How Australia’s Banks Became the World’s Biggest Property Addicts

Australia is riding out a huge gamble on property. The bet: 27 years of recession-free economic growth—during which Sydney home prices surged fivefold—would continue unabated and allow borrowers to keep servicing their debt.

The gamble has turned dicey. Tighter lending rules are deterring investors, and lofty prices are starting to deflate. A banking probe is exposing dodgy practices, and a mountain of risky loans that helped fuel the bubble needs refinancing—just as global borrowing costs rise. Now Australians are stuck with the highest household debt levels among G20 nations.

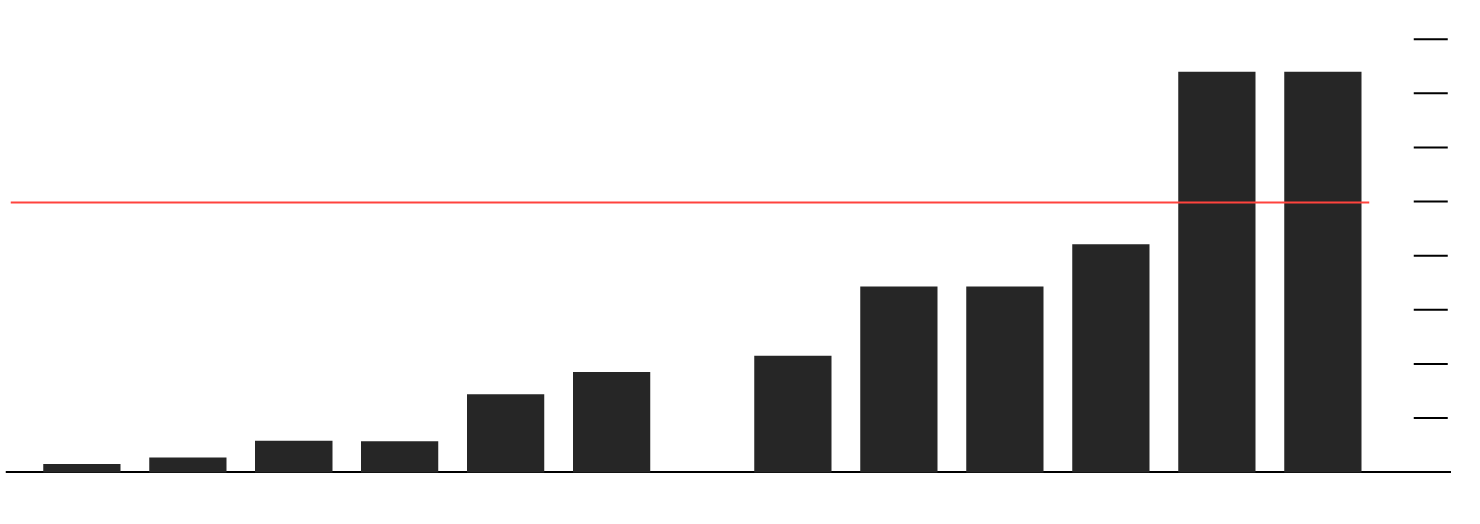

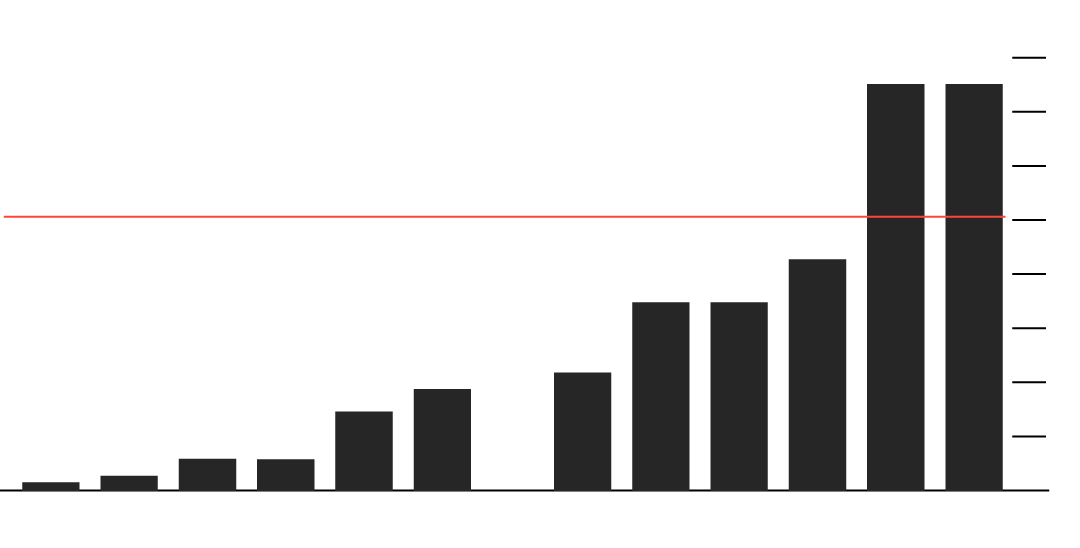

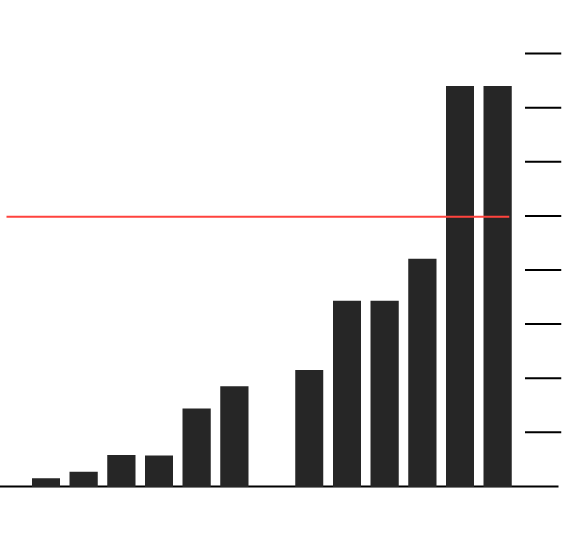

Australia household debt exceeds 120 percent of GDP

Australia

120%

Canada

South Korea

90

U.K.

U.S.

60

France

Japan

Germany

30

1992

2000

2008

2017

Australia

120%

Canada

South Korea

90

U.K.

U.S.

60

France

Japan

Germany

30

1992

2000

2008

2017

Australia

120%

Canada

S. Korea

90

U.K.

U.S.

60

France

Japan

Germany

30

1992

2000

2008

2017

Note: Household debt as % of GDP

Source: Bank for International Settlements

“Historically, we’ve seen that after economies have run up leverage, they’ve faced a hangover,” said Daniel Blake, economist at Morgan Stanley in Sydney.

He cites Bank for International Settlements research showing that household debt starts dragging on future economic growth once it’s equivalent to 80 percent of gross domestic product. Australia is sitting well on the extremes of that range, at above 120 percent.

While Australia’s banks remain well-capitalized and are still churning out massive profits, the millions of customers backing their biggest assets aren’t. Wage growth is elusive as indebted workers struggle to cling to their jobs, and consumption—which makes up more than half of the economy—is pressured as households scrimp to meet mortgage repayments.

