Five Traders Tell Us How to Survive a World of Disrupted Markets

Trading requires constant vigilance and the ability to adapt and profit from disruptions. But what happens when the act of trading itself is disrupted? To get a glimpse of the life of a trader in 2021, Bloomberg Markets asked five reporters—Justina Lee in London, Divya Balji in Toronto, Liz Capo McCormick and Sonali Basak in New York, and Rebecca Choong Wilkins in Hong Kong—to interview traders. They quizzed them about how they got into the business, what their typical day is like, how their market and investing strategy is changing, and what advice they’d give to budding traders. All are grappling with the Covid‑19 pandemic, the rise of new asset classes and technologies, the unprecedented flood of money from the world’s central banks, and the age-old challenge of keeping their emotions in check. The interviews, conducted in late August and early September, have been edited and condensed for clarity.

Jump to

THE CRYPTO TRADER

Interview by Justina Lee

OLIVER CHALK, 20

Sydney

Co-founder, Proxima Capital

Assets Under Management: $38.5 million

Early Days

I was always, as a kid, interested in trading. I thought it was the funnest way to make money, right? Just click on things and push buttons, and then out prints money or big losses. I would do stuff like buying lollies from the local store and sell them at my sister’s netball games. And that worked well for a couple weeks, until I was informed that was not legal because I didn’t have a license to sell lollies at the netball games. So I was promptly stopped at the age of 10.

When crypto came along—I was exposed [to it] in the early part of 2017—it was a way for me to express my, I guess, mercantile nature. Rather than selling lollies or video game items, I was looking at projects and making a call on whether I thought they were mispriced.

All my knowledge about markets is specific to crypto markets, and my knowledge about traditional finance is limited to what I’ve been taught by my co-founder and the people I work with who have, individually, 15-plus years writing [software for banks’ and trading firms’] exchange connections.

The Market

The crypto markets are quite simple, and [it’s] easy to get started. You can start with $10. You can create an account—not high-risk if you’re just starting with $10—although you can give yourself 100x [100 times] leverage. If you’re inquisitive, it’s very easy to get into the space and teach yourself.

The nice thing about crypto is that you’re exposed to all the loose wiring that exists in this industry. And you can electrocute yourself on that wiring, but you can also get an intimate understanding of how the internals work. I think, given the fact that you can pretty much do anything you want unencumbered and without anyone’s permission, ideally you need to be this curious, hands-on person to learn it best.

Typical Day

Any manual trading that I do, in the back of my mind it’s always: Why am I pushing this button? Could I not have the computer do this for me? And the answer is usually: Yes, but it would be a lot of work to have the computer do it. So for now, I’ll just do it.

Where I spend most of my time is this “yield farming” thing, which is probably the furthest removed from traditional finance. It’s like if a hedge fund strategy was to go around and open all of these rewards accounts for the different banks, and then just move money between them really fast. And that sounds crazy, but that’s actually what we do in the crypto space. There’s a lot of interest rates out there, or a lot of venues and projects offering high interest rates—obviously with a risk attached. Understanding that risk is the bigger part of that, and knowing what’s a genuine opportunity and what’s not worth it.

I wake up at 10:15, and then at 10:30 we have a software developer concept of a team stand-up. I say 10:15, it’s more 10:22 for 10:30. I try to get to bed before 2 a.m. Eight hours is the goal. Sometimes that doesn’t happen. But I usually find for every 30 minutes I take on the left side of my sleep block, I lose an hour of productivity on the right side. So it’s a really bad trade, unless something is really important. Usually, I try and prioritize getting those eight hours.

Most of my day is not planned at all. It’s pivoting between what needs to be done, whether it’s jumping in a meeting on tax or regulation, or going and having a technical discussion with one of the devs [developers] around how to send a message from A to B. Should we send it in this format or that format? So there’s a lot of different types of work. I’m dragged between meetings and between tasks. I would like a little bit of structure.

Disruptions

It’s been a wild journey. From putting money in shortly after I started mining, to six months later that drawing 10x [10 times], and then actually having that retrace all the way to the point at which, in Australian dollars, I was down. And now, [after] the recent crypto action, being quite comfortable again.

