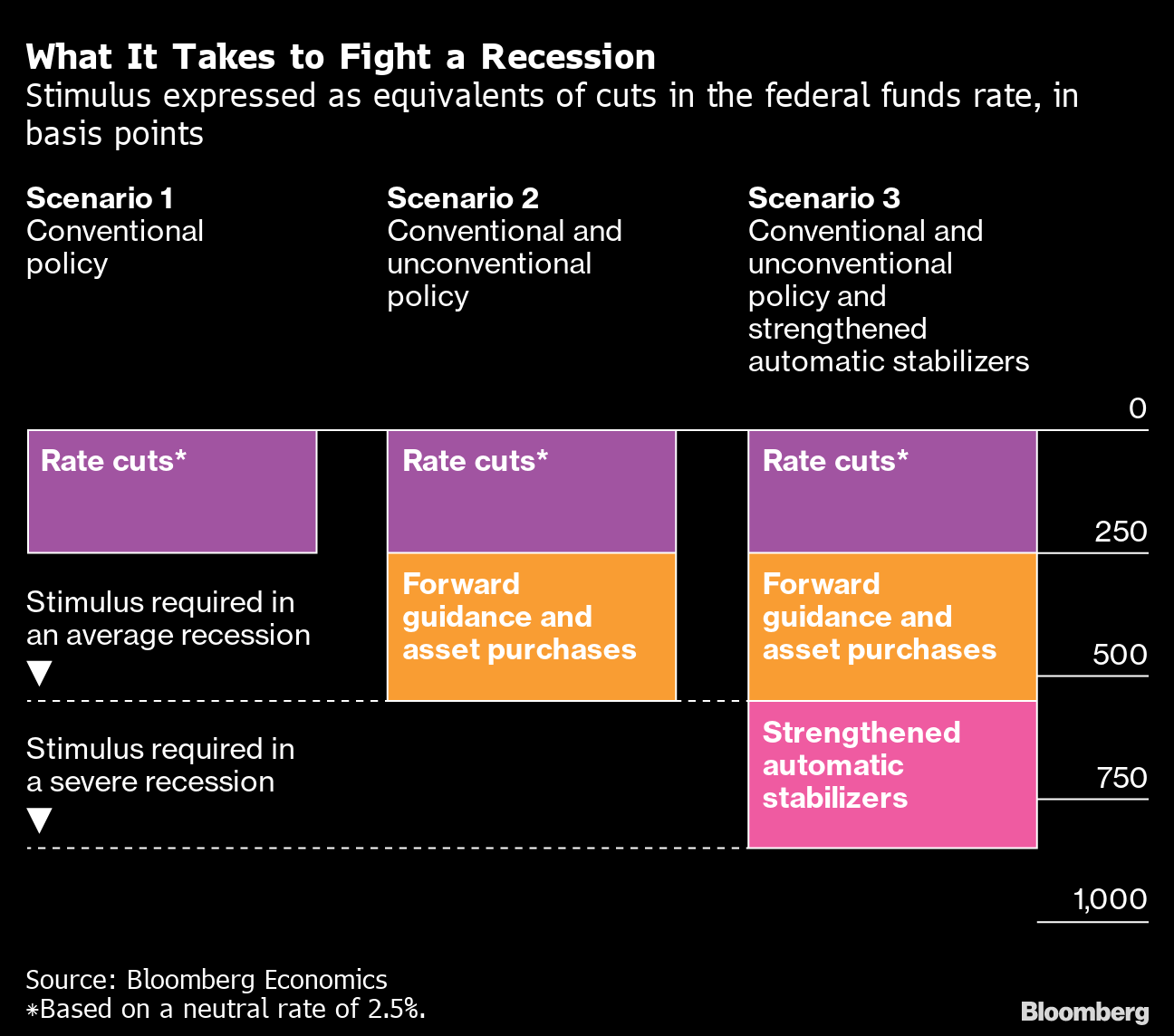

In the nine US recessions from the 1950s through 2009, the Fed cut its policy rate by an average of 550 basis points to help restore growth. That means next time around, if it relied only on its conventional policy tool—the short-term policy rate—to fight an average recession, the FOMC would be short around 300 basis points of stimulus space. Confronted with a repeat of the 2008 financial crisis or the 2020 Covid-19 collapse, the deficit would be much larger.