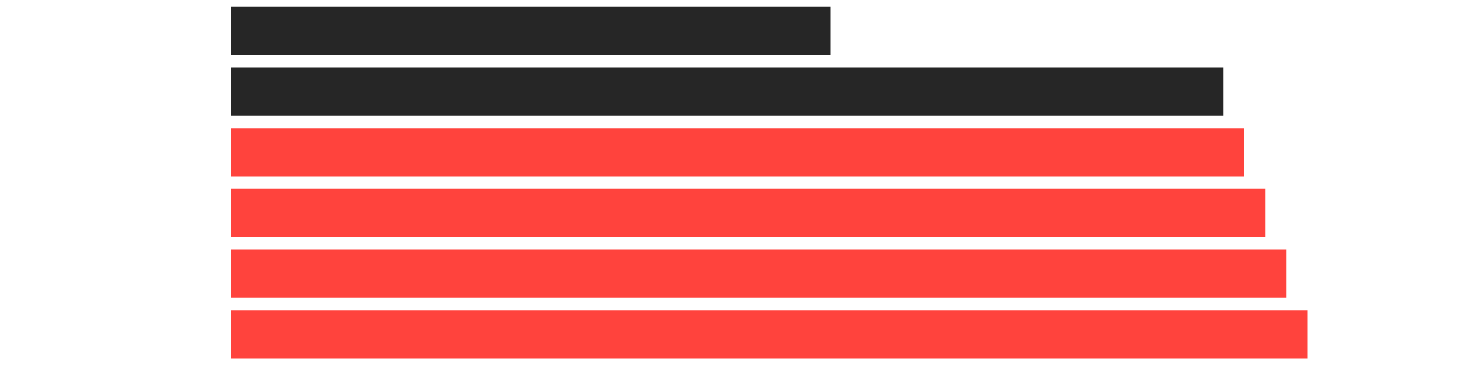

Australian banks’ mortgages are equivalent to 80 percent of the economy

GDP

A$1.73T

A$418B

A$406B

A$258B

A$253B

Banks

Commonwealth

Bank

Westpac

ANZ

National

Australia Bank

GDP

A$1.73T

Banks

A$418B

A$406B

A$258B

A$253B

Commonwealth

Bank

Westpac

ANZ

National

Australia

Bank

A$253B

National

Australia Bank

A$258B

ANZ

A$1.73T

A$406B

Westpac

A$418B

Commonwealth

Bank

GDP

Banks

Sources: Australian Prudential Regulation Authority, Australian Bureau of Statistics

Since the turn of the century, politicians Down Under have sold the “Australian Dream” by encouraging locals to take out mortgages and secure stakes in the property market—traditionally seen as an easy path to wealth.

When growth stumbled during the global financial crisis, the government started handing out checks to help buyers scrounge up deposits, bolstering the economy in the process. As the mining-investment bonanza to feed China’s demand for commodities started to splutter from 2012, the central bank rode to the rescue, cutting interest rates to record lows.

The exuberance got out of hand. Investors gorged on “interest-only loans” that required them to repay not even one cent of principal for up to five years. The frenzy for such loans peaked in June 2015, when they accounted for 46 percent of all new mortgages.

Now it’s time for those borrowers to start paying up: About A$360 billion ($266 billion) of those loans revert to interest and principal payments over the next three years, just as global borrowing costs are set increase.

The Reserve Bank of Australia isn’t yet pressing the panic button, saying its research suggests the damage from the loan rollovers should be minimal. Still, the household debt pile-currently at 189 percent of disposable income—has required it to tread warily. The RBA has kept interest rates unchanged since August 2016, the longest stretch in its modern history.

Natasha Arens, the borrower

Natasha Arens, the borrower

Natasha Arens, the borrower

For an immigrant from Russia and 47 year-old mother-of-three Natasha Arens, establishing a foothold in the property market was central to securing her family’s future in Australia.

“I was trying to give my family their share of the Australian Dream, which is owning property,” she said. “Some might say it’s crazy, but that’s what people seem to do.”

Arens said she followed a traditional strategy of betting that prices would go up in Australia. She had planned to eventually pay off the mortgage on her house by selling the additional properties after their value had risen.

“Many Aussie borrowers have bought into the housing market bubble and gone up to their eyeballs in debt,” said Andrew Charlton, director of consultancy AlphaBeta in Sydney and a one-time economic adviser to former Prime Minister Kevin Rudd. “They’ll stay afloat, so long as interest rates stay low and the economy is steady.”