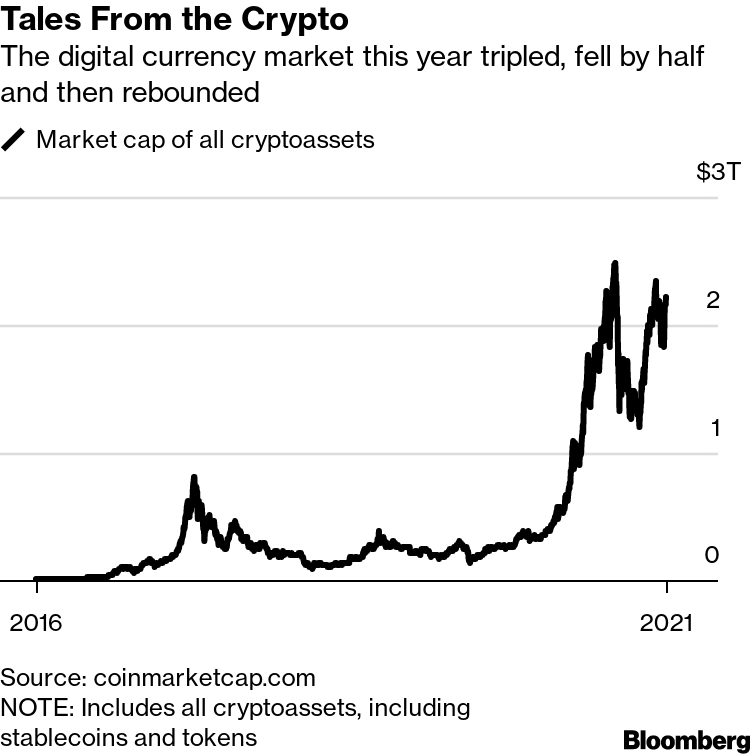

Tales From the Crypto

The digital currency market this year tripled, fell by half and then rebounded

That’s what makes me very happy to be working on an arbitrage, quant-type business venture. You’ll spend years building out your IP [intellectual property] and building on an idea that you believe will work—and if it works in the end, you’re not as exposed to the whims of the market. And I guess yield farming is an opportunity where, if you put in the effort to do the DD [due diligence], you can guarantee your success. It’s not going to be as flashy as the long-exposure funds that pull hundreds of percent per annum, or the VC [venture capital] funds that invest in the next unicorn. But at least it avoids all the stress of the up and down, right? So every day for us it goes up until something bad happens with the tech, or a counterparty goes down on us. But apart from those hidden risks, I think having that early insane volatility of crypto has helped me manage volatility and understand that I could always be off by an order of magnitude.

Trading Advice

I don’t think I have an edge as a trader by the Hollywood definition of a guy who sits at a desk picking equities and slinging cash. But what I think is setting me up to be successful is—at a personal level with my personal investments—I stick to the stuff I know. I stick to the stuff I have conviction in. I don’t feel FOMO [fear of missing out] at all.

For me, trading is just about being able to think rationally and as close to first principles as possible, and being able to peer through the noise and see the genuine risk and the genuine trades.

What’s Ahead

If you can be that one firm that has the best software in a particular domain of the market, then regardless of where the market moves, you can make a good return. It solidified our conviction to move on to a deep-tech, low-latency [minimum lag in technology response time] arbitrage and market-making path.

A lot of crypto has been rediscovering the traditional financial markets, but on fast-forward speed.

When I first started, DeFi [decentralized finance] didn’t exist. Now we have exchanges like FTX offering very sophisticated spot-margin products, futures-trading products in a very clean model.

I expect maybe in the next three to four years we may see genuinely new things gain adoption, right? Options are starting to get some traction, nothing on-chain [on blockchain, the technology that underlies cryptocurrencies] yet. I think the only unique product to crypto is the perpetuals [a type of futures contract] that have taken off, and in a big way. I’m looking forward to the future, there being some genuinely innovative products that take off within the cryptosphere.

We’ve already seen 6,000 cryptocurrencies, but we’re going to see 60,000 more. And if prediction markets take off, we’ll see 100 new markets appear every day and 101 stalling out every day. And so being able to build software and being able to build a trading firm that can trade tens of thousands, hundreds of thousands of different markets, it’s going to require automation. You can’t have that many markets managed by people, and it’s going to require planning for that future.

Lee covers cross-asset markets in London.

THE VETERAN

Interview by Divya Balji

JOHN CHRISTOFILOS, 56

Toronto

Chief trading officer, AGF Management Ltd.

Assets Under Management: C$43.4 billion ($34 billion)

Early Days

I’m very fortunate to be a son of an immigrant who came over to Canada in the early ’60s. My father’s first job was as the bartender for the traders on Bay Street, so he got to learn about trading, talking to the traders every day.

As a 14- and 15-year-old young man I used to take a subway downtown to Bay Street and sit at the end of the bar. I would watch the traders come off the floor and talk about the great things that happened that day and the things that didn’t go so well. And I remember—vividly—telling my father after one of the visits, “I want to be a trader.” I started reading the newspaper, checking the stock quotes and the like, and that’s how I got the itch for trading. Four years later, I became an input operator on the floor of the Toronto Stock Exchange. And that’s when my career started. That’s back in 1984, a long time ago.

Typical Day

I’m up at 4:09 every single morning. People always question the 09, but I must tell you I’m a very superstitious and routine-driven individual. Nine is my favorite number, after Gordie Howe and the Detroit Red Wings. So I must wake up at 4:09 every single morning. I literally jump on my elliptical machine. I turn on my laptop, and I’m checking the overnight markets. At AGF we’re a global shop, so we trade in 44 different markets around the world. I’ll check Asia and, about that same time, Europe is starting to open. Sometimes that day doesn’t end till 1 the following morning because after a full day of trading North American hours, we get a couple-hour break, and then Asia reopens. It’s not every night, but two or three times a week we’ll be up quite late trading the Asian markets.

