Wall Streeters Reel In Riches From a Year of Unequal Rescues

Many business lines are thriving amid government intervention.

In a year of catastrophe, corners of Wall Street have been thriving. It’s a feat that can be explained by one word: access.

Not to masks or vaccines, but to markets, to being in the flow. As the pandemic devastated large swaths of the economy, it delivered a once-in-a-generation windfall to those who buy, sell, borrow, lend and speculate in the world of high finance. Bank traders, dealmakers, hedge funds and even lenders are counting their profits after the tumult of 2020.

While officials squabbled over how to deal with the public health crisis, central banks acted swiftly, driving interest rates to new lows and stocks to new highs. The Federal Reserve loaded another $3 trillion of assets onto its books and pledged even more. Unintended consequences were another day’s concern. For Wall Street, that meant massive gains.

This will go down as one of the wildest and strangest years in Wall Street history, all the more so because it’s largely played out in work-from-home isolation, against a backdrop of so much human suffering.

But in an era that left so many feeling helpless, help came swiftly for the markets. Interventions fended off financial mayhem, but also left disparities in its wake. What follows is a look at piles of wealth created, and how they came to be.

Traders With Handguns

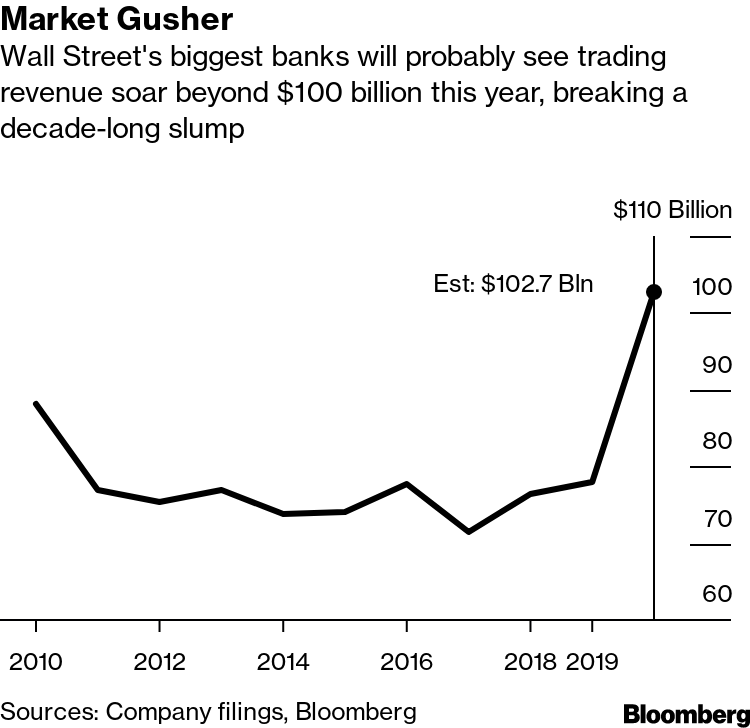

Market Gusher

Wall Street's biggest banks will probably see trading revenue soar beyond $100 billion this year, breaking a decade-long slump

Sources: Company filings, Bloomberg

On a Monday morning in late February, Wall Street seemed to realize the novel virus ravaging Asia was really a global problem. The Dow Jones Industrial Average tumbled more than 1,000 points that day, the first leg of a dramatic selloff from record heights. For many Americans, that was the first alarm bell. For traders, it was the long-awaited return of volatility.

If Wall Street bank traders are worth their keep, they make money whether prices rise or fall by matching sellers and buyers. Inside the most elite banks and market makers such as Citadel Securities, traders quickly realized they were embarking on a once-in-a-generation deluge of orders.

For a time, many shrugged off suggestions that they stop commuting downtown. Once they did, some snapped clandestine selfies, brandishing handguns in front of their “rona-rig” computer screens. One shows a trader waving a semi-automatic pistol, another a .357 Magnum. The message to confidants was clear: Nothing — not the virus nor the panic that had people ransacking toilet paper aisles — would pry them away from making money.

The five biggest U.S. investment banks — JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc., Goldman Sachs Group Inc. and Morgan Stanley — are now set to post their first $100 billion year for trading revenue in more than a decade. By the end of September, revenue surged 34% industrywide, according to a McKinsey & Co. analysis. Profits at Citadel Securities more than doubled in the year’s first half alone.