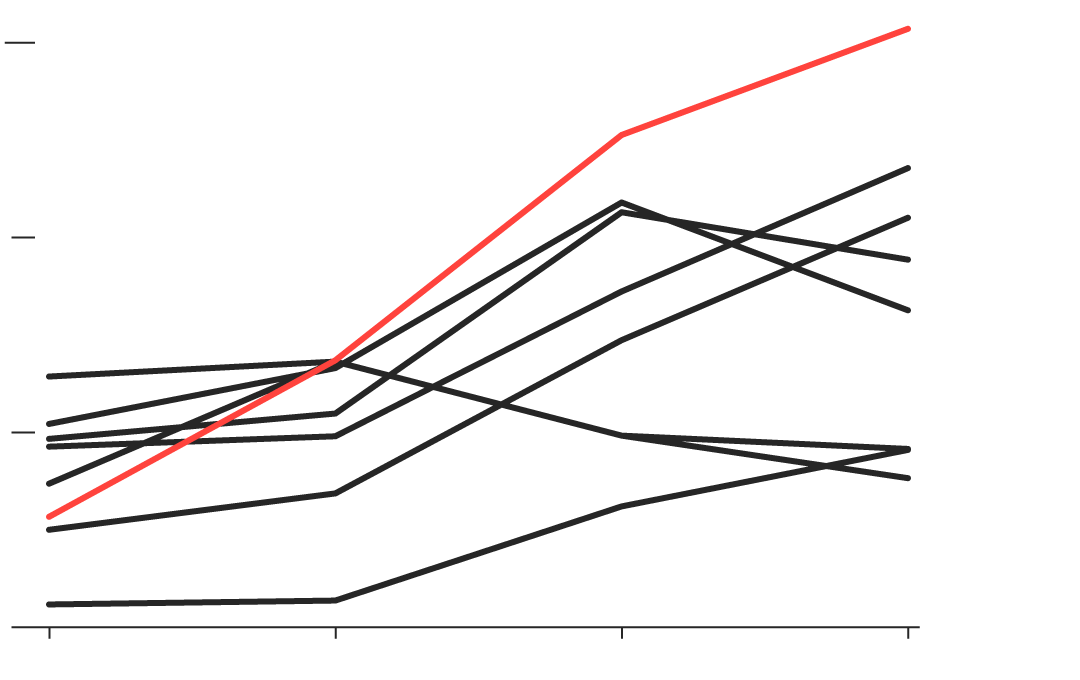

How an investor’s repayments could almost double

From 2014-2019

A$1,885

From 2019

A$3,173

Plus 1 rate hike

A$3,241

Plus 2 rate hikes

A$3,310

Plus 3 rate hikes

A$3,379

Plus 4 rate hikes

A$3,449

From 2014-2019

A$1,885

A$3,173

From 2019

Plus 1 rate hike

A$3,241

Plus 2 rate hikes

A$3,310

A$3,379

Plus 3 rate hikes

Plus 4 rate hikes

A$3,449

From 2014-2019

A$1,885

A$3,173

From 2019

Plus 1 rate hike

A$3,241

Plus 2 rate hikes

A$3,310

Plus 3 rate hikes

A$3,379

Plus 4 rate hikes

A$3,449

Note: Monthly repayments for A$500,000 interest-only mortgage borrowed at 4.5% over 25 years, switching to interest and principal mortgage after 5 years.

Source: Australian Securities & Investments Commission

Neither scenario is guaranteed. While the economy is forecast to grow at an above-average pace through 2020, the central bank has repeatedly warned that its biggest threats are external and real—and mainly from its biggest trading partner.

Australia is the developed world’s most China-dependent economy, and the RBA regularly cites China’s mountain of corporate debt as a major worry. Furthermore, as the U.S. ramps up trade war threats with the No. 2 economy, a significant hit to Chinese exports would see Australia caught in the crossfire. A shock erupting from either risk would see Australians start to lose their jobs and be unable to meet mortgage repayments.