It wouldn’t be the first time the Fed has fallen short. In 1929, after Black Monday, the central bank failed its first big test: It allowed thousands of banks to go under and millions of workers to lose their jobs. “It is inexpedient,” the Fed’s policy committee said, “to exhaust at the present time any part of our ammunition … in a vain attempt to stem an inevitable recession.” The result was the Great Depression.

Things were different by the 2008 financial crisis. To be sure, the Fed—in its role as financial system supervisor—takes a share of the blame for missing the warning signs in the runup to the crisis. “It’s sort of a narrative capture,” says Raghuram Rajan, who, as economic counselor and director of research at the International Monetary Fund at the time, was one of the few to ring an alarm. Regulators saw top Wall Street companies such as Goldman Sachs Group Inc. as “the smartest people in the universe” and trusted their ability to manage risks, Rajan says.

But once the crisis hit, Fed Chair Ben Bernanke—a student of the Great Depression—showed he had learned from the failures of the 1930s and would use the Fed’s full range of powers to avert catastrophe.

Not only did the Fed exhaust its conventional tools—cutting the benchmark federal funds rate to 0%—but it also deployed unconventional ones. Big banks were bailed out. The Fed provided forward guidance, assuring markets that short-term rates would stay low. And it purchased bonds worth trillions of dollars to push long-term borrowing costs down as well.

Bernanke concluded that—applied aggressively—forward guidance and asset purchases could have an effect similar to cutting the federal funds rate by an extra 300 basis points. Looking forward, those tools plus conventional rate cuts add up to give the Fed about 550 basis points of stimulus power—just about enough to fight an average recession.

What It Takes to Fight a Recession

Stimulus expressed as equivalents of cuts in the federal funds rate, in basis points

But that won’t be enough for a really serious recession. The next time that happens, the economy will need more stimulus than the Fed has at its disposal. Fortunately, it’s not entirely out of options.

One of those options is to lift the inflation target to 3% from 2%, which would open up an extra 100 basis points to cut. There have also been stimulus experiments in Japan, Europe, and the UK that the Fed could try. Those include giving banks subsidies to encourage them to make more loans; paying negative interest rates—essentially charging banks a penalty—for reserves they leave with the central bank; and yield curve control, or capping the yields on government bonds of progressively longer maturities. Such steps could squeeze a few more drops of stimulus out of monetary policy.

Those options are a last resort, for good reason. Households hate inflation, which is a powerful argument against moving to a 3% target. Negative interest rates are bad for bank profits, and if the banks were to pass the penalties along to household depositors, they’d do little to bolster the Fed’s public support. Yield curve control would cause the Fed to lose control of the size of its balance sheet.

Forward guidance and asset purchases have already been criticized as exacerbating inequality and financial instability. So far the benefits for the wider economy have clearly outweighed the costs. But if the Fed decides to take its experimentation further, the costs could be formidable.

•••

There are limits to what monetary policy can do on its own. But when monetary policymakers act in concert with a fiscal policy, that can be a game changer.

In 1942, soon after the US entered World War II, the Fed agreed to cap Treasury borrowing costs to ensure that wartime spending could be financed at an affordable price. That cooperation went on too long—until 1951, well into the Korean War—and limited the Fed’s ability to fight inflation. But it also showed that monetary and fiscal policy can work together.

Delivering the proper dose of fiscal stimulus isn’t easy. Critics have widely panned the US fiscal response to the 2008 financial crisis and ensuing Great Recession as having done too little, with the government pulling back too quickly. In the Covid crisis, the opposite happened. With the Democratic Party in control of both houses and the White House, Congress passed, and President Joe Biden signed, a $1.9 trillion stimulus package in early 2021. That put a rocket under the recovery, but it supercharged inflation as well.

