This article is by Shan Anwar, Corporate Treasury Product Specialist.

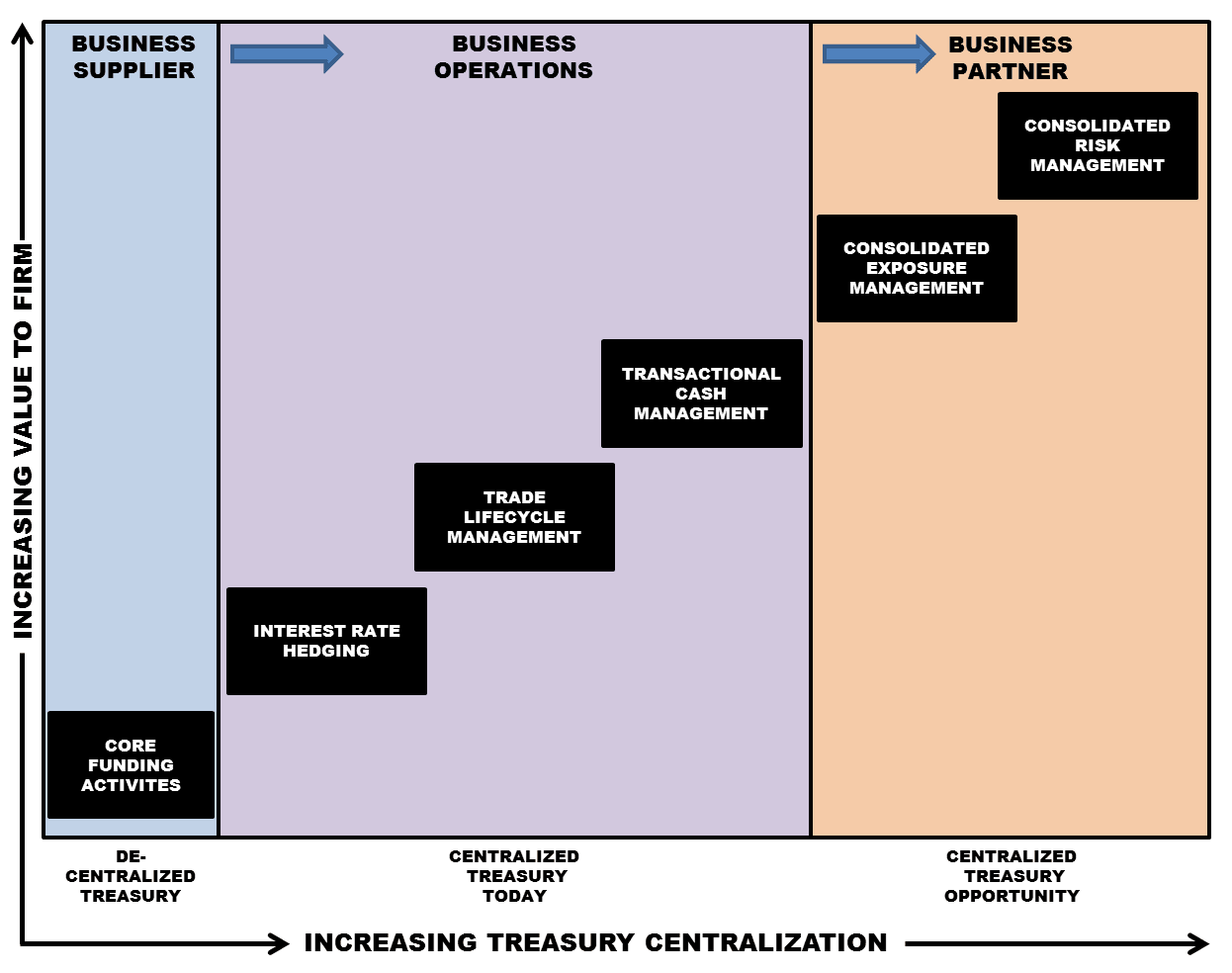

Historically, corporate Treasurers have only been responsible for their firm’s core funding activities. Treasurers in this context were funding suppliers to the firm’s constituent business lines, and their ability to add value to the firm was limited.