Executives are now debating how much to hand out in bonuses. Even though the optics of showering millions of dollars on traders in a time of national pain are ugly, bosses are worried their rainmakers will leave for deep-pocketed hedge funds, taking revenue out the door.

Expectations are so high that a trader who got $2.5 million last year has vowed to leave one of the nation’s biggest banks if he doesn’t get significantly more for 2020.

There’s also an argument that traders were just in the right seats at an opportune moment. How much more do they deserve if every giant bank saw trading revenue soar? How much was derived from government intervention in markets?

Whether it was wrought by their own brilliance or a gift from the Fed, traders want a slice of the billions they reeled in for banks.

Financing Financiers

Pandemic-Proof Payouts

Risky corporate loans that include funds for dividends surged to the highest level in years after the Fed unlocked markets.

Figures show the monthly volume of leveraged loans that include funding for dividend payments.

Source: Bloomberg

Across the business world, the pandemic set off a race to stockpile money to survive lockdowns. For banks, that meant unprecedented demand from companies hoping to max out credit lines or tap markets at a time when lenders themselves were retrenching. There wasn’t enough money to go around.

The Fed rushed out its own vaccine — liquidity — and suddenly bond markets that had been teetering on the brink staged a spectacular rebound. As the central bank slashed interest rates, appetite for riskier corporate loans bounced back. Most public companies got the cash they needed.

Some companies, often controlled by private equity firms, got that and more. They borrowed extra to line the pockets of their owners with special dividends, taking advantage of a familiar buying pattern in markets that has little to do with the underlying strength of the economy.

“Investors have made money almost every time they have bought a dip since 2009,” said Bob Kricheff, senior portfolio manager at Shenkman Capital Management. “If you’re playing tennis and you win hitting it to your opponent’s left, you keep hitting it to the left.”

With everyone hitting to the left, borrowers have grabbed $39 billion since April via loans that included proceeds earmarked for dividends — up from $34 billion in the same period last year. October’s $15 billion haul was the most for any month since 2016.

As the pandemic erupted, the idea that easy financing would let companies shower so much money on private equity owners might have struck many people as unfathomable. Now it’s come to pass.

Some injections line up with the pandemic economy: KIK Custom Products, which had already been growing, saw demand increase for its sanitizing products. The company owned by Centerbridge Partners sold $1.9 billion of loans and bonds this month, funding a $400 million dividend to the buyout firm, according to people familiar with the matter. Discount tool seller Harbor Freight is benefiting from a flurry of home improvement. It got a $3 billion loan from debt investors in October that included an approximately $900 million payout to its billionaire owner, people familiar with the deal said.

Spokespeople for the companies and their backers declined to comment or didn't respond to messages seeking comment.

And then there’s Finance of America, a lending platform owned by Blackstone Group Inc. offering products including reverse mortgages. The deals are often marketed to seniors who can borrow against equity in their homes, typically at much higher rates than traditional mortgages, with the balance due when they die. Finance of America sold $350 million of bonds in October for a payout to Blackstone. It’s now preparing to go public with a $1.9 billion valuation by merging with a blank-check company.

A spokeswoman for Finance of America said accessing capital markets helps it “continue to play its important role supporting the financial needs of millions of consumers.”

Blank-Check Bargain Hunting

Rush to Market

SPACs are holding IPOs at an unprecedented rate during the pandemic.

Figures show quarterly initial public offerings of SPACs through last week.

Source: Bloomberg

Blank-Check Flurry

SPAC fundraising is gaining momentum as dealmakers hunt bargains in the wake of the pandemic -- often with terms offering them rich rewards.

Figures show aggregate fundraising by SPACs through IPOs since 2015.

Source: Bloomberg

A few years ago, the mark of a corporate mogul was a Rolex and a Gulfstream. In 2020, it’s a special purpose acquisition company.

One after another, more than 200 blank-check companies have held initial public offerings this year, raising over $70 billion to hunt for bargains. Many are chasing privately held companies reluctant to hold IPOs of their own in turbulent times.

Skepticism abounds. For starters, the executives in charge typically get special “founder” stakes that can equal 20% of all the shares — plus warrants that can juice their returns even more. Then there’s the two-year deadline to complete an acquisition for the awards to pay off, which critics say encourages bad deals.

One of the skeptics, activist short seller Muddy Waters Capital, called SPACs “the great 2020 money grab.”