We’re taking hundreds of phone calls a day. We’re getting thousands of IB messages in our Bloomberg workstations all day from dealers around the world. I get somewhere between 500 and 700 emails every day. It’s too many to read, but we get them. At 9:30 I always say, “We buckle up and go for a ride.” Because that’s when the market opens and things start to get a little bit more hectic. And then throughout the day, we’re having discussions with our analysts and portfolio managers and our dealers on the other side about what’s happening in the market. I love trading. And if I could do it 24 hours a day, I would. And maybe some days it feels like it’s 24 hours.

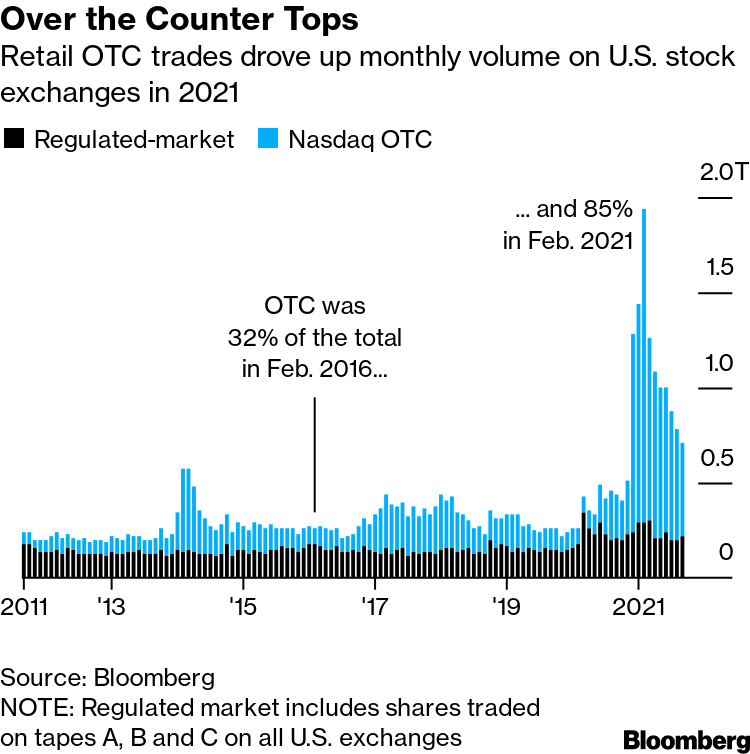

Over the Counter Tops

Retail OTC trades drove up monthly volume on U.S. stock exchanges in 2021

Other superstitions include literally being on the minute when I’m doing things throughout the morning. I have a bunch of calls that I take early in the morning from our dealer. They’re regimented. Then we have two morning calls with our own investment management team in the morning and then with our staff, especially during the pandemic, we’re having these calls twice a day, early in the morning to update everybody on markets and what happened overnight.

So, yes, I am a routine person. The only part of the routine that’s not normal is when 9:30 hits and the bell rings, I don’t know what’s going to happen. Markets are very volatile these days.

Highs and Lows

So my biggest trading high isn’t a particular trade, but it’s a series of trades that we get involved in. They’re called block trades, so larger quantity trades. It’s great to see that, because you know you’ve initiated, you assisted, and you executed on the trade.

The biggest low is a particular instance that happened way back, one of my first orders. I wrote it down, and I ran out to the square on the trading floor, and I yelled out, “I’ll buy 50,000 ABC.” All of a sudden, all these tickets started coming at me. I run back to my phone clerk, tell him I bought 50,000 shares, and he looks at me. He says, “John, we told you to sell 50,000 shares.” That was a low point. That taught me a lot, that errors do happen, and you have to be very, very diligent in the trade process.

Disruptions

We went from chalkboards on the floor to computers to, now, supercomputers. If you look at the last 10 or 15 years of evolution in the trading game, it’s changed dramatically: dark pools and algorithms and tick sizes. We went from eighths—12 and ½-cent spreads—to sub-penny spreads. The number of trades that occur now—we used to do tens and hundreds a day—we are now doing tens of thousands a second.

I think the biggest change is multiple marketplaces, right? It was very simple, single market, single point of contact. Now with dark pools and multiple marketplaces and ATS [alternative trading systems] and the like, there are 50 in the U.S., 15 in Canada—I’m only talking about North America now—that you have to have full connectivity to and understand how those markets work. I think that’s the biggest disrupter, No. 1. And then No. 2, going from eighths [of a dollar] down to pennies, in terms of spread.

And then on a technology perspective, everything now is chopped down. There’s fewer block trades. So algos [algorithms] are in the market, and they’re terrific tools. You don’t have to use it every single time. And in fact, there are certain securities that you don’t want to use an algo in—illiquid securities, low-priced securities, they’re much more difficult to trade, and you’re probably going to move the price if you use a systematic algo.

Trading Advice

There are three or four really key things. One, taking emotion out of it completely. Staying educated—very, very important. Staying disciplined, right? And staying patient, especially in an environment like this, where we have volatility, unbelievable intraday. If you can take advantage of the volatility in the market, you can add alpha [outperformance] to a portfolio. So the more volatility, the more opportunity for us as asset managers to take advantage of that opportunity.

What’s Ahead?