As the business environment has become more complex, however, some firms and their treasuries will need to evolve. The global financial crisis put liquidity and risk management in the spotlight, as the interconnectedness between these once siloed processes became obvious. This makes clear the need for more and more activities to become centralized within Treasury.

As sources of capital dry up, “funding” becomes more complicated. Funding activities require tools to hedge issuances. Hedging activities requires an infrastructure to be able to execute and monitor trades. Globalization requires that cash is managed across various currencies with diverse banking partners. Regulatory burdens have increased since the financial crisis, requiring cross-border management of the varying regulatory regimes. All of these activities need to be managed under a risk management framework that recognizes the firm’s risk appetite

A centralized Treasury model enables Treasurers to add increasing value to their businesses, and, in turn, become a partner to the underlying businesses they serve. In some cases this can even add to the bottom line. For example, centralizing all aspects of cash management within Treasury allow Treasurers to optimize their funding profile. External debt can be reduced as a result, reducing hedging activity. Derivative hedges can further be reduced by netting consolidated cash exposures across different businesses. One way to think of this is that for every $100 million reduction in derivative notional, Treasuries can save their organizations $30,000 (assuming a conservative estimate of 3 basis points saved on bid-offer spread).

Why centralize in the first place?

Centralization eliminates duplication of effort across the firm. For example, centralizing hedging and trading operations eliminates the need for each business line to have their own traders and trade lifecycle management resources. Agreements with counterparties are streamlined, reducing the operational burden of managing different external agreements and associated KYC requirements for different legal entities within your own firm.

Centralized cash management can provide similar efficiencies. Banking relationships can be optimized across the regions and partners with which a firm transacts. Central management of bank-to-bank payments increases the controllership over these transactions, reducing interest and other claims against the firm. Internal funding will always be cheaper than external funding, so that centralizing cash within Treasury allows an organization to tap into those hidden funds that may be available from internal operations.

Centralized risk management allows the firm to concentrate the management of the underlying exposures that give rise to financial risks. Risk management in this context will allow Treasurers to manage liquidity risk, market risk, financial institution credit risk, commodity risk, and operational risk. This allows business lines to concentrate on business and customer risk – their core expertise.

Finance and accounting functions can also be centralized for financial transactions within Treasury. This allows the firm to recruit individuals with specific expertise in, for example, designating derivatives under hedge accounting rules or the intricacies of valuing derivative for financial reporting (e.g., incorporating the non-performance risk of your counterparty bank). For the complex rules governing hedge accounting, especially, expertise and experience in designating hedges can save your firm from uncomfortable reviews with your auditors.