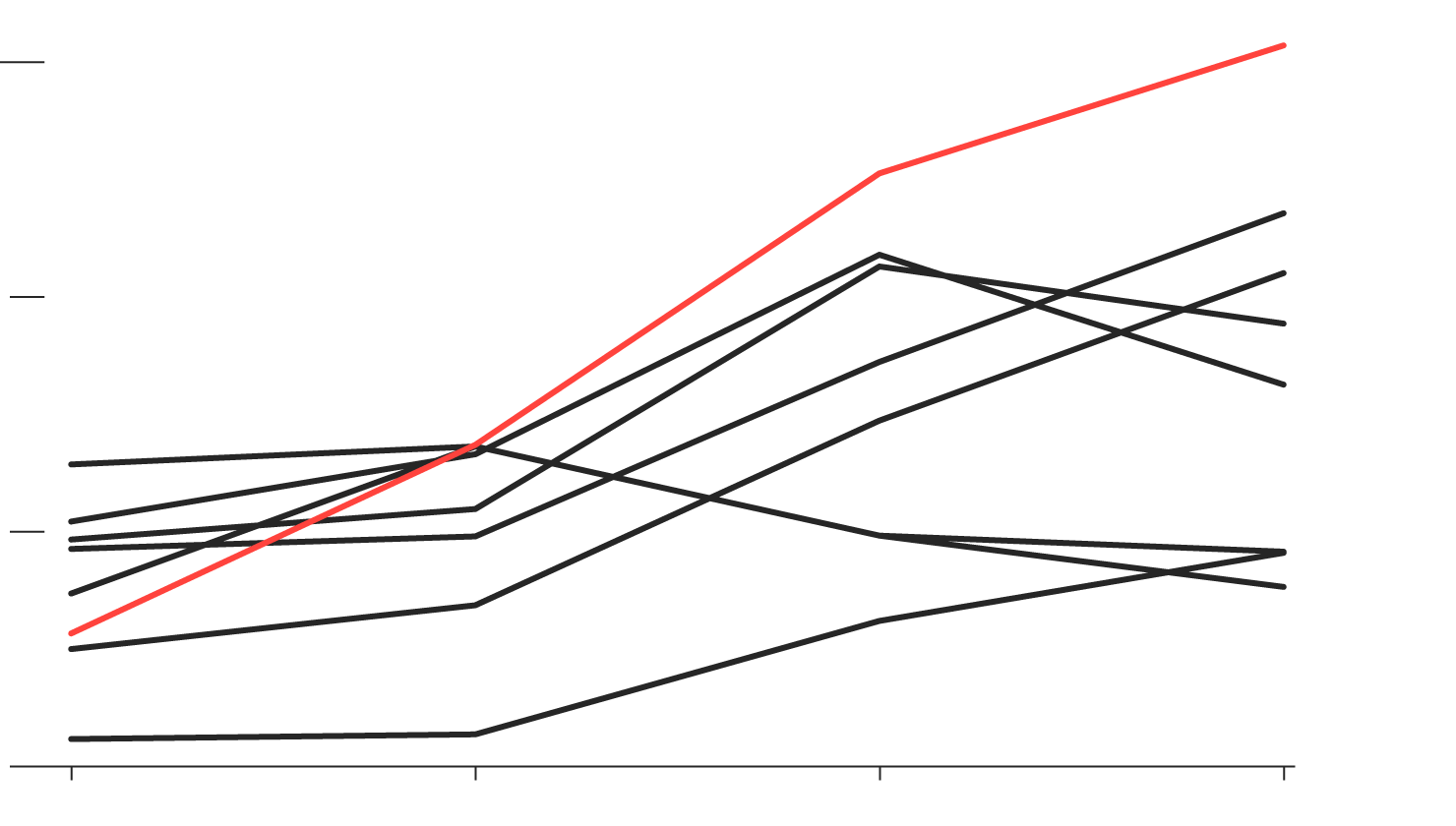

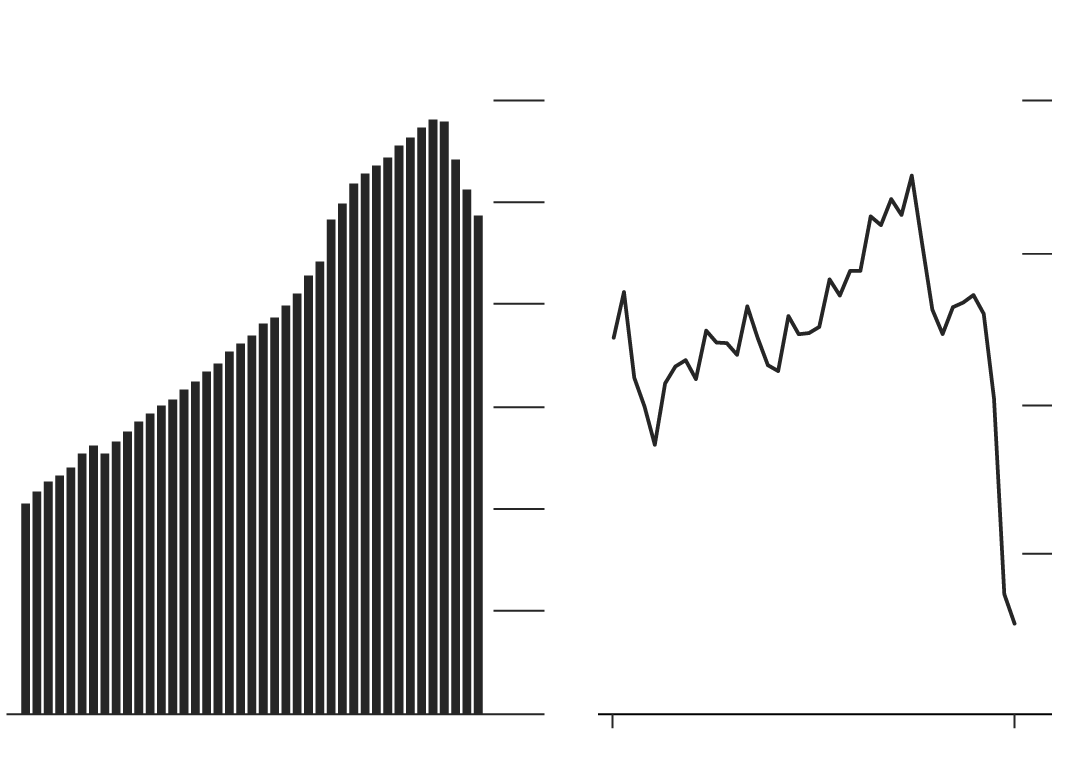

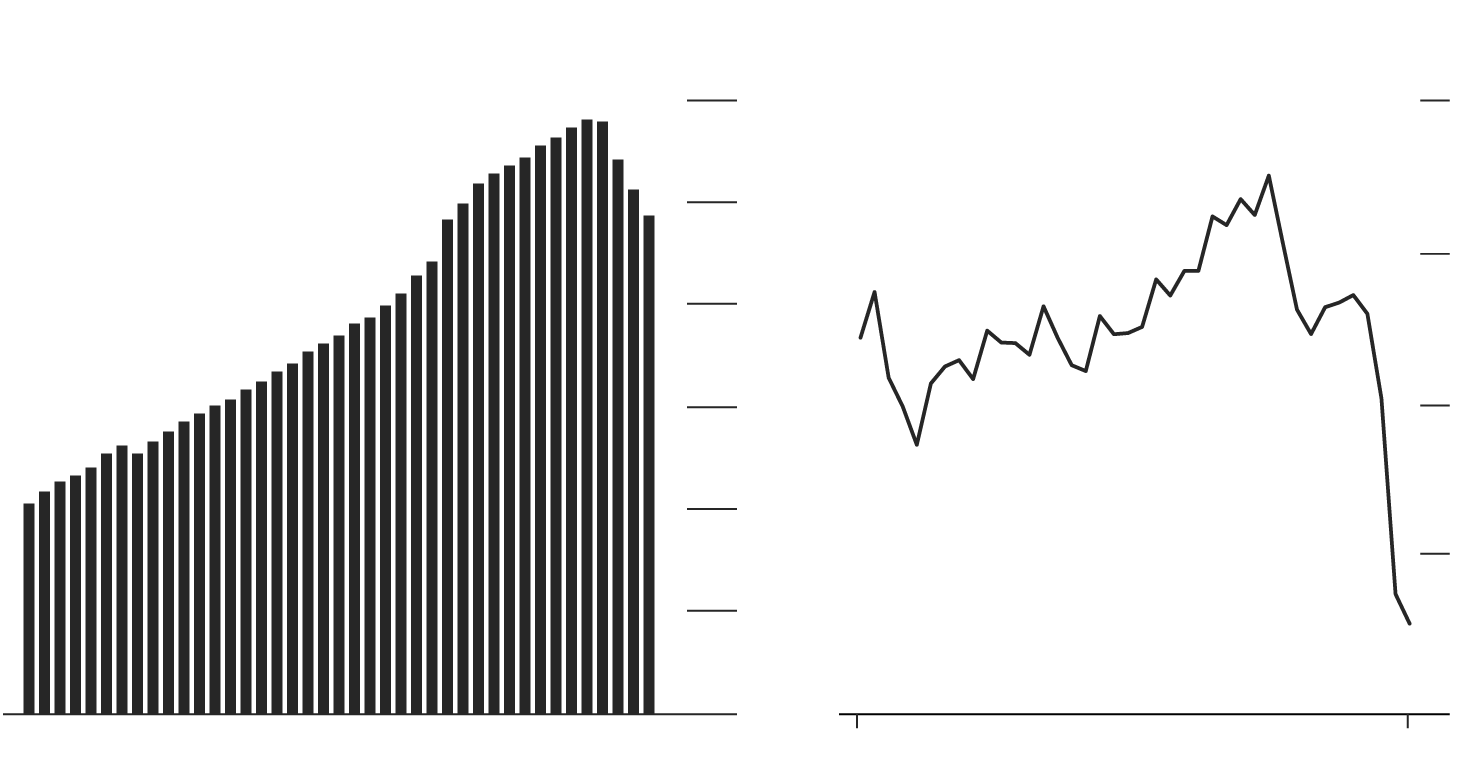

Higher rates just a question of time

80%

70

60

Better than even chance of a rate rise

50

40

30

20

10

0

07/2018

07/2019

80%

70

60

Better than even chance of a rate rise

50

40

30

20

10

0

07/2019

07/2018

80%

70

60

Better than even

chance of a rate rise

50

40

30

20

10

0

07/2018

07/2019

Note: Swap traders’ expectations of RBA’s next interest-rate move

Source: Bloomberg Data

And then there’s interest rates. RBA Governor Philip Lowe has stressed they’ll eventually rise, but only once the sticky jobless level—currently at 5.4 percent—nears the central bank’s full employment estimate of 5 percent and inflation climbs closer to target. While markets and most economists don’t expect a hike for at least a year, U.S. tightening will inevitably lift costs for Australian banks, which tap foreign funding to finance their lending.