There’s an opportunity when there’s lots of excess volume. And we’ve seen that with a lot of these meme stocks. The retail [investor] engagement from my perspective is unbelievably good for us. I am a big fan of growing our ecosystem. We don’t want this to be an elitist environment. We want everybody to participate. The other thing I think that will happen is most traders will have to up their game in terms of other asset classes. So if you’re a cash equities trader, you better understand the options market, the futures market, the fixed-income. I think you’re going to get more multiasset traders in the industry.

Balji is the team leader for equities coverage in the Americas, based in Toronto.

THE QUANT

Interview by Liz Capo McCormick

KATHRYN “KATY” KAMINSKI, 43

Boston

Portfolio manager / chief research strategist, AlphaSimplex Group

Assets Under Management: $6.5 billion

Early Days

I grew up always loving math. As a kid, I sort of always assumed I’d be an engineer or do something like build bridges. But then when I was twentysomething, I did an internship working for a bank, doing some modeling, and it was so exciting and so dynamic, and I was so fascinated by the world of finance. I decided that finance and the markets were for me and just never looked back after that point.

I did a Ph.D. at MIT in operations research. I was so excited to have the opportunity to work with professor Andrew Lo, who was my thesis adviser. He was a huge influence in teaching me about the world of systematic trading and how quantitative techniques can be used in finance. My Ph.D. thesis was actually on trading rules and simple ways that we make decisions in investing, and why people choose to make decisions based on these rules. So naturally, of course, I wanted to get my hands dirty and get out there and do it myself as well.

The Market

Systematic trading is really exciting, because what you’re trying to do is disentangle the decision-making process from the gut reaction process. It’s about getting up and looking at the markets and seeing how your models are performing relative to where the market’s moving. And making sense of today’s moves, examining the positions, and also thinking about: What does my system and my decision-making system know, and what does it not know? And how are things changing?

The true challenge of a systematic trader is to understand how to build models that move with markets as they change, that incorporate information in a robust and straightforward way. A very fast model is going to change its position more aggressively as you see changes in the markets, whereas slower models are going to take more time and absorb information at a slower rate. When you build a portfolio, especially of multiple models, it becomes very complex. Each of your models represents a way to decide: Do I believe that the market is going up, or do I believe it’s going down? And you use that information and aggregate it to come up with a view. It’s very similar to a discretionary approach. It’s just much more clear to determine what’s actually driving you.

Crisis Trading

The primary data that are important for us are price and volatility and things like volume. And so when we see something like a Covid-type event, you see volatility spike, which tells you something about what’s happening to risk and risk preferences. I love the term “crisis alpha.” I’ve studied it a lot and written a lot of papers on it. Everyone likes the alpha, and no one likes the crisis. We had that exact experience in Q1 2020. We saw energy prices starting to fall. We saw some very negative signals in Asia. Then we also saw energy start to really sell off. We also saw bonds rallying aggressively and yields dropping drastically, way before the equity markets even fell on Feb. 21. What was interesting to me about that is all of those trends were extremely strong. And yet the equity market just sort of hummed along and was complacent. And even I was feeling like: Oh, this is not an American problem.

And then on the 21st, the market dropped. And everyone realized: Wait a minute, this is everyone’s problem. Sometimes it’s very hard to really understand what’s going on in the market as one individual person. But when you use some very quantitative techniques, you can understand what prevailing trends the markets are telling you. Our strategies actually do better during periods of crisis and stress. And that’s why it’s a strange scenario, because you feel uncomfortable yourself.

Trading Advice

It takes discipline to be objective with short-term data and not overreact to it. We actually design a lot of protocols in our day-to-day to tie our hands. Anything we do has to be approved by an investment committee, so that means there’s a lot of checks and balances in terms of what goes into our decision-making process. I still don’t like it sometimes, but I don’t have the access to sort of make a gut decision.

I always like taking long walks and getting some fresh air. And I have to get up every once in a while from my computer and move around and sort of think about new ideas, or take a jog or run and walk the dog. Everything we do is very team-based, and that also helps.