Irwin Simon, who has ranked as one of the world’s best-paid executives even without the SPAC he launched in 2019, has been watching this year’s flurry. He defends the business.

“Everybody I know is doing a SPAC these days,” said Simon, who founded the natural products conglomerate Hain Celestial Inc. and runs marijuana company Aphria Inc. In June, his Cayman Island-based Act II Global Acquisition Corp. combined with a licorice company and a sugar-substitute maker both controlled by the billionaire Ron Perelman to form Whole Earth Brands.

To help justify their take, SPAC execs have to find great companies, Simon said.

“There’s no windfall if the stock doesn’t work,” he said. “The next six to nine months are going to be key. If they don’t find good companies and don’t do good deals, SPACs could get a bad rap.”

Simon wanted to name his Italian water dog SPAC, he said, “but my wife wouldn’t let me.”

Hedge Fund Revival

As the Trump administration played down the pandemic early this year, the head of a $4 billion hedge fund stumbled onto Twitter videos that made his eyes widen. They purportedly showed Chinese authorities welding doors shut to enforce lockdowns. He saw it as proof a disaster was coming to the U.S., and that it was time to prepare and play it right.

Before 2020, a lot of hedge funds looked like they were inching toward irrelevancy. But in the pandemic era, they regained their mojo.

Boaz Weinstein’s flagship hedge fund at Saba Capital Management, for example, returned 82% this year through October. Heading into 2020, investors in his fund had received an annualized return of around 3% — on par with a low-cost muni-bond mutual fund. Assets had dwindled to below $2 billion.

Like a lot of hedge funds, Saba is designed to perform in volatile markets, and volatility has been scarce for most of the last decade. The industry lumbered along, with assets stuck around $3 trillion. Some funds prospered, with Citadel, Millennium Management, Two Sigma Advisers and D.E. Shaw & Co. getting bigger while many of the rest languished as returns suffered.

This year offered a “much needed” chance for hedge funds to prove themselves to clients, said Jon Caplis, who runs research firm PivotalPath.

Most every strategy has performed well, with some specialty stock funds among the top gainers. Technology, media and telecom funds rose 29% on average through November and health-care funds jumped 21%, according to Caplis. Even discretionary global macro funds hit their stride after struggling for years with Andrew Law’s Caxton Global Investment fund rocketing 36% through late November and Rokos Capital and Brevan Howard Asset Management churning out bumper profits.

Caplis expects next year could build on 2020.

“I don’t think we’ll quickly get back into a low-volatility environment,” he said, pointing to November’s vaccine euphoria. “In the aftermath of Covid, we’ll still be dealing with a rapidly evolving global economy and macro factors, like trade with China, that the pandemic pushed to the back burner.”

Home-Loan Heyday

One of the surest ways to make money this year was to stand between Americans rushing to lock in cheap mortgages and a U.S. government eager to prop up the housing market.

Home lenders have reported bumper earnings in 2020, thanks to record-low interest rates, the flight of families to the suburbs and an unprecedented promise by the Fed to buy an unlimited amount of mortgage bonds. For companies that underwrite the loans and then pass off the risks, the business hasn’t been this profitable in at least 20 years, according to data from the Washington-based Urban Institute.

By the end of the year, Americans will have taken out a record $4.4 trillion of home mortgages, according to data provider Black Knight Inc. That’s roughly $600 billion more than the previous record set in 2003. Mortgage executives describe 2020 as the industry’s best year ever.

Usually, mortgage defaults rise and fall with unemployment, pulling the business of underwriting new loans along. But in a year when more than 10 million people suddenly found themselves out of work in the U.S., the mortgage machine is humming.

Few firms benefited more than Mat Ishbia’s United Wholesale Mortgage.

His Michigan company is the nation’s largest wholesale mortgage lender, which means it provides the cash for home loans that initially are handled by brokers. The company projects it’ll originate $200 billion of mortgages this year, double its 2019 production.

United is generating margins normally associated with Silicon Valley technology darlings. In the quarter that ended in September, it reported net income of $1.45 billion on $1.83 billion of revenue. That month, United announced it would go public in a deal with a SPAC that valued the business at $16 billion.

Ishbia’s stake in the company would give him a net worth of about $11 billion, placing him among the 60 richest Americans.

“We are a large company that sells a product that nobody wants. Nobody wants a mortgage, they want the house,” Ishbia said. The wealth that’s generating “is much, much, much bigger than I ever dreamed.”