“The worst case is where interest rates rise very, very rapidly overseas—and not just the central bank rates or overnight rates, but bond rates,” said Roger Montgomery, founder and chief investment officer of Montgomery Investment Management Pty. “That could be a problem because we know that even prime borrowers, if they have negative equity, that significantly increases the propensity to default.”

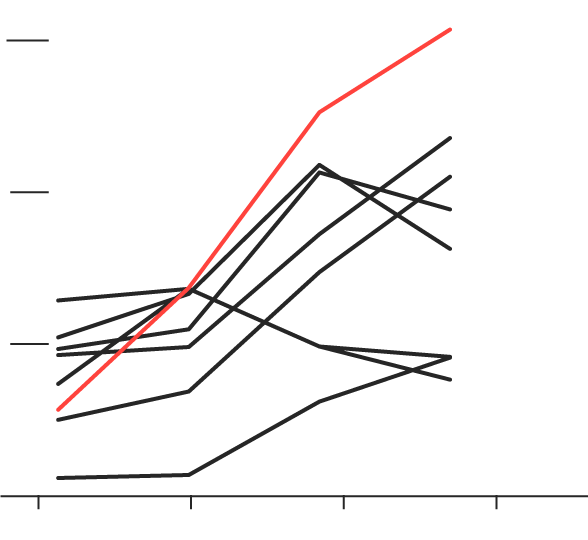

Australia’s banks are on notice. Alarmed by the free-for-all in risky loans and the deterioration in standards that accompanied lenders fighting for market share, regulators slapped them with curbs that included restrictions on interest-only lending. The value of new interest-only lending, which is the preferred option of investors, is down 57 percent on a year ago.

Banks are handing less money to investors

50%

Curbs

placed on

interest-only

loans

40

30

20

10

0

–10

–20

First of two

RBA rate cuts

–30

2011

12

13

14

15

16

17

2018

50%

Curbs

placed on

interest-only

loans

40

30

20

10

0

–10

–20

First of two

RBA rate cuts

–30

2011

2012

2013

2014

2015

2016

2017

2018

50%

Curbs

placed on

interest-only

loans

40

30

20

10

0

–10

–20

First of two

RBA rate cuts

–30

2011

2012

2013

2014

2015

2016

2017

2018

Note: The year-on-year change in the value of outstanding and newly approved housing loans to investors.

Source: Australian Bureau of Statistics

Edward Doueihi, the developer

Edward Doueihi, the developer

Edward Doueihi, the developer

Builders are delaying residential projects because prices have soared out of many Australian buyers' reach, while some Chinese investors have left the market altogether, said Edward Doueihi, 46 year-old managing director at Sydney property developer Ceerose.

Some developers are putting jobs on hold, either because developers can’t get pre-sales to make a project work or they can’t get funding, he said. The result is that the 30-year industry veteran is now looking for alternative opportunities.

“We’ve been looking at going international.”

The adequacy of lending standards has been a key focus of an independent inquiry into financial misconduct. The Royal Commission has heard of banks failing to verify borrowers’ finances and staff falsifying loan documents to collect bonuses. Analysts are betting the revelations will lead to greater regulation of the mortgage market and force banks to tighten lending standards further.

How resilient will Australian households be in the event of an economic downturn? The RBA last year estimated that the average borrower has a buffer equivalent to 2 1/2 years of repayments. Drilling down, the picture is somewhat darker: One-third of borrowers have enough funds to cover just one month’s mortgage payment, if that.

Redom Syed, the broker

Redom Syed, the broker

Redom Syed, the broker

Sydney-based mortgage broker Redom Syed said he has seen a “material clampdown” since the start of the Royal Commission banking inquiry, with lenders ramping up verification of borrowers’ income and living expenses.