One solution could be to strengthen what economists call automatic stabilizers: rules that increase government spending and reduce revenue whenever the economy weakens, without the need for Congress to act in the moment.

“In countries where there is a tradition of automatic stabilizers, fiscal policy was quite well calibrated” during the Covid crisis, Laurence Boone said in an interview when she was still chief economist of the Organization for Economic Cooperation and Development. (She’s now France’s secretary of state for European affairs.) “In countries where there is wider use of discretionary fiscal policy, it has been much more difficult to calibrate the support.”

In a future crisis, a smarter version of Fed-Treasury collaboration might be the least bad way of filling any hole in monetary policy. Here’s one proposal:

1. The Fed takes its policy rate to 0% and informs Congress that it expects the rate to remain on the floor for at least a year. In addition, the Fed begins asset purchases—buying bonds in the markets—to lower longer-term rates.

2. Upon receiving the Fed’s notification, the Treasury begins mailing out monthly checks to households—perhaps $100 per adult and $50 per child for everyone below a certain income threshold.

3. The payments continue every month until the unemployment rate is at or below 6%, which would put it about 2 percentage points above most economists’ estimates for the sustainable level of unemployment.

The economics make sense. Sending funds directly to the lowest 80% or so of households by income would be good for growth and equality. And right-sizing fiscal stimulus–in this case by tying the delivery of checks to the unemployment rate–would help prevent the overshooting seen in the Covid relief effort. The line between monetary and fiscal policy, crucial for maintaining Fed independence, would be preserved.