Disruptions

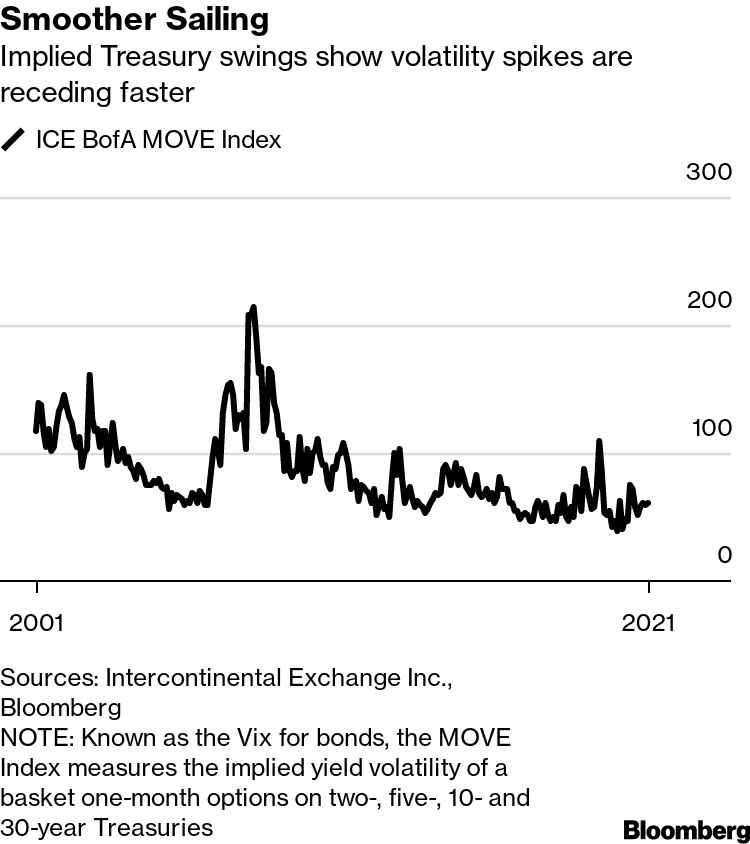

If you looked back over the last 20 years, volatility was very asymmetric. It would spike up, and then it would be much slower to come back down. We’ve noticed in the last 10 years or so that that characteristic of markets has actually changed quite a bit. We saw volatility spike, and it dissipated a lot faster than it did historically. Our goal is to find different ways to measure volatility so you can allow it to dissipate faster or slower, depending on what you measure.

Smoother Sailing

Implied Treasury swings show volatility spikes are receding faster

The things that we hate are cross-asset reversals—days where many different asset classes or core themes revert. It’s often deleveraging. June was a challenging environment, because you saw massive moves in terms of where the market believed the world would go once the Fed came out and spoke. As soon as the Fed came up and had something to say about inflation and tapering, then people started to think differently. Market prices moved very aggressively in multiple markets. We’re much more concerned about those types of scenarios than we are about equity markets in general.

What’s Ahead

We always follow the systematic process. Sometimes when I tell this to people, they’re shocked. Because they say, “Well, now you’d have more information.” I said, “Well, one individual doesn’t have more information than the market.” I think we like to think we do—and we definitely feel like we do sometimes—in those moments.

The only times when systematic traders really need to think about adjusting the models are if there’s something that our models don’t know that is very extreme. Something like the tsunami or the earthquake in Japan, where you have another type of risk, a risk related to whether or not the market will be open. Those kinds of risks we pay attention to—migration of exchanges, regulatory stress—our trade-models don’t know those things.

We often get a little nervous around very bimodal events, things like elections, when it’s clear that there’s going to be a lot of volatility in the future that is not in models or easy to measure. So in those types of situations we tend to have a lot of meetings and sort of ascertain how serious is this event. But most systematic traders will not make a directional call. They might decide that risk is too high, but it’s very rare. It’s very, very rare on purpose.

Capo McCormick covers rates and foreign exchange markets in New York.

THE DISTRESSED-ASSET TRADER

Interview by Rebecca Choong Wilkins

MICHEL LÖWY, 51

Hong Kong

Co-founder/Chief executive officer, SC Lowy Financial (HK) Ltd.

Assets Under Management: $1.5 billion

Early Days

The first time I truly traded distressed assets was in ’99 when I decided to move from my previous employer to Deutsche Bank to start their distressed trading business for Asia back in Singapore. That was a sell-side business with a large balance sheet, that’s why I got into trading.

The Market

What’s really interesting, if you compare Asia with Europe or the U.S., is that the market is way more fragmented. You cannot compare India with China, Korea, Indonesia in terms of the type of opportunities, the type of corporates. Obviously the U.S. is just one market. Europe—there are differences between countries, but I can see in our business in London there are a lot more similarities between looking at a German corporate, a Dutch corporate, or an Italian corporate, while here in Asia the differences are still much more significant. You may look at countries like Japan or Korea that have extremely developed insolvency regimes that are fairly predictable. And you look at Indonesia or even China that are much less predictable and where you may not be able to rely on their legal system or on the accounting numbers as much as in other markets. It’s not like Chapter 7, Chapter 11, that’s the formula that’s going to work. And that’s why after doing this for 25 years I’m still having fun.

Typically the corporates that are distressed in Asia tend to be smaller. They tend to be sometimes privately held companies as opposed to public companies, which is the case in the U.S.

In a country where the central government is as important as China, you often find a fairly binary outcome [for] whether or not the government is going to support that corporate or whether the government is going to change the rules of the game. And that was the case 25 years ago as well. There’s a difference between being state-owned and a guarantee by the state.

Typical Day

My typical trading day today is very different from what it used to be, because, to be perfectly frank, I don’t trade as much as I used to, sadly. It starts with the morning meeting. The morning meeting is sacrosanct for me, so everybody’s got to be there on time. Then obviously you start to trade, read research, see clients. Being in Asia, you can afford to have a long lunch or even occasionally go to the gym and get yourself ready for when London comes in. I traded in New York way back, 15 years ago. The difference is that in New York you have a much shorter trading day, much more intense. While in Asia it’s a much longer day, but the rhythm changes more during the day. So you start at 7 or 8 in the morning and sometimes finish at 2, 3 in the morning, because you still trade with U.S. clients until late in their session.