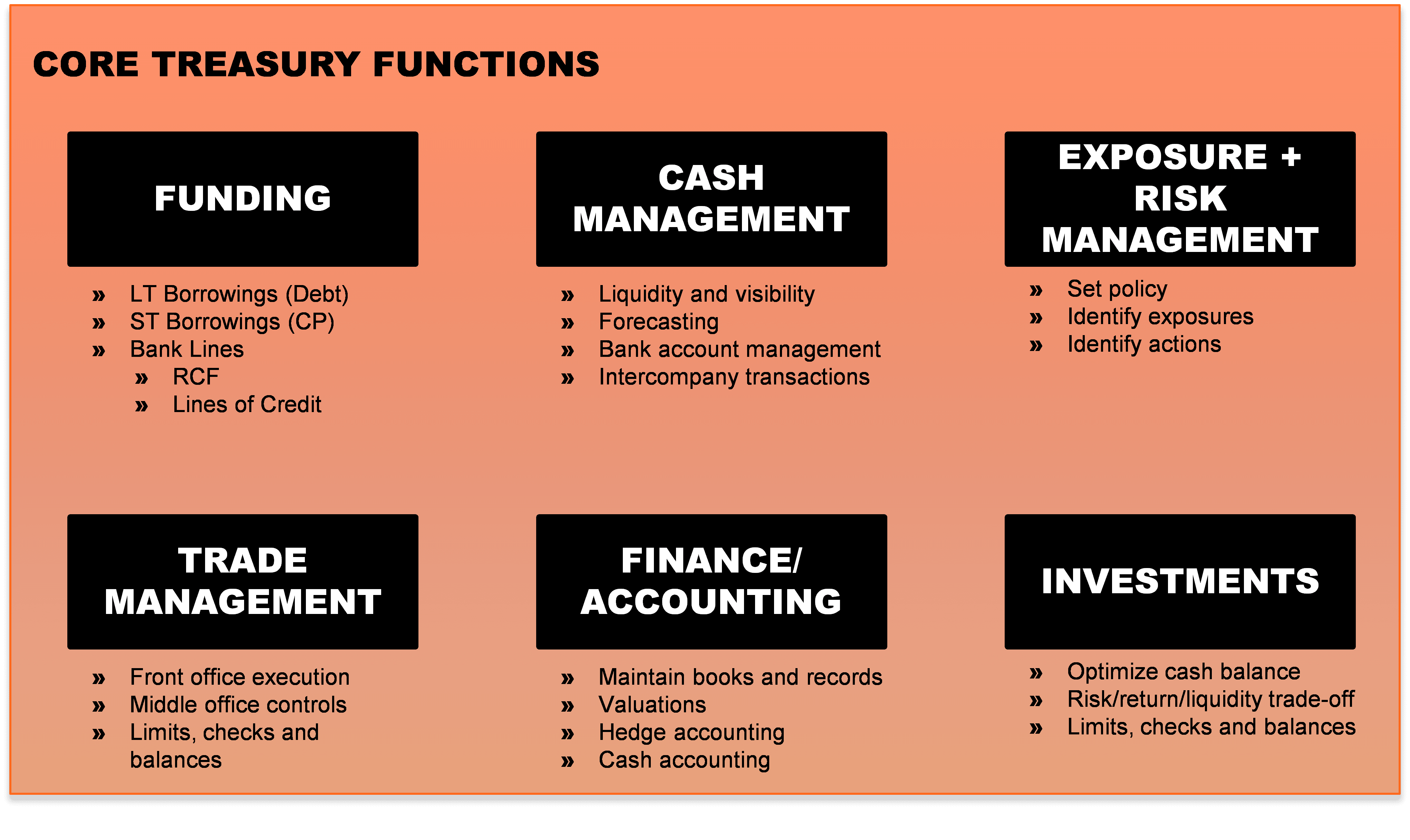

The diagram below summarizes some of the key functions that can be centralized within Treasury.

Barriers to centralization

Why don’t more corporates centralize Treasury operations today? Some corporates may find that a “hybrid” approach works better for their business – for example, subsidiaries are tasked with identifying exposures related to their line of business and then request head office operations to execute hedges.

The largest impediments to centralization, however, are technology limitations. Although Treasury activities are linked with each other, few systems offer the wing-to wing capability of connecting cash management with hedge management, requiring manual touch points or interfaces and manipulation of data.

Many Treasuries manage forecasted cash exposures within spreadsheets, for example, making the aggregation of exposures at the consolidated level a time-consuming and error-prone process. Those systems that do offer this functionality are expensive, with implementation taking months or years.

Other barriers include:

- Lack of resources – Treasuries are already lean functions within their firms. According to a 2014 AFP survey, 54% of Treasuries have less than five full-time employees. Given current resource constraints, asking Treasurers to do more will require realignment of existing resources to Treasury.

- Lack of framework – A holistic approach to Treasury management requires a framework to identify the various functions that need to be centralized as well as identifying roles and responsibilities on how those functions are to be managed.