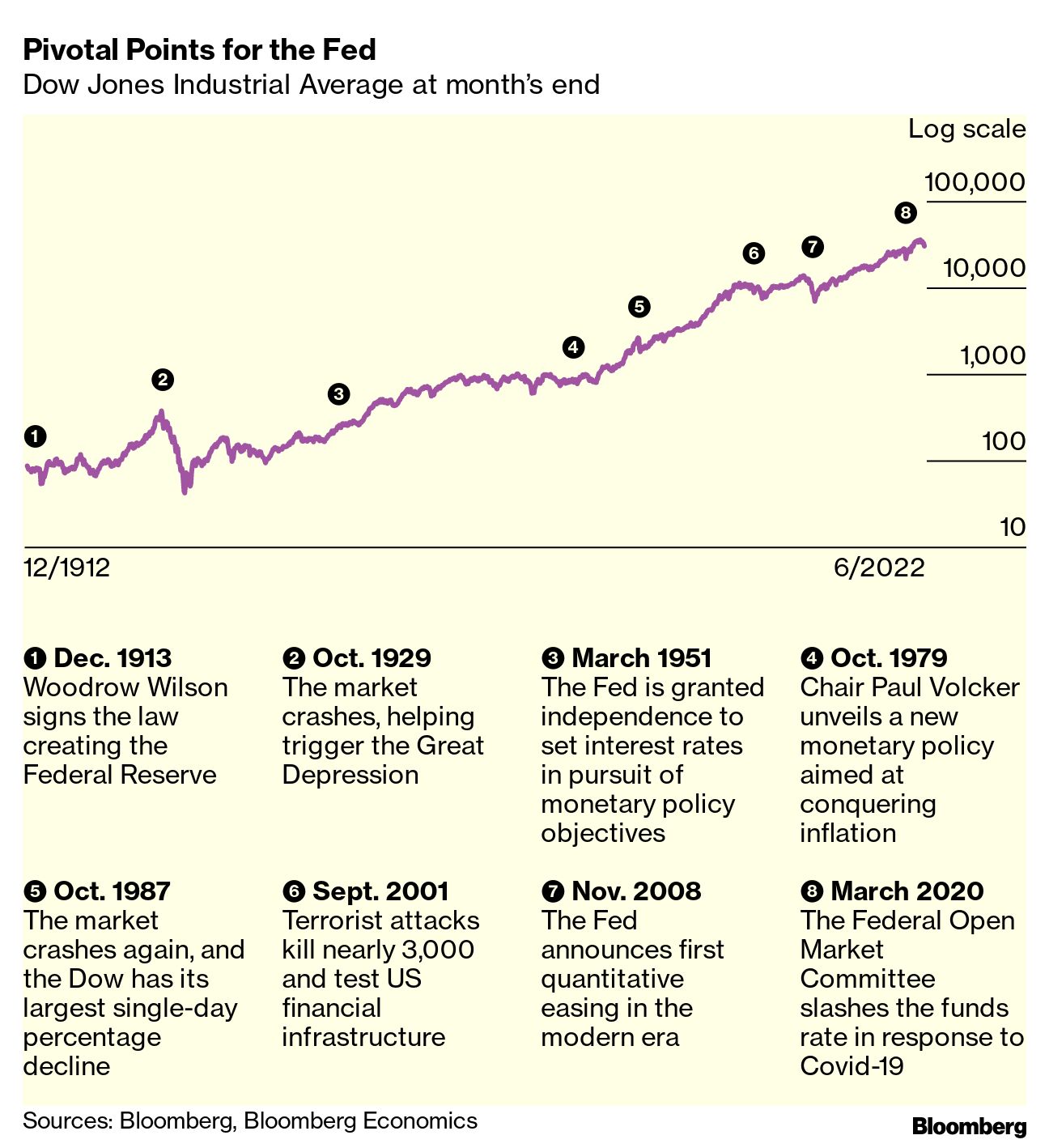

Pivotal Points for the Fed

Dow Jones Industrial Average at month’s end

But the politics would be difficult. No politician wants to give up his or her discretion to decide how much money to dole out to voters—or when to do so.

It’s possible to imagine more extreme solutions. Modern Monetary Theory, for example, would give Congress the primary responsibility for managing growth and inflation, with the Fed back to capping borrowing costs as in World War II. In Bernanke’s view, the costs of that approach would far outweigh the benefits. “With the best will in the world,” he says, “I am not sure the fiscal authorities have either the knowledge or the ability to move in a quick and sensitive manner” to control inflation.

It’s also possible to imagine that the Fed will face a very different environment in the years ahead. De-globalization, aging populations, and the fight against climate change could shift the balance in the economy and require a higher federal funds rate to keep inflation in check. That would make it harder for the US economy to grow, but also give the Fed more space to cut rates when recessions hit. That’s an intriguing possibility. For now, though, it’s not one that the Fed—or the markets—are betting on.

•••

There’s a related challenge that also demands careful attention: how to provide the economy with the low borrowing costs needed to spur growth without fueling speculative bubbles in financial markets.

“We have a conflict between the monetary policy we need for domestic economic activity—inflation and unemployment—and the monetary policy we need for financial stability goals,” says Liaquat Ahamed, the author of Lords of Finance: The Bankers Who Broke the World, the Pulitzer Prize-winning book on the policy mistakes that led to the Great Depression.

As the collapse in the value of cryptocurrencies and other speculative assets in the face of Fed tightening demonstrates, the threat to stability is real. Plugging the gaps in financial regulation, in particular by expanding oversight of the so-called shadow banking system, would help guard against future crises and take some of the pressure off the Fed.

•••

First, the Fed must control inflation—even at the expense of a recession. Then it’s essential to rethink fiscal stimulus, financial regulation, and the Fed’s tool kit. None of the options is easy. Still, the choice is between a US economy where the Fed has credibility as an inflation fighter and—working with Congress—the tools to fight recessions, and one where it does not.

The right path is obvious. The hopeful message from 109 years of Fed history is this: The failures of the current crisis might galvanize the political will to take it.

Orlik and Wilcox are economists for Bloomberg Economics in Washington.