I like to get to the office before the others, set up my list of priorities, things that I want to achieve. And I think it’s important to have that, because when you trade, you get pulled into many directions all day long. So going back to your list of what am I trying to do here is really, really important.

Trading Advice

In distressed, to be a successful sell-side trader you need to want to win. And there’s no small trade or big trade—it’s about winning. As a trader, the energy level of the entire trading floor depends on you. So if everybody’s sleepy, you’ve got to find ways to get that energy going and the momentum going. It’s having those fundamental skills, interpersonal skills, energy level, and a desire to win.

If you are a good distressed investor, you take less risk. There is more risk involved, but you understand those risks, you assess those risks. And what will happen in the next few years won’t be surprises. Now, you’re not always going to be right, but you need to be right about understanding the risks. And once you do that, it’s very comfortable, because you have a road map, and you follow that road map for a few years. You need to make mistakes to understand how to get better next time. And, like everyone, I’ve made mistakes, I’ve made bad investments.

Disruptions

When I started trading distressed in Asia, there were fewer than five players. And within a few years there were maybe 10 players. Today there’s still not that many if you compare Asia with the rest of the world. There’s 20, 30 players that play in the space, not more.

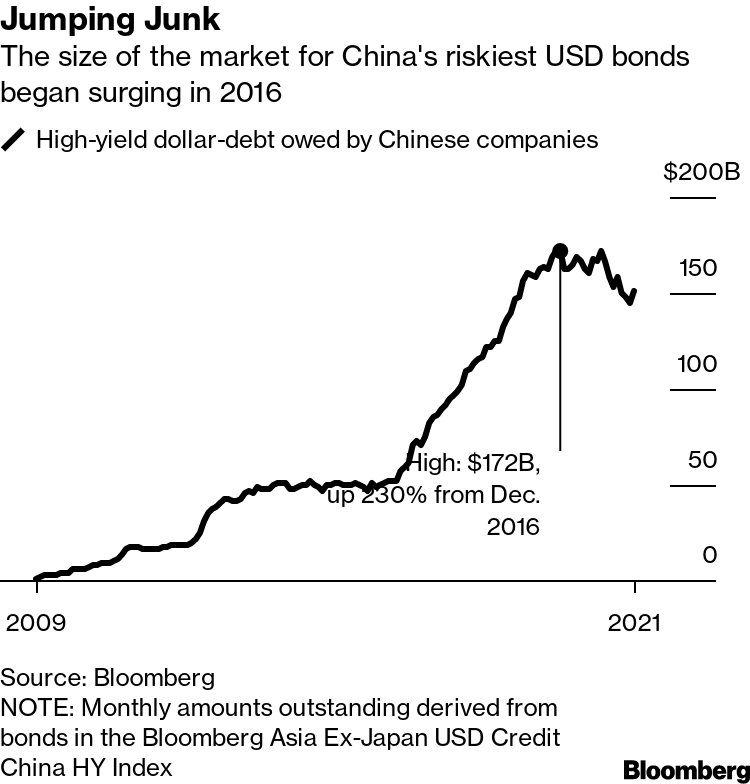

Jumping Junk

The size of the market for China's riskiest USD bonds began surging in 2016

Fifteen years ago, there’s no way an independent player like SC Lowy would have been as successful as it is today. And the fact that banks are putting less capital at work, the fact that they aren’t capable of retaining their best staff is giving us more opportunities. There was no Chinese high-yield bond market 10, 15 years ago. And now you have $200 billion issuance, which makes it a quite large market. It’s not a mature market in the sense that the rules of the game are still not totally clear. Which is why when a Chinese corporate becomes distressed they tend to immediately trade at 20¢ rather than 60¢. I believe that in the next few years we’ll start to be able to better predict the outcome of restructurings.

Highs and Lows

What’s interesting is that many of the successes have led to the next success. One of the largest transactions we did, I think back in 2013, was the restructuring of KLC, Korea Line. And at the time we were involved [in] buying bankruptcy claims, converting them into equity. We did a DIP [debtor-in-possession] financing that my business partner, Soo Cheon, had to explain to the court in [South] Korea. It was the first DIP financing ever in Korea. And that gave us a lot of insight into shipping in general and containers. And so we got involved in another company called Zim Shipping. And we ended up buying secured claims and unsecured bonds. And as part of the restructuring we ended up with quite a bit of equity—equity that we exited only recently this year. And that was one of the many reasons that we are having a record year at SC Lowy, because they [Zim Shipping] took advantage of container rates to lease the business and to go from high to high. That adventure started on the back of KLC eight years ago. Which is another lesson about distressed investment: patience.

I think one of my trading lows was back at DB over 20 years ago, where I bought something that I should not have purchased. I didn’t have a reason to buy this, and I wanted to sell it. And so I sat on the trading floor asking my team to bail me out, and that’s just not the way it works.