- Lack of data – Related to the system limitations discussed above. In order for Treasury to manage these functions, Treasuries require consolidated data in order to manage these functions effectively. In the case of risk management, it become obvious that a firm cannot manage the exposures it doesn’t know about.

How to get there

Depending on your organization, the level of effort to pivot to a centralized Treasury framework can be large. In general, the following steps can help on the journey to centralization:

- Making the case to senior management – The benefits of centralization may not be readily clear to your firm’s senior management. For example, the Company may be used to the different business lines managing and hedging financial exposures on their own.As with most matters, making the cost benefit argument here makes the largest impact. For example, you may estimate the costs of hedging (in terms of people, bid/offer spreads, transaction costs, etc.) the many trades which exist today against the benefits of executing fewer trades under a centralized netting structure.

- Establish policies – Once senior management has bought in, policies governing Treasury activities help eliminate any ambiguity in the now centralized processes. Policies should lay out roles, responsibilities – for both Treasuries as well as business lines – and clearly defined escalation procedures.A key benefit here of documentation is to help standardize processes and help ensure the next step is achievable.

- Centralize processes and systems – With polices established, it is now time to execute. Treasurers should look to eliminate, or at least standardize, manual operations using spreadsheets, and consolidate various processes that have historically been performed at the business level. Similarly, data consolidation and standardization are a key piece of the centralization equation.A “wing to wing” Treasury Management Solution is key to enabling the centralization transformation. An integrated, automated single system ensures that the same system you input your transactions is the same system that at the end will account for them and analyze them for risk management.

Optimize benefits of centralization

Centralization is an iterative process – a continuous journey. Wherever a Company is on this path, it can take the opportunity to reflect whether their operations have been optimized, in effect, transforming themselves from serving as business operations to becoming business partners. Best-in-class treasuries will ask themselves:

- Do I look at my firm’s cash transactionally or holistically.

- Holitstic cash management – a complete view of bank balances, short-term liquidity needs (through A/P or A/R, for example) and long-term cash forecasts allows optimization of banking relationships and enhancement of return on cash through cash pooling and target balance management.

- Do I have a complete view of my firm’s financial exposures?

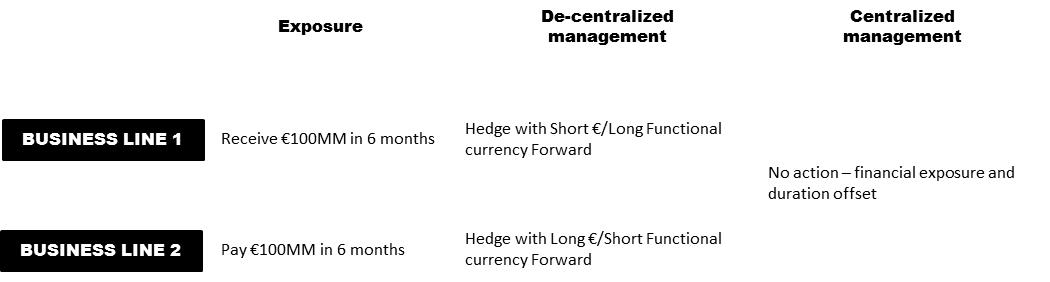

- Holistic cash management leads to having a consolidated view of exposures. Treasurers can then take action to mitigate the risk of their exposures through hedging actions efficiently by netting exposures, for example.

- Are my hedging activities executed efficiently?

- Electronic trading of OTC derivatives reduces execution costs. Solutions such as electronic confirmation matching allow confirmation and settlements to occur automatically.

- Am I able to use risk management tools to mitigate the entire universe of risks to the firm (e.g., market risk, credit risk, operational risk, compliance/regulatory risk)?

- Understanding and defining a firm’s risk appetite is the first step to using risk management tools effectively.

- Once this is accomplished, best-in-class firms integrate their risk policy into their execution systems – exposure limits, trader limits, counterparty credit limits as well as ensure compliance with regulatory requirements.

- Simply stated – How much time do I spend on information gathering vs information analytics?