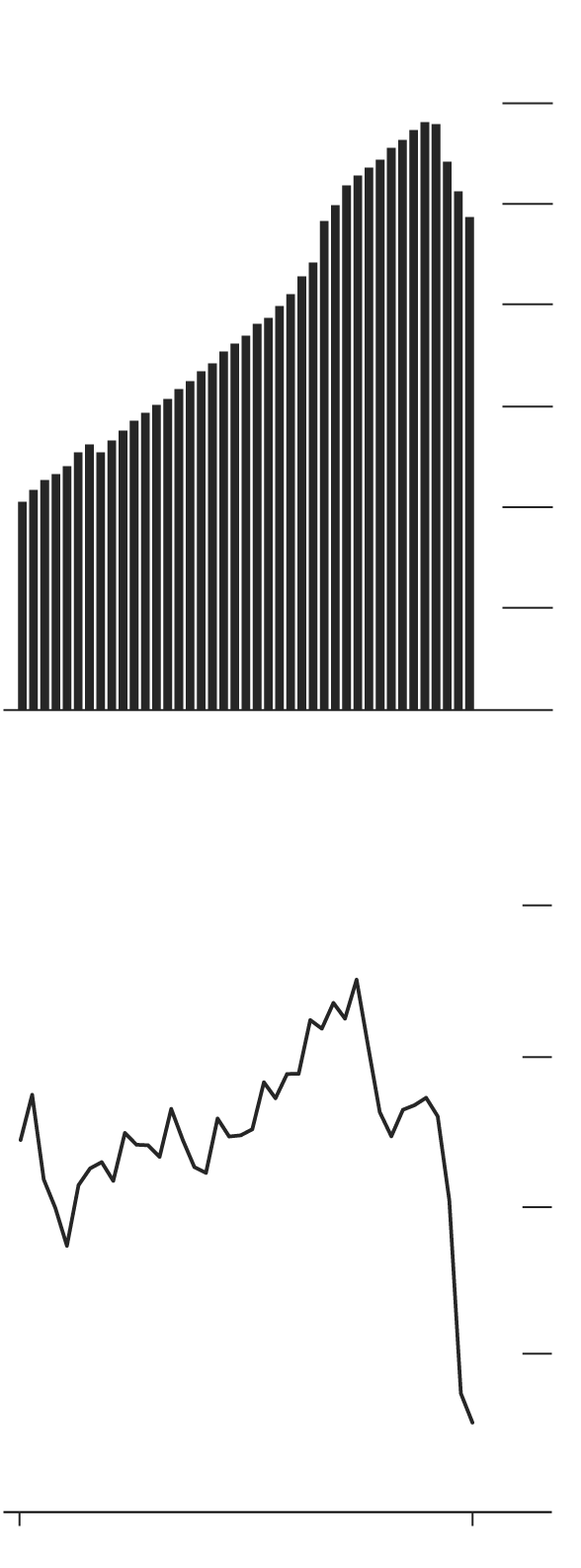

The rise and fall of Australia’s risky mortgages

Outstanding interest-only loans

A$600B

Interest-only lending

has almost tripled

since 2008 ...

500

400

300

200

100

0

03/2008

03/2018

Interest-only loans as portion of total bank loans

50%

40

30

... but issuance

as a portion of total

lending has plunged

since the regulator

tightened rules.

20

10

03/2008

03/2018

Outstanding interest-only loans

Interest-only loans as portion of total bank loans

50%

A$600B

Interest-only lending

has almost tripled

since 2008 ...

500

40

400

30

300

... but issuance

as a portion of total

lending has plunged

since the regulator

tightened rules.

200

20

100

0

10

03/2008

03/2018

03/2008

03/2018

Outstanding interest-only loans

Interest-only loans as portion of total bank loans

50%

A$600B

500

Interest-only lending

has almost tripled

since 2008 ...

40

400

30

300

... but issuance

as a portion of total

lending has plunged

since the regulator

tightened rules.

200

20

100

0

10

03/2008

03/2018

03/2008

03/2018

Source: Australian Prudential Regulation Authority

“Banks are very nervous, and it’s making the approvals process tricky and uncertain and is naturally having an impact on the market” said Syed, 28, who set up his firm Confidence Financial after leaving the Australian Treasury, where he advised on international financial markets.

Syed is also seeing a number of “surprised” interest-only clients, who were unaware that their repayments are set to increase and are now scrambling for options. For every A$1 million of mortgage debt, a borrower now needs roughly A$40,000 more in household income than three years ago, Syed said. For those on the wrong side of the new restrictions, options are limited: Find the money for higher payments, move to another interest-only loan at a non-bank lender or sell the property.

“Many Australians are sailing close to the wind and will be in trouble if a storm comes,” said AlphaBeta’s Charlton. “If interest rates rose materially, it would push many Australian households into severe mortgage stress.”

Correction: A previous version of the “Higher rates just a question of time” chart had an inaccurate date range.