The big lesson is don’t do something unless it’s your decision. Yes, as a sell-side trader, you’re there to trade, you’re there to create liquidity, you’re there to help your client, but there has to be a strategy. So the first piece of advice [for junior traders] is that—not if but when they make a mistake—they talk to me immediately. The traders who are trying to hide their problems, that’s how you set yourself up for a catastrophe. In our risk management the No. 1 thing is dialogue; to sit on the trading floor so that we’re aware of what’s happening.

What keeps me awake at night is for traders in different time zones to make a mistake and not daring to wake me up. And a few times they’ve woken me up in the middle of the night, and I’m grateful that they did, because collectively we were able to find a solution.

I seriously dislike a very quiet trading floor. And maybe I’m old-school, but I believe that you get a lot more out of a real conversation than an IB chat.

What’s Ahead

I believe that the increased defaults of Chinese issuers are going to force all the different players to set the rules of the game so that it becomes more predictable.

I was one of the first to highlight that the problems in Evergrande [property developer China Evergrande Group] were going to be very complicated to sort out without government intervention. The price from a risk-return standpoint didn’t make sense. And we’re only talking a few months ago, [and now] we’re finding ourselves in the situation where we could see one of the largest restructurings in Asia ever.

Choong Wilkins covers China credit and distressed debt in Hong Kong.

THE CREDIT TRADER

Interview by Sonali Basak

JOHN ZITO, 40

New York

Senior partner, deputy CIO of Apollo Credit, co-head of global corporate credit, Apollo Global Management Inc.

Assets Under Management: $330 billion in credit

Early Days

I was an econ major, so I’ve always been more math-oriented. I grew up in Miami. [Amherst College] was a big culture shock for a couple of years. I learned a ton going to a totally new environment. The liberal arts education at Amherst is broad and great from an investor’s perspective to really think about all the different outcomes.

I actually didn’t even know what a bond was, and my stepfather said, “You might want to try Wall Street.” A bunch of my friends were going into investment banking, and I actually took a different route. I joined a small convert arb [convertible arbitrage] fund. This was just trading convertible bonds and, at that point, high-yield bonds. There was a guy there named Jim Kastberg, and he was starting a $5 million hedge fund. Back then you could start a hedge fund with a guy and a Bloomberg [terminal]. In a year he raised over $1 billion.

The fund started in 2002, and I was really a second employee. I did everything from learning the whole back office to booking trades. I evolved into being the trader for the fund, because he [Kastberg] was out capital-raising a lot.

I’ve only been on the buy side. Most traders start on the sell side and go to the buy side. I learned the way to construct a portfolio, the way to deal with LPs [limited partners], the difference between a good investment and bad investment, when to get out of an investment when you’re wrong—all of those important things that require you to get things wrong, to actually learn.

The Market

The leveraged finance market’s somewhat of a cottage industry. A lot of the people I still know today, I’ve been in the markets with them for 20 years. There’s a handful of people making a majority of the decisions on big pools of capital. When I started we were just coming out of the tech bubble, and you could buy bonds at 50, 60, 70 cents on the dollar, and there wasn’t a central bank put. You had longer cycles. Now you don’t have those cycles anymore, and you have interest rates that are very low. The return environment is much more difficult to charge hedge-fund-like fees. The ability to generate alpha is much harder than it was before.

Typical Day

I tend to wake up during the week around 5:30. I try to work out three or four times a week. [Trading is] all current events-related—it’s a new idea, a new industry. You’re learning about weather—I learned about tech, then oil and gas, the banking system—I mean, it’s super engaging, right? It’s competitive, team-oriented, culture-driven. There are all these things that just are so fun about it. I love it.

Highs and Lows

Primus Telecom, 10 and ¾ [percent] bonds—it was one of the tech names that came out of the tech bubble that was supposed to recover. I had a call with the management team, and they told me that for sure they were going to refinance the bonds at 105. I went to the PM [portfolio manager] and said, “I talked to the company. The company said they’re going to refinance the bonds.” I thought it was that simple. They ended up filing for bankruptcy within a year of that. That was my first big mistake—totally naive about questioning the assumptions that go into the model.

If you haven’t had any big losses in your career, you’re probably not taking enough risk. You get pretty humbled by the markets. Your lows, when you lose money, always feel much worse than any of your wins. That’s for sure. I think the proudest moment was probably just the entire Hertz ecosystem—where we put $6.5 billion into the estate over the last 12 months. We provided tons of capital, all different parts of the capital structure, showcased the entire firm.

Disruptions

I do think over time, it’s going to go more toward electronic trading platforms. You’re seeing portfolio trading ramp up significantly. You’re seeing certain market participants try to make credit more of a widget, which, as fundamental investors, we have issues with. People will just say, “I can buy a portfolio of double-B [rated] loans or double-B [rated] bonds, and that’s fine. I don’t need to do credit work on any of it.” I think over time, there’ll be credit cycles again, and I think you’re going to see some losses taken in some of the portfolios where people are putting either too much credence on rating or too much credence on the diversification. Then we’ll be more active [in trading] again. I joined Apollo because it’s a deep, fundamental bottom-up shop. We never trade just to trade.

Covid Crisis

We transacted over a 100 billion [dollars] of debt last year. We’re one of the largest counterparties with the Street, but most of it was acquiring debt in March, April, and May. Then toward the end of the year, as things normalized, [there was] selling. In some cases, we’re just owning it.

I had a daughter on Feb. 10. So we had a 1-month-old, and then I got an email on I think March 15 that I was exposed to someone in the office with Covid or something. We rented a house, and I was locked away for a week during the most volatile times, so that was fun.

We were underwriting to some pretty low, pretty draconian situations, but the firm gave us latitude. Obviously we had to go through all the proper investment committees and everything else, but they really trusted the credit business to invest significant pools of capital. We started [holding] 7:30 a.m. calls. We would go through—every morning—every name and all the way through across the business, private equity, real estate, credit. In corporate credit alone, we have close to 700 [investments]. That environment is in some ways exciting, right? Not great for where the world was, but from an investor’s perspective, that’s the environment where you get to really differentiate yourself. We were some of the largest lenders on some of these companies.

We drew 100% of every dollar committed to us from March 14 to March 31. That’s why our investors are with us. Every time there have been bouts of volatility or there’s a new trend, we tend to be forward-leaning when it comes to credit. I think they kind of expected it from us. We ended up raising more capital in April. If you look at all the new issuance, all the refinancings, all the activity, it was about a trillion-dollar opportunity. I thought it was going to be over two years. It happened, it felt like, in maybe six months.

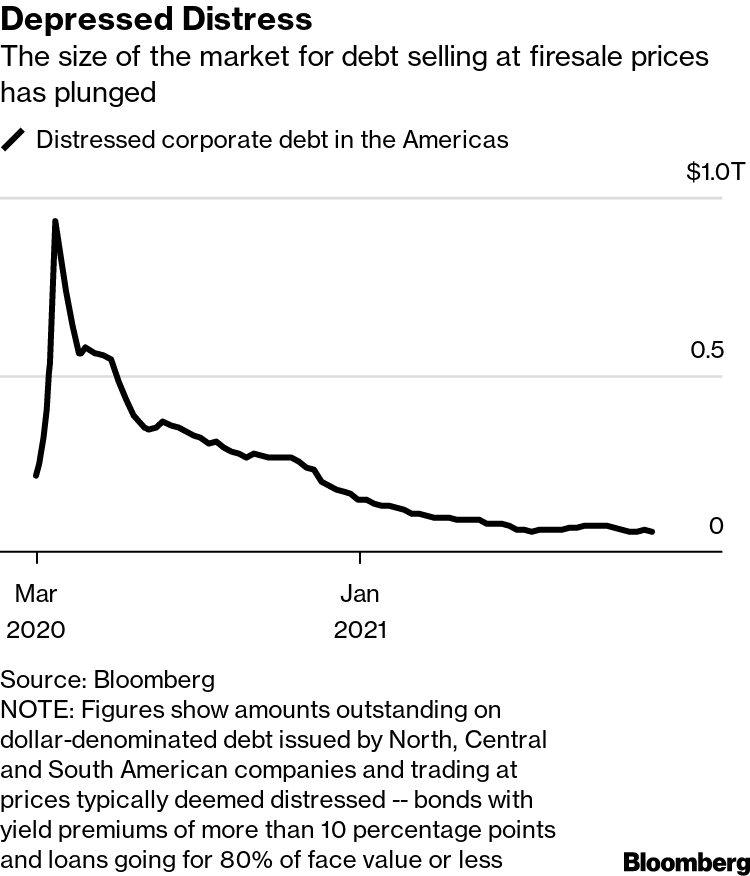

Depressed Distress

The size of the market for debt selling at firesale prices has plunged

My birthday was March 21, and I think the [market] low was March 23, so that was, like, the worst birthday. I remember that weekend calling my head of research and saying, “How bad can it get?” We were probably a week early in terms of starting to buy and, you know, we weren’t feeling great at the time. We had significant mark-to-market losses, but it all came back by the second week of April.

Trading Advice

For us it’s impossible to transact in securities well without understanding the fundamentals. It’s the reason I joined Apollo. There’s a psychology around understanding what’s out there, not fighting the market—being respectful of what the market’s telling you—and being really cynical about every input that’s in your mind and questioning every assumption. Which can be tiring sometimes, but you have to do it.

What’s Next

The scope of what we do is changing. If you told me five years ago that we would be going into Amazon resellers and providing loans to them—I mean, the ecosystem is changing so fast.

San Francisco doesn’t think about debt financing—they [technology startup companies] think about equity, VC funding. But now they’re mature, and that transition is going to be a huge opportunity for us, and we’re excited about that.

Take all crypto, all tokenization, all DeFi [decentralized finance]—everything related has gone to $2 trillion. So everything that we do day to day, the market’s telling you is going to be disrupted. I think it’s coming to Wall Street pretty quickly. We can either fight it or we can be in front of it. We’re going to lean in. And if it’s wrong, we’re going to learn a ton. If we’re right, we’re going to be at the forefront of it. I think we have the scale to really change the way that certain things operate, and that’s going to be our focus.

Basak covers finance and wealth for Bloomberg News, Bloomberg Television, and Bloomberg Radio.